Market & Macro

Qualcomm After Investor Day: What Wall Street Is Actually Debating

Qualcomm's latest filings show a handset decline, fast automotive growth, resilient licensing economics, and a much larger data-center promise. Here is the evidence Wall Street still needs.

Qualcomm's Wall Street debate changed on June 24, 2026. The company is no longer asking investors to view it only as a premium-phone chip and patent-licensing franchise. It is asking them to underwrite a broader computing platform across cars, industrial systems, personal devices, and data centers. The latest actual results, however, still show a business whose earnings quality is tied to phones and licensing.

| Time horizon | Evidence on the page | The real question |

|---|---|---|

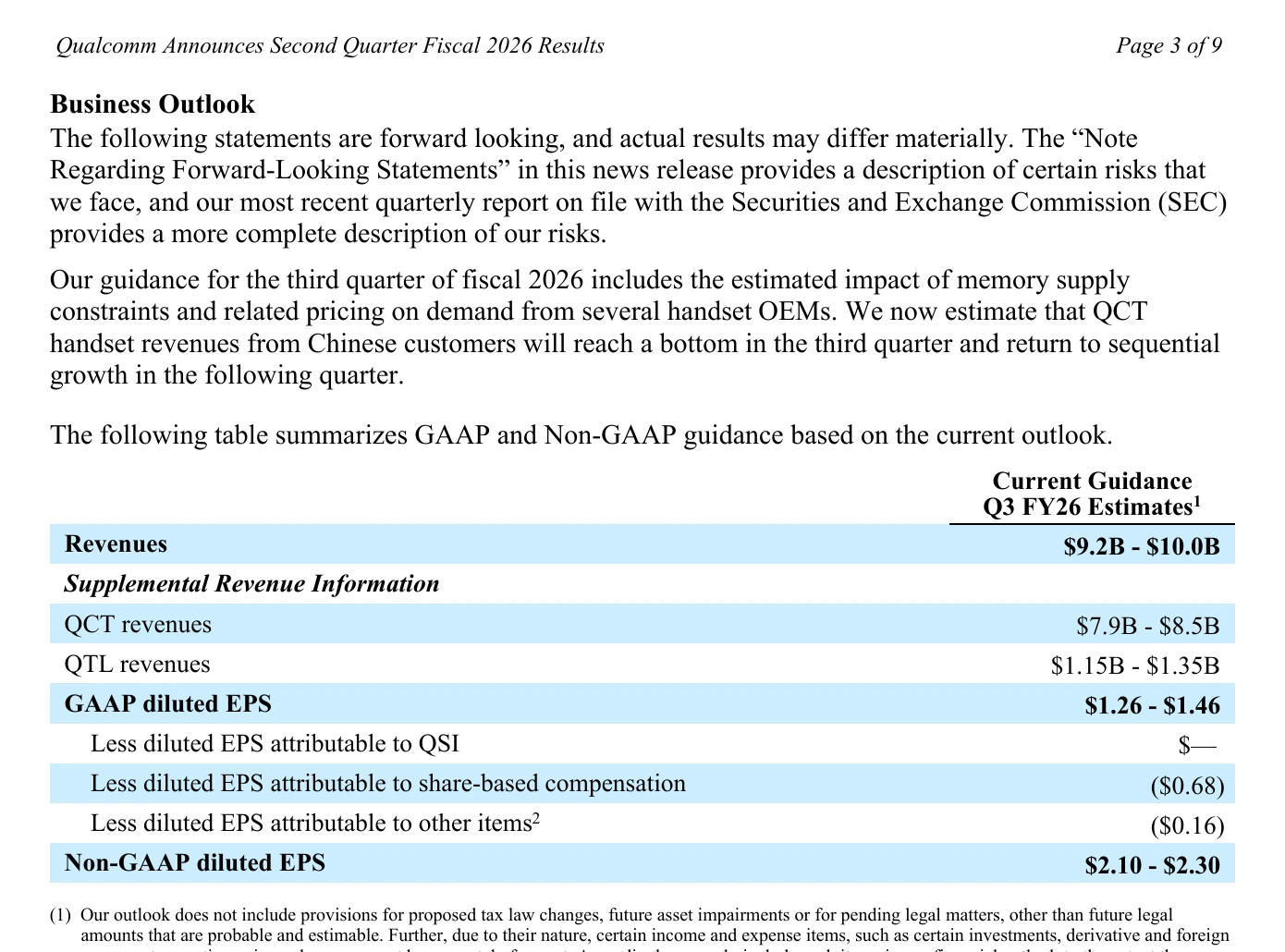

| Near term | Q3 FY2026 revenue guide of $9.2B-$10.0B | Does handset demand stop weakening? |

