Market & Macro

Robinhood Stock in 2026: Tokenization Optionality Versus Crypto Regulation Evidence

A 2026 Robinhood stock review that separates market context, the existing earnings base, 10-K crypto-regulation language, and SEC tokenization optionality.

(Sources: Google Finance HOOD quote page, Robinhood 2025 Form 10-K via SEC iXBRL viewer, SEC Crypto Task Force submission from Robinhood on tokenization, SEC Form 4 for Paula Loop dated April 1, 2026)

Thesis

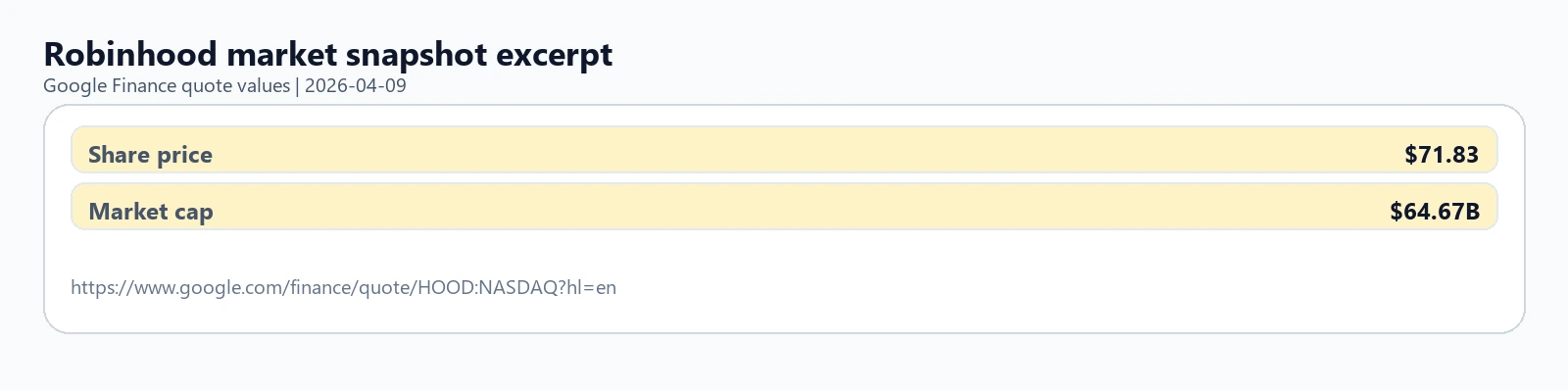

Robinhood is not a small overlooked broker anymore. The captured quote page showed HOOD at $71.83 and about $64.67 billion of market value on April 9, 2026. The burden of proof has shifted from "is this a real business?" to "can the platform earn a broader multiple than a retail broker?"

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

The falsifiable call is that the next valuation step depends less on generic crypto-trading volume and more on whether Robinhood can turn regulatory clarity into a tokenized-securities distribution layer. If 2026 brings clearer rules but no product evidence, no custody progress, and no sign that tokenized assets can reach mainstream brokerage users, the premium should be treated as optionality that was pulled forward.

Source Evidence Snapshot

The hero image carries the price and market-cap context. The body evidence keeps two non-overlapping regulatory layers: Robinhood's 10-K crypto legislation language and its SEC tokenization policy position. The current earnings base remains a source note because it comes from the same Google Finance surface as the hero.

Source note: Google Finance HOOD quote page, captured 2026-04-09. The visible quarterly financials panel showed Q4 2025 revenue and net income, which establish the existing earnings base before any tokenized-securities contribution is proven.

What the Street is Pricing

The market is already paying for more than a normal brokerage recovery. The quote snapshot's valuation context, plus the 2025 operating base, implies Robinhood is being valued as a platform that can benefit from active trading, crypto demand, and future regulatory openings at the same time.

