Green Transition

The KRBN Wrapper Is the First Check Before Carbon Credit Exposure

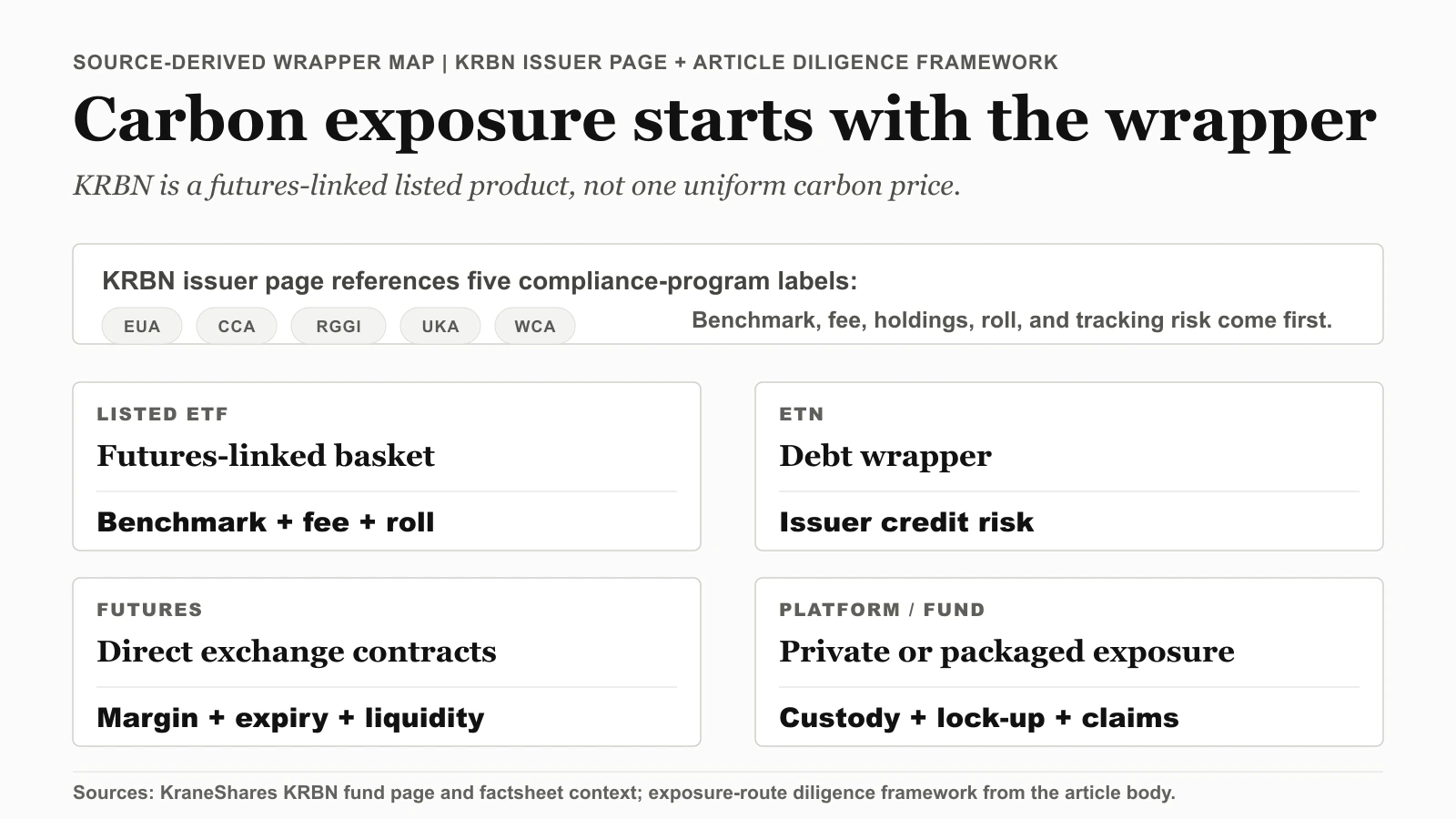

Carbon exposure isn't one product. Due diligence on carbon-credit ETFs, futures, platforms, and private vehicles in 2026 — structure, liquidity, regulation, and risk controls first.

Thesis

(Source: KraneShares KRBN fund page)

Pinning down what "carbon-credit exposure" actually means came first. For KRBN, the issuer's own words supply the definition — the S&P Global Carbon Credit Index benchmark plus exposure spanning EUA, CCA, RGGI, UKA, and WCA — and because both the fund page and the factsheet PDF spell that out, we let those two documents carry the evidentiary load for this page. Narrow webpage crops and single-market screenshots were set aside deliberately; a basket tied to five compliance programs cannot be honestly checked from one cropped figure. And where a claim was really about policy mechanics, it went back to the CBAM and global-carbon-markets pages rather than being restated here.

The carbon series has already worked through the EU ETS, global carbon markets, CBAM, and the voluntary carbon market. This article focuses on the implementation map and the due diligence questions behind each access route.