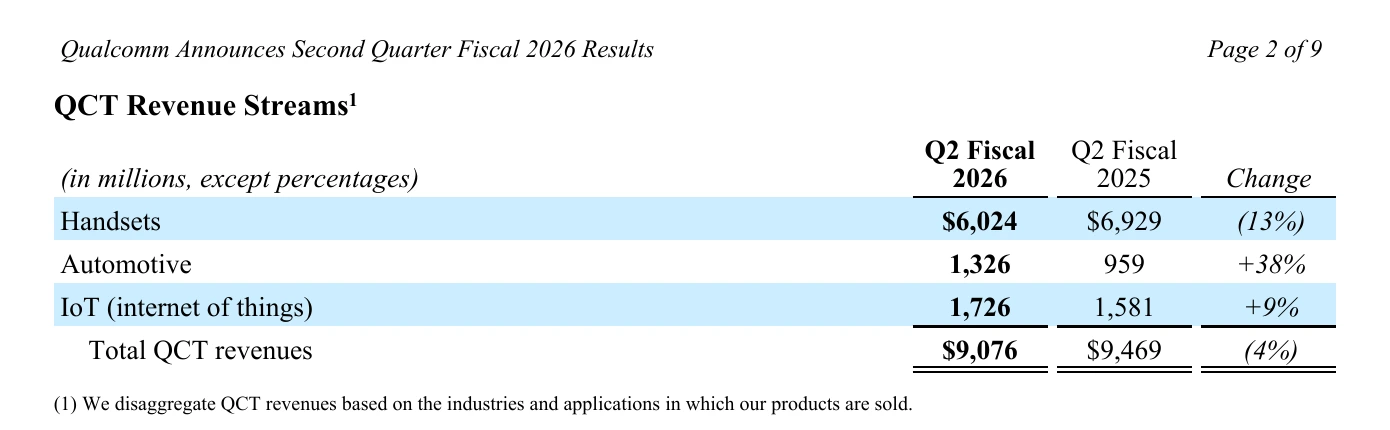

| Current mix | Q2 FY2026 handsets -13%, automotive +38%, IoT +9% | Can the new engines offset the old one in dollars? |

| Long term | FY2029 non-handset revenue of $40B and data-center revenue above $15B | When do targets become disclosed revenue? |

What you see is a company with a credible diversification direction and an unfinished financial transition. Why it matters: the stock's quality depends on the mix of earnings, not only the size of the opportunity. The table cannot prove that FY2029 goals will be met. The next check is whether reported revenue begins to close the gap.

2026-07-13, page 2. Values are USD millions.Thesis

The evidence supports a balanced conclusion. Qualcomm has real growth assets outside phones, and QTL remains a high-margin licensing engine. Yet the latest quarter shows that automotive and IoT growth has not fully neutralized the handset decline. Investor Day added substantial data-center optionality, but optionality should not be counted like current revenue.

The best reading is therefore neither a simple phone-cycle story nor a completed AI-platform story. It is a transition with three proof gates: near-term handset stability, faster mix improvement, and disclosed data-center conversion. Until those gates are visible in reported results, the long-term narrative should carry a larger execution discount than the headline targets imply.

Source Evidence Snapshot

The first proof is the issuer's own segment table. Q2 FY2026 handset revenue fell from $6,929M to $6,024M, a $905M decline. Automotive increased from $959M to $1,326M, while IoT increased from $1,581M to $1,726M. The direction is favorable outside phones, but the dollar bridge is not complete.

Source-derived visual: figures from the Qualcomm Q2 FY2026 earnings release, page 2; editorial math adds the $367M automotive increase and the $145M IoT increase to reach $512M.

What you see is the offset problem in dollars: +$512M from automotive and IoT did not cover -$905M from handsets, leaving total QCT revenue down $393M. Why it matters: high growth rates in smaller segments can look more powerful than their current earnings weight. This visual cannot tell us whether the handset decline is structural or a temporary inventory and memory-cost effect. The next check is the company's Q3 FY2026 guide and the following quarter's handset recovery.

