Market & Macro

What the 2026 FOMC Calendar Says About When Fed Cuts Can Come

Before treating rate cuts as the base case: the FOMC calendar, CPI release timing, and the repeated-confirmation threshold the Fed has actually signaled. A 2026 read.

Thesis

(Source: Federal Reserve - FOMC Calendars and Information; U.S. Bureau of Labor Statistics - CPI Home)

The Federal Reserve's 2026 FOMC calendar, captured 2026-04-05, is not a forecast document — it is a layout of fixed dates. Set those meeting dates beside the BLS CPI "Next Release" schedule, which we re-checked the same day, and a pattern shows up: several CPI prints land between policy windows, not on them. That side-by-side is what persuaded us the consensus "faster easing" story was treating single data months as if they were decisions. The rest of this piece works from the pairing, not from any one headline.

The early-year consensus across many macro desks pointed to a faster easing cycle, but by spring that path had to be repriced. The key shift was not one headline. It was a repeated mismatch between market optimism and policy caution.

A durable policy framework in 2026 requires separating three layers:

- Calendar reality: meetings occur on fixed dates and policy decisions are interval-based.

- Data reality: inflation and labor releases can move expectations between meetings.

- Risk reality: supply-side and geopolitical shocks can delay easing even when headline inflation looks better for a month.

This structure prevents overreacting to isolated prints.

Source Evidence Snapshot

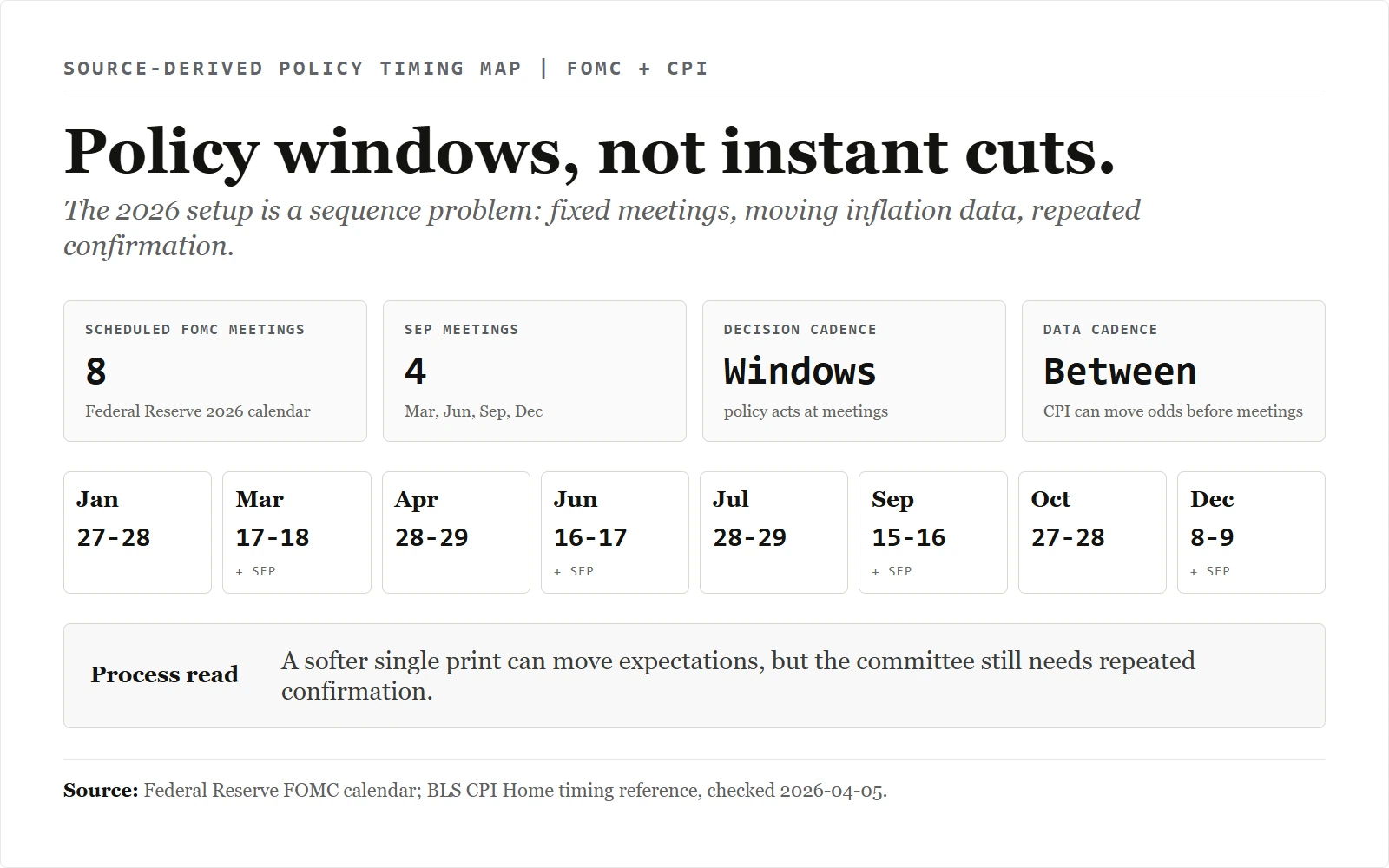

The hero map ties the Federal Reserve's 2026 FOMC calendar to the CPI timing reference. The point is sequencing: fixed policy windows, moving inflation data, and repeated confirmation before a cut case gets stronger.