A practical reader question is: "Which carbon-credit exposure route is actually being evaluated?" Unlike broad equity index exposure, carbon products still require extra product diligence before the theme can be treated as an investable category.

Source Evidence Snapshot

The source stack focuses on product-wrapper diligence rather than repeating policy screenshots from the rest of the carbon series.

| Source | What to verify | Why it matters |

|---|---|---|

| KraneShares KRBN fund page | The fund benchmark, strategy description, expense information, and current exposure table. | KRBN is a futures-linked wrapper, so the issuer page is the first stop for understanding what the ticker actually packages. |

| KraneShares KRBN factsheet PDF | The issuer's report-style summary of the benchmark, fund details, expense ratio, and covered carbon allowance programs. | A static factsheet is cleaner evidence than a narrow webpage crop when checking the product wrapper. |

| S&P Global Carbon Credit Index context from the issuer page | Which compliance programs are referenced, including EU allowances, California allowances, RGGI, UK allowances, and Washington carbon allowances. | A broad carbon ETF is not a single carbon price; it is a basket tied to multiple regulatory systems. |

| Global carbon markets comparison | Regulator and auction-result pages for EU ETS, California, RGGI, and China ETS. | The product wrapper should be checked against the underlying market structures it claims to package. |

This guide keeps the proof layer centered on access vehicles. CBAM regime mechanics and EU ETS calendar details belong in the dedicated CBAM and global carbon markets pages, so the same official evidence role does not repeat across the series.

Product Landscape: Compliance vs. Voluntary

Before diving into specific products, you need to understand the two distinct arenas you can invest in.

For many retail readers, compliance-market products are the first area to research because they are generally more accessible, more liquid, and have clearer policy drivers than voluntary-credit exposures. That does not make them automatically suitable.

Route 1: Carbon ETFs (Most Transparent Public Wrapper)

A listed carbon ETF trades exactly like a stock, but that familiarity is the trap: the wrapper is operationally simple while what it holds is not. The question that actually matters is not whether the ticker trades easily; it is which carbon markets, futures rolls, fees, and tracking differences sit underneath. KRBN makes the point concrete — on the 2026-04-02 issuer exposure table, EU Allowances (EUA) were the single largest component, so a buyer at that date was, in practice, taking a EUA-weighted position across a five-program basket rather than an evenly split bet on global carbon prices. That weighting is a snapshot, not a fixed rule, and the issuer table is the field a reader should re-pull before treating the basket as balanced.

KraneShares Global Carbon ETF (KRBN)

KRBN is one of the most visible listed vehicles for compliance carbon exposure. On the issuer page, it is benchmarked to the S&P Global Carbon Credit Index and references major cap-and-trade programs, including:

- EU Allowances (EUA)

- California Carbon Allowances (CCA)

- RGGI

- UK Allowances (UKA)

- Washington Carbon Allowances (WCA)

It trades on the NYSE like other ETFs and packages carbon allowance futures exposure into one ticker.

What to know:

- KRBN invests in carbon allowance futures, not physical allowances, which introduces roll costs and tracking error

- As of 2026-04-02 on the issuer exposure table, EUA was the largest component; that composition can change

- Expense ratio matters, so check the current fee and compare it to alternatives

- Like any futures-based product, contango (when futures prices are higher than spot) can create a drag on returns over time

Carbon ETNs

Exchange-traded notes (ETNs) are another route. Unlike ETFs, ETNs are debt instruments, so holders carry issuer credit risk in addition to carbon-market risk.

Other Carbon ETFs

The ETF landscape is evolving. There are now products that focus on specific carbon markets (EU-only, California-only) and others that blend carbon with broader climate-related investments. The space is still small enough that KRBN dominates, but competition is growing.

Route 2: Carbon Futures (Institutional-Style Exposure)

Carbon futures on exchanges like ICE (Intercontinental Exchange) are the institutional route for direct market exposure, but they sit outside the normal beginner-product set.

EU carbon allowance futures (EUA futures) trade on ICE Endex. California carbon allowance futures trade on ICE as well. These are standardized contracts with defined expiration dates, and they are the instruments institutional participants and compliance buyers actually use.

What futures change:

- More direct price exposure than an ETF wrapper

- Leverage and margin mechanics

- Higher liquidity in the EU ETS market than in smaller carbon markets

- Exchange contract specifications instead of a fund expense ratio

Why be cautious:

- Futures require a margin account and understanding of contract specifications

- Contracts expire, so you need to roll positions, which has costs

- Leverage amplifies losses just as readily as gains

- Not suitable for passive, set-it-and-forget-it investing

- Minimum position sizes may be too large for small accounts

For most retail research workflows, the practical point is that futures are a complexity benchmark: if the ETF or platform exposure cannot be explained relative to the underlying futures market, the product is probably not yet understood well enough.

Route 3: Specialized Carbon Platforms

A growing number of platforms advertise carbon-credit access for individuals. These range from marketplace-style platforms that claim direct credit ownership to fintech apps that package carbon exposures.

Some platforms focus on compliance allowances and claim smaller-increment access to EU or California allowances. Others focus on voluntary credits or packaged baskets of verified carbon offsets.