2026-07-13, page 3; the table is company guidance, not an article forecast.The guide makes the near-term caution explicit. Qualcomm put Q3 FY2026 revenue at $9.2B-$10.0B, QCT revenue at $7.9B-$8.5B, QTL revenue at $1.15B-$1.35B, and non-GAAP diluted EPS at $2.10-$2.30; management also said Chinese-customer handset revenue was expected to bottom in the quarter and return to sequential growth afterward.

What the guide proves is that the memory and inventory pressure was incorporated into the company's next-quarter range. It does not prove the bottom will hold. The next useful evidence is the reported handset number, not a new description of end demand.

What the Street Is Pricing

Wall Street now has to price three different businesses inside one ticker. The first is a cyclical premium-handset chip franchise. The second is QTL, whose patent-licensing economics remain unusually profitable. The third is a set of growth options in automotive, IoT, personal computing, robotics, and data centers.

The latest Form 10-Q shows why the licensing engine matters. QTL produced $1,382M of revenue and $994M of earnings before tax in Q2 FY2026, a 72% segment EBT margin. QCT, by comparison, produced $9,076M of revenue and $2,465M of EBT, a 27% margin. The smaller licensing segment therefore contributes a disproportionate share of segment profit.

Source-derived visual: Qualcomm's Investor Day 2026 press release, dated 2026-06-24; all FY2029 figures are company targets, not actual results, consensus estimates, or article projections.

The long-term ambition is materially larger than the current revenue base. Qualcomm raised its FY2029 non-handset revenue goal to $40B, including more than $15B from data centers, $10B from automotive, and more than $14B from IoT. It also expanded the automotive design-win pipeline to $65B and said handsets should represent about 33% of QCT revenue in FY2029.

What you see is a proposed change in the company's earnings identity. Why it matters: a broader, recurring mix could reduce dependence on handset replacement cycles. The map cannot prove customer ramps, market share, or future margins. The next check is disclosed revenue by new category and the operating spending required to produce it.

The market-pricing question is therefore not whether the addressable markets are large. It is how much probability to assign to the bridge from current QCT economics to the FY2029 mix. Treating all of the bridge as certain would ignore execution; treating it as worthless would ignore the already visible automotive and IoT growth.

