The REIT Comeback: Why Real Estate Could Be 2026's Surprise Winner

Data center REITs are crushing it, office is still bleeding, and rate cuts could turbocharge the entire sector. Here's why REITs deserve a spot on your radar in 2026.

Hynexly

The Asset Class Nobody's Talking About

While everyone's been obsessing over AI stocks and crypto, one of the oldest asset classes in existence has been quietly setting up for a major run. I'm talking about REITs — Real Estate Investment Trusts — and I think 2026 could be the year they remind everyone why they belong in a diversified portfolio.

The REIT index got absolutely crushed in 2022-2023 as rates spiked. Most investors wrote off the entire sector. But here's the thing: not all real estate is created equal. And the divergence happening right now within the REIT universe is one of the most interesting stories in markets.

Let me walk you through what's happening — and where I think the opportunities are.

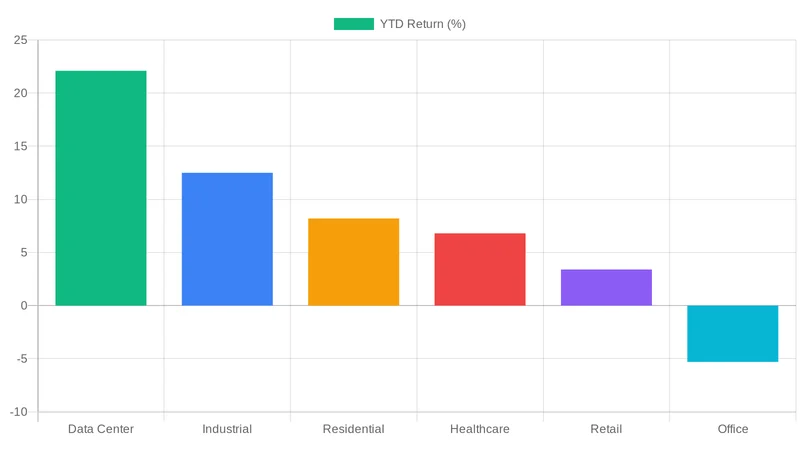

The Great REIT Divergence

Look at this chart and tell me REITs are boring:

What you're seeing is a sector that's splitting into clear winners and losers. Data center REITs are absolutely ripping. Industrial and healthcare REITs are holding their own. Residential is grinding higher. And office? Still in the gutter.

This isn't random — it reflects structural shifts in the economy that aren't going away anytime soon.

Data Center REITs: The Undisputed Champions

If there's one subsector I'd pound the table on right now, it's data center REITs. The AI boom has created a demand surge for computing infrastructure that is genuinely unprecedented.

Equinix and Digital Realty — the two heavyweights — are seeing leasing activity at levels they've never experienced before. Hyperscalers like Microsoft, Amazon, and Google are signing massive deals for data center capacity to power their AI workloads. And the supply side simply can't keep up.

New data center construction takes 18-24 months, requires enormous power capacity, and faces permitting bottlenecks. Meanwhile, AI compute demand is doubling roughly every 12 months. That supply-demand imbalance translates directly into pricing power and rising rents.

The kicker? Data center REITs aren't even that expensive relative to their growth. Equinix trades around 25x FFO, which sounds steep until you realize they're growing AFFO at 8-10% with a visible pipeline stretching years into the future.

The Housing Shortage: A Structural Tailwind

On the residential side, the US housing market remains chronically undersupplied. We're short an estimated 4-5 million homes after a decade of underbuilding following the 2008 financial crisis. That deficit isn't going away quickly.

For residential REITs — think apartment operators like AvalonBay and Equity Residential — this means sustained occupancy rates and rent growth. People need somewhere to live, and if they can't buy (because mortgage rates are still elevated and home prices haven't corrected), they rent.

Single-family rental REITs like Invitation Homes and American Homes 4 Rent are also benefiting. The suburban rental market has exploded as families who are priced out of homeownership turn to renting houses instead of apartments.

The Office Problem (And Why It's Not the Whole Story)

Yes, office REITs are struggling. Remote and hybrid work have permanently reduced office space demand in many markets. Vacancy rates in cities like San Francisco, Chicago, and Manhattan are at multi-decade highs.

But here's what I want to push back on: the office implosion is real but it's been priced in — aggressively. Many office REITs are trading at 40-60% discounts to their pre-pandemic valuations. The worst operators will continue to bleed, but the best — those with Class A properties in strong markets — are starting to see stabilization.

I wouldn't go overweight office, but writing off the entire subsector at these valuations feels like the wrong call to me.

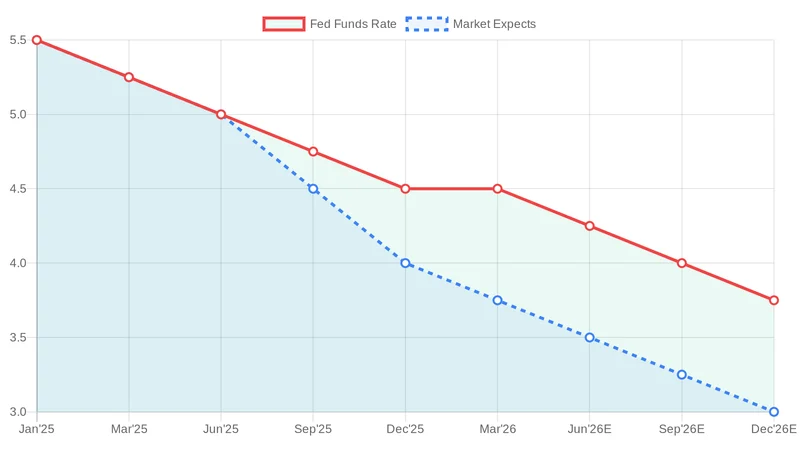

The Rate Cut Catalyst

Here's the potential game-changer that most people are sleeping on: rate cuts.

REITs are extremely sensitive to interest rates. When rates go down, three things happen simultaneously:

- Borrowing costs drop — REITs are leveraged vehicles, so cheaper debt goes straight to the bottom line

- Yield spreads widen — a 4% REIT dividend yield looks a lot more attractive when Treasuries pay 3.5% versus 5%

- Cap rates compress — property values mechanically increase when discount rates fall

The Fed has signaled two cuts in 2026. If the economy softens enough for them to deliver, REITs could see a meaningful re-rating. The sector historically outperforms in the 12 months following the first rate cut by an average of 15-20%.

How I'm Playing It

My approach is simple: overweight the structural winners, be selective on everything else, and avoid the value traps.

Core positions: Data center REITs (Equinix, Digital Realty) and residential REITs (AvalonBay, Invitation Homes). These benefit from secular trends regardless of the macro environment.

Opportunistic: Healthcare REITs (Welltower) and industrial REITs (Prologis). Both are positioned for steady growth with rate-cut upside.

Avoiding: Low-quality office and retail REITs that are cheap for a reason.

A broad REIT ETF like VNQ works if you want diversified exposure, but I prefer being selective because the performance dispersion within the sector is enormous right now.

The Bottom Line

REITs have been the forgotten asset class for two years. That's exactly when I start getting interested. The combination of data center demand, a structural housing shortage, and potential rate cuts creates a setup that could make real estate one of 2026's best-performing sectors.

The key is selectivity. Not all REITs are created equal — the gap between winners and losers has never been wider. Pick the right subsectors and you could be looking at strong total returns from both price appreciation and dividends.

Real estate isn't sexy. But neither was buying anything in March 2020. Sometimes the best trades are the ones nobody's excited about.

Not financial advice. I hold positions in several REITs mentioned above.