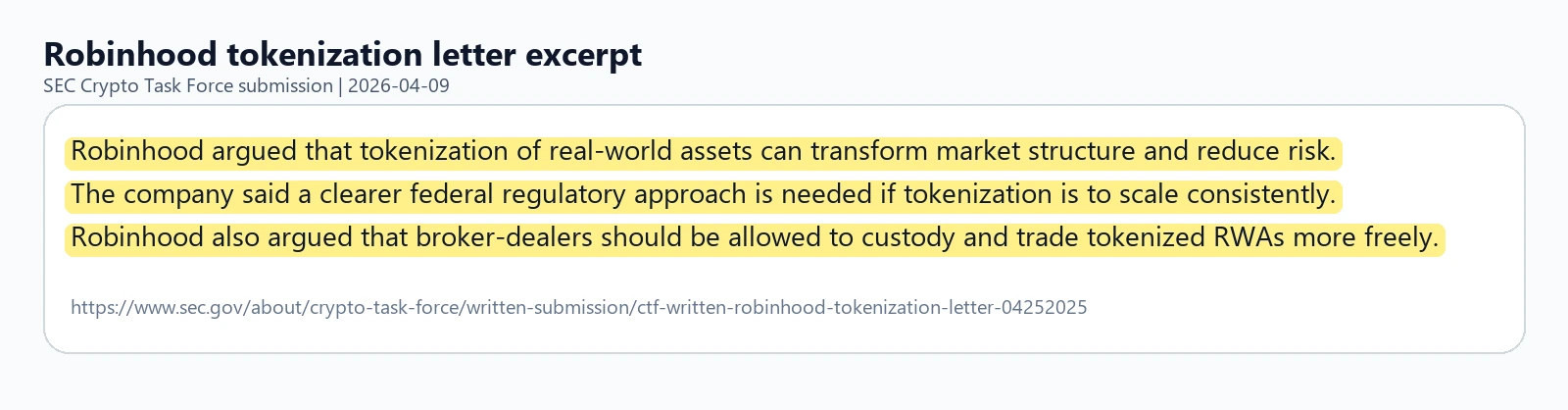

Public consensus data were not in the retained evidence for this print, so the article does not import an outside valuation range. The cleaner interpretation from the available sources is that HOOD is pricing an option, not a disclosed revenue stream. The option is that digital-asset legislation becomes usable and Robinhood's consumer distribution gives it a natural place in tokenized stocks, funds, private assets, or other on-chain wrappers.

That distinction matters. Crypto transaction revenue is already part of the business. Tokenized securities are not yet proven at scale. A premium multiple can be justified only if the company keeps converting regulatory positioning into actual products and usage.

There is a practical way to keep that optionality honest. Treat every regulatory headline as a checklist item, not as revenue. The checklist is simple: broker-dealer permission, custody treatment, eligible asset types, customer access, economics per transaction, and whether the product expands wallet share beyond Robinhood's existing active-trader base. Until several of those boxes are visible in company disclosures, the tokenization story should stay in the "future platform" bucket.

Risks to the Thesis

| Risk | Confirming signal |

|---|---|

| Regulation moves slower than the share price | CLARITY, GENIUS, or related market-structure rules remain fragmented, delayed, or too narrow for mainstream broker-dealer product launches. |

| Tokenization stays narrative-only | Robinhood keeps filing policy letters but does not show product rollouts, custody capability, volume, or customer adoption. |

| Core earnings cool before the option pays | The brokerage and crypto revenue base weakens before tokenized-securities revenue can become visible. |

| Insider evidence is overread | The reviewed Form 4 showed transaction code M, not a clean open-market purchase code P; it should not be used as a discretionary insider-demand signal. |

The biggest risk is timing. The available evidence supports strategic optionality, but it does not show current tokenization revenue. If the market prices that option as if it is already a business line, the stock becomes vulnerable to any delay in rulemaking or product execution.

What Flips the Call

The next trigger is not another generic crypto headline. It is evidence that Robinhood is moving from policy posture to product surface.

The call becomes stronger if Robinhood discloses a compliant tokenized-asset product path, clearer broker-dealer custody mechanics, or usage data that links existing brokerage users to tokenized securities. It becomes weaker if 2026 regulation improves in theory but Robinhood's filings and product releases still point only to optionality.

The current evidence supports a narrower conclusion: Robinhood has a real earnings base and a plausible regulatory option. The equity story should not be described as if that option has already converted into revenue. The next disclosure has to close that gap.