Risks to the Thesis

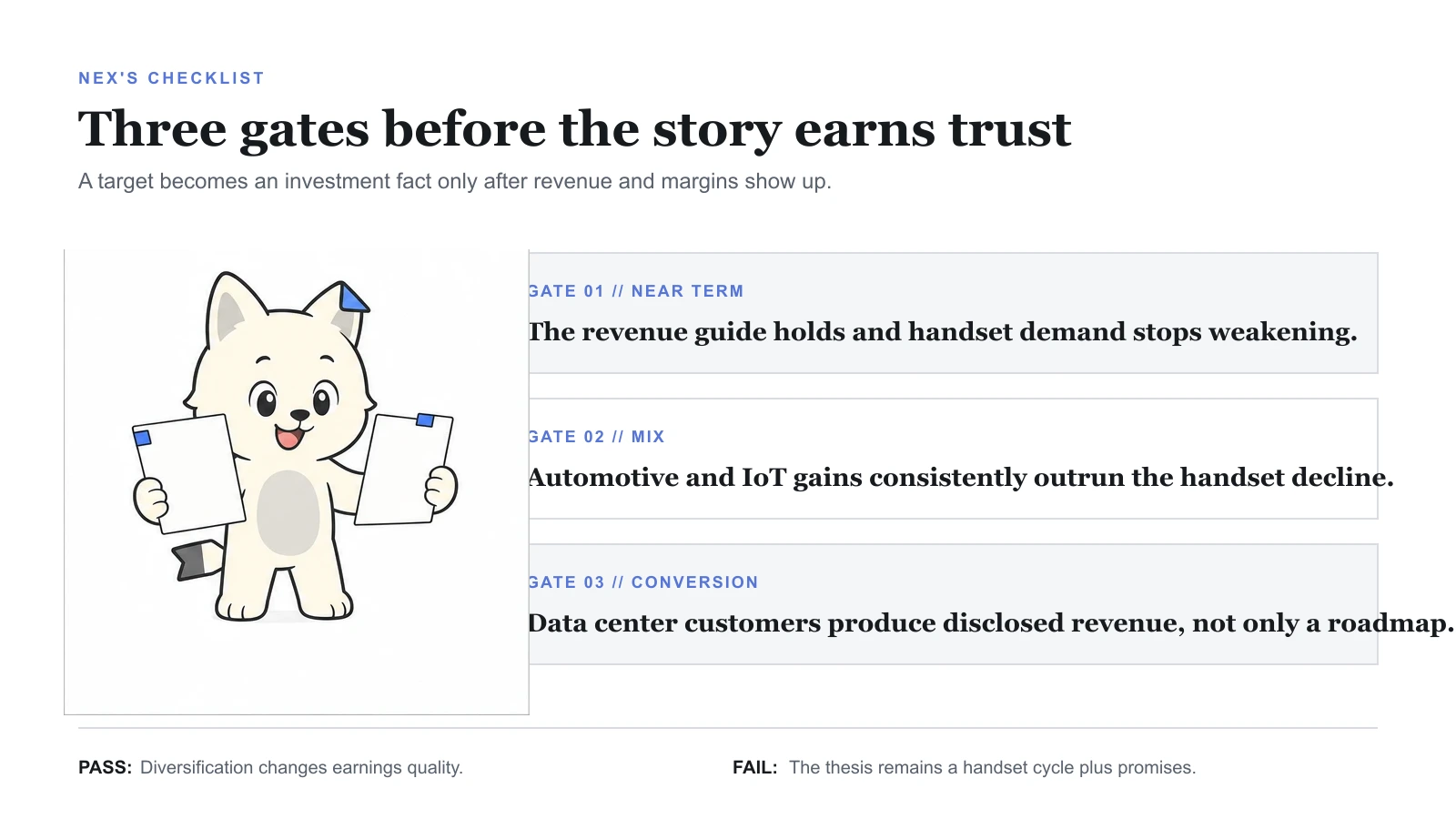

Explanation visual: Nex separates current operating evidence from management ambition. The three gates are an editorial monitoring framework derived from the latest earnings release, Form 10-Q, and Investor Day disclosures.

Nex's checklist prevents a large target from doing the work of a reported result. What you see is a sequence: stabilize the base, improve the mix, then verify conversion. Why it matters: a weak base can consume the gains from new businesses. The framework cannot predict timing. The next check is each gate against the next filing.

| Risk | Current evidence | What would make it worse |

|---|---|---|

| Handset cycle | Q2 FY2026 handset revenue -13% | Q3 FY2026 misses the guide or the expected rebound slips |

| Margin pressure | QCT EBT margin 27%, down 3 points | New-category spending rises before revenue conversion |

| Customer concentration | Two customers or licensees represented 24% and 22% of Q2 FY2026 revenue | More insourcing or weaker premium-device demand |

| Licensing durability | Key OEM license terms expire between fiscal 2027 and fiscal 2031 | Renewals weaken pricing or legal protection |

| Data-center execution | FY2029 target above $15B | Product schedules or customer ramps fail to become disclosed revenue |

The table shows that the main risks are linked. Handset weakness pressures QCT revenue, investment in new categories can pressure margin, and concentration increases the cost of a customer-specific change. None of these risks invalidates the diversification strategy by itself. Together, they explain why evidence of conversion matters more than a large addressable-market claim.

What Flips the Call

The conclusion becomes more constructive if Q3 FY2026 lands within the published range, handset revenue then returns to sequential growth, and automotive plus IoT dollar gains begin to cover the handset drag. A separate positive flip is disclosed data-center revenue with enough margin detail to judge whether the business improves earnings quality rather than only total sales.

The conclusion weakens if Q3 FY2026 falls below the range, the handset recovery keeps moving out, QCT margin remains under pressure, or the first data-center ramps require spending that overwhelms their contribution. By FY2027, investors should expect more than customer names and roadmaps; they should expect a measurable revenue bridge toward FY2029.

This is the clean decision boundary: Qualcomm does not need every new category to win. It does need the combined new engines to outgrow the erosion in the old concentration points while preserving the licensing cash engine.

Methodology, Sources & Disclosure

This article separates actual results, company guidance, management targets, and editorial interpretation. Dollar-bridge calculations use disclosed segment values; no private analyst research, proprietary estimates, valuation model, or share-price objective is used. Facts were checked as of 2026-07-13.

- Qualcomm Q2 FY2026 earnings release

- Qualcomm Form 10-Q for the quarter ended March 29, 2026

- Qualcomm Investor Day 2026 press release

This is general information, not individualized investment advice. The article does not issue a rating or a share-price objective.