What to look for:

- Regulatory status and investor protections

- Fee structure (transaction fees, custody fees, spread)

- What you actually own, because some platforms sell credit-linked tokens or derivatives rather than actual allowances

- Liquidity, including whether secondary-market exits are clearly documented

- Track record and counterparty risk

This space is still maturing. Platform claims require careful due diligence before treating the exposure as investable.

Route 4: Private Carbon Funds

For accredited or institutional buyers, private funds focused on carbon credits have been emerging. These funds typically take a more active approach, including allowance purchases, carbon-credit project finance, or strategies that aim to capture specific carbon-market dynamics.

Some focus on the compliance-voluntary arbitrage. Others invest directly in CDR technology companies or carbon credit originators. A few are structured as venture capital funds targeting early-stage carbon market infrastructure.

The minimum commitments are typically substantial (six figures and up), and the lock-up periods can be long. For eligible buyers with the capital and time horizon, these funds can expose parts of the carbon market that public products do not easily package.

Carbon as a Diversification Claim to Test

The diversification argument is a hypothesis to test, not a conclusion to assume.

Carbon prices can respond to regulatory decisions, weather-linked energy demand, industrial output, and climate-policy calendars rather than the same variables that drive broad equity indexes.

That difference makes carbon exposure researchable as a diversification candidate, but it does not make the outcome automatic. Carbon is a younger asset class with limited long-run history, and correlation patterns can change under systemic stress. Treat diversification as a potential benefit, not a guaranteed allocation result.

The Structural Case for Carbon Prices

The structural case for carbon prices usually rests on two mechanics:

Supply is mechanically tightening. In compliance markets, the cap on allowances ratchets down every year by law. This creates a policy-defined scarcity path.

Demand is structural. Companies need allowances to operate. This is compliance-driven demand rather than discretionary demand.

Product Risks to Check Before Exposure

Risk factors deserve equal weight:

Regulatory Risk

This is the big one. Carbon markets exist because governments created them. What governments create, they can modify or dismantle. A shift in political priorities, recession fears, competitiveness concerns, or changes in government could lead to looser caps, more free allowances, or even policy reversal.

This risk is often assessed as lower in the EU than in many other jurisdictions because of deeper institutional support, but it is not zero. In the US, state-level programs can be more exposed to political turnover.

Price Volatility

Carbon prices can re-rate quickly on policy reviews, auction outcomes, energy shocks, and macro demand changes. Large drawdowns and sharp rebounds are both possible.

Liquidity Risk

While the EU ETS is liquid, smaller markets (RGGI, voluntary markets, emerging market systems) can have thin trading volumes. Getting in is one thing; getting out at a fair price when you need to can be another.

Product Complexity

ETFs based on futures contracts behave differently from spot exposure. Roll costs, contango, and tracking error can significantly impact returns. Make sure you understand the product mechanics before investing.

Oversupply Scenarios

If policymakers increase free allocations, adjust market-stability mechanisms, or delay tighter caps, scarcity can ease and prices can weaken.

Due Diligence Checklist

For readers researching carbon exposure for the first time:

1. Compare listed ETPs first. A KRBN-like product is easier to review than direct futures or private platforms because fees, holdings, and market prices are public. That convenience does not remove futures-roll, liquidity, or tracking risk.

2. Understand what you own. Read the ETF prospectus. Know which markets are included, how futures rolling works, and what the fee structure is. This is not a set-and-forget asset class.

3. Keep the time horizon explicit. The structural case for carbon prices is tied to multi-year policy pathways. Short-term trading around policy announcements is specialist territory.

4. Watch the regulatory calendar. EU ETS review decisions, CBAM implementation updates, and national carbon pricing launches can move markets.

5. Keep the exposure framework conservative. No matter how strong the carbon-policy thesis appears, regulatory risk alone justifies conservative treatment.

6. Consider the tax implications. Carbon futures and ETFs may have different tax treatments depending on your jurisdiction. Consult a tax professional, especially for direct futures positions.

What Changes the Carbon-Exposure Framework

Carbon credits remain one of the more policy-linked and structurally constrained market themes, with long-term tailwinds from cap tightening and continued decarbonization policy.

At the same time, this asset class requires more product work than plain-vanilla equity ETFs. Regulatory, liquidity, and futures-structure risks are all material.

Practical takeaway: stay within products you can explain end-to-end, keep the exposure framework conservative, and evaluate outcomes over multi-year horizons rather than quarter-to-quarter moves.

Series Context

Carbon credits are no longer just a niche curiosity. They have real infrastructure, growing liquidity in some venues, and a policy-linked growth story. The menu of ETFs, futures, platforms, and funds is broader than it was, but a wider menu does not lower the need for product-level diligence.

The key is matching the vehicle to knowledge level, risk tolerance, and time horizon while staying clear about what each product actually owns.

This closes the five-part carbon credits series. Readers who worked through the EU ETS deep dive, global markets, CBAM, and the voluntary market now have a practical baseline for product-level diligence.