Source capture: Federal Reserve - FOMC Calendars and Information, captured 2026-04-05; the evidence map renders the 2026 FOMC calendar beside the BLS CPI timing reference. The dates are the sources'; the layout is ours.

Source note: U.S. Bureau of Labor Statistics - CPI Home, checked 2026-04-05 for the "Next Release" section.

What Is Holding the Committee Back

1) Inflation confirmation still needs repetition

One softer month can improve risk sentiment, but policy direction usually requires persistence. Core components, services inflation behavior, and breadth of cooling matter more than a single headline surprise.

2) Energy and geopolitical inputs remain unstable

Monetary policy is a demand tool. It cannot directly remove supply disruptions, shipping risk premia, or commodity shock channels. That creates a policy asymmetry: easing too early can be costly if supply-side pressures re-accelerate.

3) Labor data has not delivered a clear break

When employment and wage indicators remain relatively firm, the urgency to cut is lower. In that environment, the committee can prioritize confirmation over speed.

Market Implications: Why Repricing Matters

Repricing from "many cuts" to "fewer and later cuts" has two consequences:

- Duration exposure becomes highly sensitive to each inflation and labor release.

- Equity leadership tends to reward earnings credibility over multiple expansion alone.

This does not imply no cuts. It implies that the evidence threshold for a stronger easing case has risen.

A Scenario Grid for the Next Policy Window

Article-derived scenario grid: framework from this section, grounded in the FOMC calendar and CPI timing reference. It is not a probability model; it counts branches before assigning market-data weights. The layout is ours.

Article-derived scenario grid: framework from this section, grounded in the FOMC calendar and CPI timing reference. It is not a probability model; it counts branches before assigning market-data weights. The layout is ours.

Base case: delayed but orderly easing

Inflation trends lower gradually and labor remains stable enough to avoid recession conditions. Easing arrives later, and the path is shallow.

Sticky-inflation case: fewer cuts than priced

If progress stalls in core services or energy pressure feeds into expectations, the first cut can be pushed out and total cuts can be lower than consensus.

Growth-break case: faster easing

If growth or labor deteriorates abruptly across multiple indicators, policy can shift earlier than current pricing suggests.

Count the directions this grid actually points: of the three scenarios, two — the base case and the sticky-inflation case — resolve toward later or fewer cuts, and only one, the growth-break case, resolves toward faster easing. That is a two-of-three, roughly 67%, tilt of the framework's own branches toward delay before any probability is assigned. The missing input is the weight the reader's own market data puts on each branch — the priced number of 2026 cuts and the priced timing of the first one are the figures worth pulling, and we do not plug in a feed we cannot source here. Until those weights argue otherwise, the grid's structure is not symmetric: it leans toward patience, not toward speed.

The value of this grid is not prediction certainty. It is exposure discipline under multiple plausible paths.

Risk Discipline Before the First Confirmed Cut

A practical risk framework can be kept simple and repeatable:

- Set event-week sizing rules in advance of CPI and policy meetings.

- Keep concentration limits explicit, especially in rate-sensitive sectors.

- Separate one-day macro reactions from multi-quarter earnings revisions.

- Re-test downside scenarios after each major macro release.

- Rebalance on schedule rather than on narrative intensity.

Related tools: use the position size calculator to translate event-week risk limits into share counts, and the portfolio rebalancing calculator to keep rate-sensitive exposure close to a target weight after macro moves.

Data Triggers to Monitor Between Meetings

Use a fixed checklist between FOMC dates:

- CPI/PCE trend persistence rather than single-month surprises.

- Labor-market direction across payrolls, unemployment, and wage momentum.

- Credit-spread behavior as a stress signal for growth-sensitive assets.

- Policy communication consistency across statements and speeches.

When the same signal repeats across releases, confidence should increase. When signals conflict, position sizing should stay conservative.

How to Read the Calendar Without Overfitting

The calendar is useful because it forces a sequencing discipline. A CPI release before a policy meeting can change the probability distribution, but it does not automatically create a policy decision. The committee still has to compare inflation composition, labor-market breadth, and financial conditions against the risk of easing too early.

That is why the FOMC calendar and the CPI release page should be read together. The calendar tells investors when the committee can act. The CPI page tells investors when one of the key inputs can change the debate. Neither source, by itself, is a complete signal.

For portfolios, this distinction matters. A rate-sensitive position can look attractive after one softer inflation print, but the risk budget should still reflect the next labor release, the next inflation print, and the next policy communication window. The cleaner process is to update scenario weights after each release, then wait for repeated confirmation before changing the base-case allocation.

This also keeps macro views from becoming stale. If inflation improves but credit spreads widen, the portfolio read is no longer just "when will cuts arrive?" It becomes whether the path to cuts is orderly or stress-driven.

What Changes the Fed-Cut Case

In 2026, the dominant error is still binary framing: either "cuts now" or "no cuts at all." A more useful framework is conditional policy. Easing is possible, but timing depends on repeated confirmation.

For risk management, the durable edge comes from process quality: calendar discipline, data confirmation, and scenario-based controls.