The CHIPS Act Is Reshaping Semiconductor Stocks — Here's Who Wins

The US is spending $52B+ to bring chip manufacturing home. TSMC still dominates, but Intel, GlobalFoundries, and others are racing to close the gap. Here's what it means for semiconductor stocks.

Hynexly

The Biggest Industrial Policy Bet in a Generation

Here's a number that should grab your attention: the United States currently manufactures about 12% of the world's semiconductors. In 1990, that number was 37%.

Let that sink in. The country that invented the transistor, built Silicon Valley, and designs the most advanced chips on the planet makes barely one in ten of them.

The CHIPS Act is Washington's attempt to reverse that decline, and it's already reshaping the semiconductor landscape in ways that matter for your portfolio.

The $52 Billion Question

The CHIPS and Science Act, signed in 2022, committed $52.7 billion in subsidies and an additional 25% investment tax credit for semiconductor manufacturing on US soil. The money has been flowing — and the fabs are being built.

As of early 2026, here's where the major investments stand:

- TSMC — $65B+ committed to Arizona fabs, with the first facility producing chips and the second under construction

- Intel — $100B+ planned across Ohio, Arizona, New Mexico, and Oregon, backed by $8.5B in CHIPS Act grants

- Samsung — $25B+ Texas expansion underway

- GlobalFoundries — $12B+ New York expansion with $1.5B in CHIPS Act funding

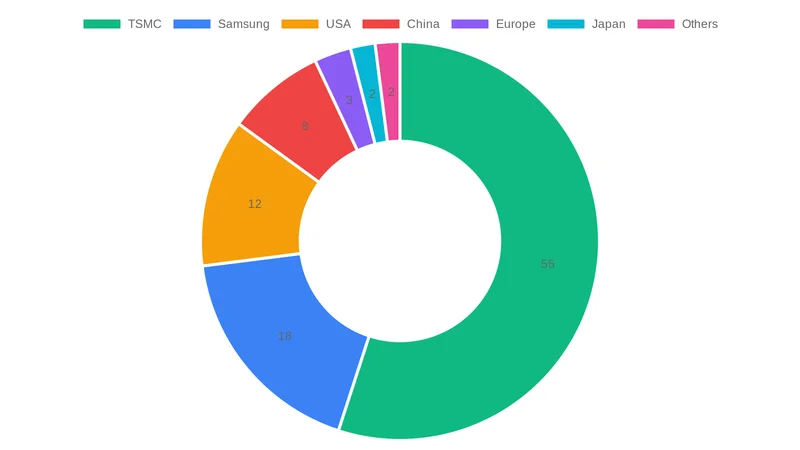

This isn't just corporate welfare — it's a national security imperative. Taiwan produces roughly 60% of the world's semiconductors and over 90% of the most advanced chips. A single earthquake, blockade, or military conflict could cripple the global technology supply chain overnight.

TSMC: Still the King, But Building in America

Let's be clear: TSMC remains the undisputed leader in advanced semiconductor manufacturing, and no amount of US subsidies is going to change that in the near term. Their process technology is at least 2-3 years ahead of the nearest competitor, and their manufacturing yields are the envy of the industry.

But TSMC building in Arizona is significant. The first fab is already producing 4nm chips — a milestone that many skeptics said couldn't happen on American soil. The second fab targeting 3nm and 2nm nodes is progressing.

For TSMC shareholders, the US expansion is a mixed bag. It diversifies geographic risk (positive), but US manufacturing costs are 30-50% higher than Taiwan (negative). The CHIPS Act subsidies help close that gap, but don't eliminate it entirely.

My take: TSMC at current valuations is fairly priced. It's a phenomenal company but the stock reflects that. I'd be a buyer on any dip below 15x forward earnings.

Intel: The Comeback Kid or the Comeback Flop?

This is the most polarizing stock in semiconductors right now, and I have strong feelings about it.

Intel's CEO has staked the company's future on becoming a world-class foundry — manufacturing chips not just for Intel, but for other companies too. It's an audacious strategy. The CHIPS Act makes it possible by de-risking billions in capital expenditure with government subsidies.

The bull case: Intel has the most CHIPS Act funding of any company. Their Intel 18A process node (comparable to TSMC's 2nm) has shown promising early results. If they execute, Intel could capture a meaningful share of the foundry market and justify a massive re-rating.

The bear case: Intel has been promising manufacturing comebacks for years and consistently underdelivered. Their current-generation products still trail AMD and Apple's TSMC-manufactured chips in performance-per-watt. And building a foundry business from scratch while your core business faces competitive pressure is incredibly difficult.

I'm cautiously optimistic. Intel at $25-30 is pricing in a lot of bad news. The CHIPS Act funding is real downside protection — the US government essentially can't afford for Intel to fail. But I'm keeping my position size modest because execution risk is very real.

The Second-Tier Winners

Beyond TSMC and Intel, several companies are benefiting from the reshoring trend in less obvious ways:

GlobalFoundries (GFS) — The "other" American foundry. They don't compete at the bleeding edge, but they manufacture the mature-node chips that go into cars, industrial equipment, and defense systems. Their CHIPS Act funding positions them well, and their partnership with the DoD is a long-term revenue anchor.

Applied Materials, Lam Research, KLA — These are the picks and shovels of the semiconductor industry. Every new fab needs billions of dollars in equipment, and these three companies dominate the market. The CHIPS Act is essentially a multi-year equipment spending cycle, and they're the biggest beneficiaries.

Texas Instruments (TXN) — TI has been quietly building new 300mm fabs in Texas and Utah. They don't get the headlines, but their strategy of investing in capacity for analog and embedded chips during a downturn is classic TI — disciplined, long-term, and likely to pay off.

The Losers of Reshoring

Not everyone wins in this new landscape.

Fabless companies with no US manufacturing may face pressure if "made in America" requirements expand beyond defense contracts into broader government procurement. Companies heavily dependent on Asian manufacturing could see cost disadvantages.

Chinese semiconductor companies are the clearest losers. US export controls have cut them off from the most advanced manufacturing equipment, and the CHIPS Act's guardrails prevent recipients from expanding advanced capacity in China. The technological gap is widening.

What This Means for Your Portfolio

The CHIPS Act reshoring trend is a multi-year investment theme, not a quick trade. Fabs take 3-5 years to build and ramp to full production. The spending is just getting started.

Here's how I'm positioned:

Equipment makers are my highest-conviction play. AMAT, LRCX, and KLAC benefit regardless of which chipmakers win. Every dollar of fab construction translates into equipment sales.

TSMC remains a core semiconductor holding. Dominant technology, expanding geographic footprint, and the most important company in the global tech supply chain.

Intel is a speculative position. Small enough that I can sleep at night if it doesn't work out, but large enough to matter if the turnaround delivers.

Avoid chasing political narratives. The CHIPS Act is real money with real impact, but don't overpay for "reshoring premium." These are cyclical businesses at the end of the day.

The Bottom Line

The United States is making its biggest bet on industrial policy since the space race. $52 billion in subsidies, tens of billions more in private investment, and a national security mandate are reshaping where the world's most critical technology is manufactured.

For investors, the opportunity is clear but requires patience. The equipment makers are the safest way to play it. TSMC remains the quality anchor. Intel is the swing factor that could make or break the reshoring narrative.

The chips are — quite literally — on the table.

Not financial advice. I hold positions in several semiconductor stocks mentioned above.