Market & Macro

IBM Stock in 2026: Quantum Ambition Versus Software Cash Flow

A 2026 IBM stock review that separates the quantum-computing roadmap from software growth, infrastructure momentum, free-cash-flow support, valuation context, and short-interest positioning.

(Sources: IBM Q1 2026 earnings release, IBM 2025 Annual Report, IBM Quantum Roadmap, IBM Investor Relations events, Nasdaq official quote API, Nasdaq official quote summary API, ChartExchange IBM short interest, MarketBeat IBM short interest, FINRA equity short-interest data catalog)

Thesis

IBM Stock in 2026 is the cleanest public-market way to debate enterprise quantum computing, but the stock should not be analyzed as a pure quantum trade. The falsifiable thesis is narrower: IBM can keep a credible strategic premium only if Software keeps compounding, Infrastructure stays out of decline, and free cash flow continues to expand while quantum milestones move from roadmap language toward demonstrable client value.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

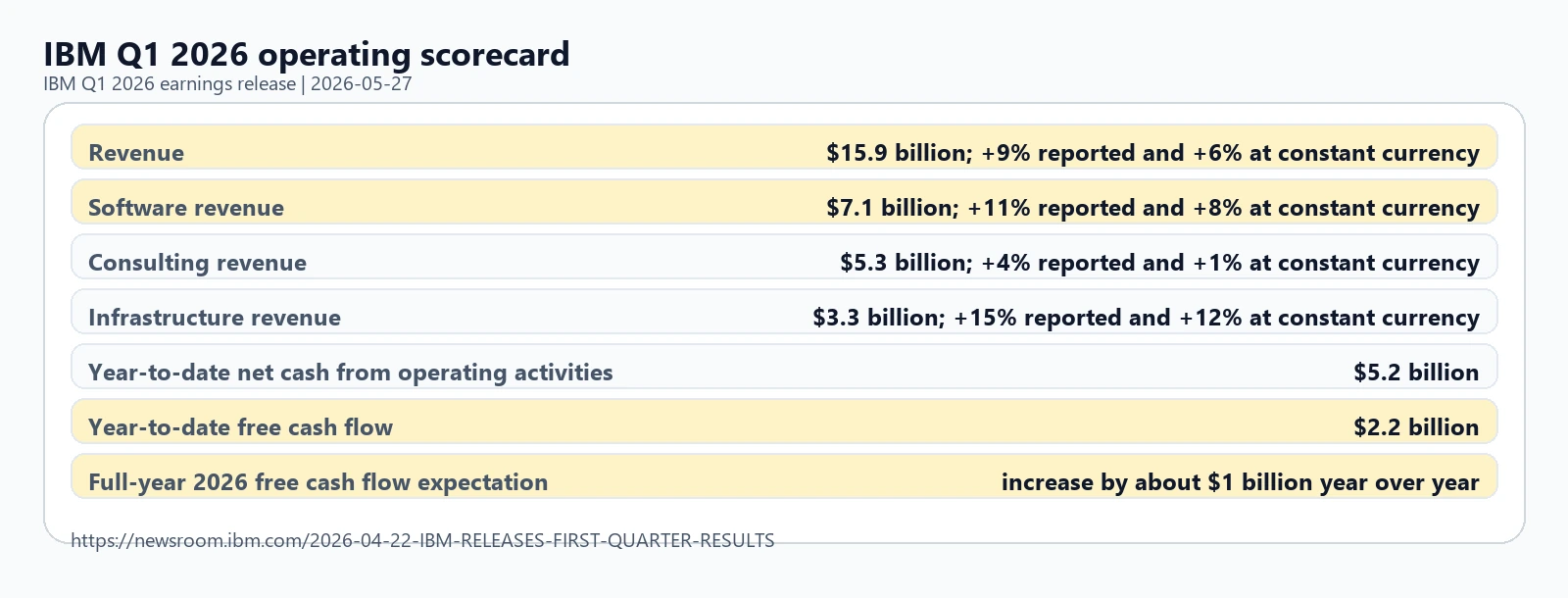

The latest official evidence supports that frame. IBM's Q1 2026 release showed revenue of $15.9 billion, up 6% at constant currency, with Software revenue of $7.1 billion, up 8% at constant currency. Infrastructure was even stronger in the quarter, up 12% at constant currency, while Consulting was only up 1%.

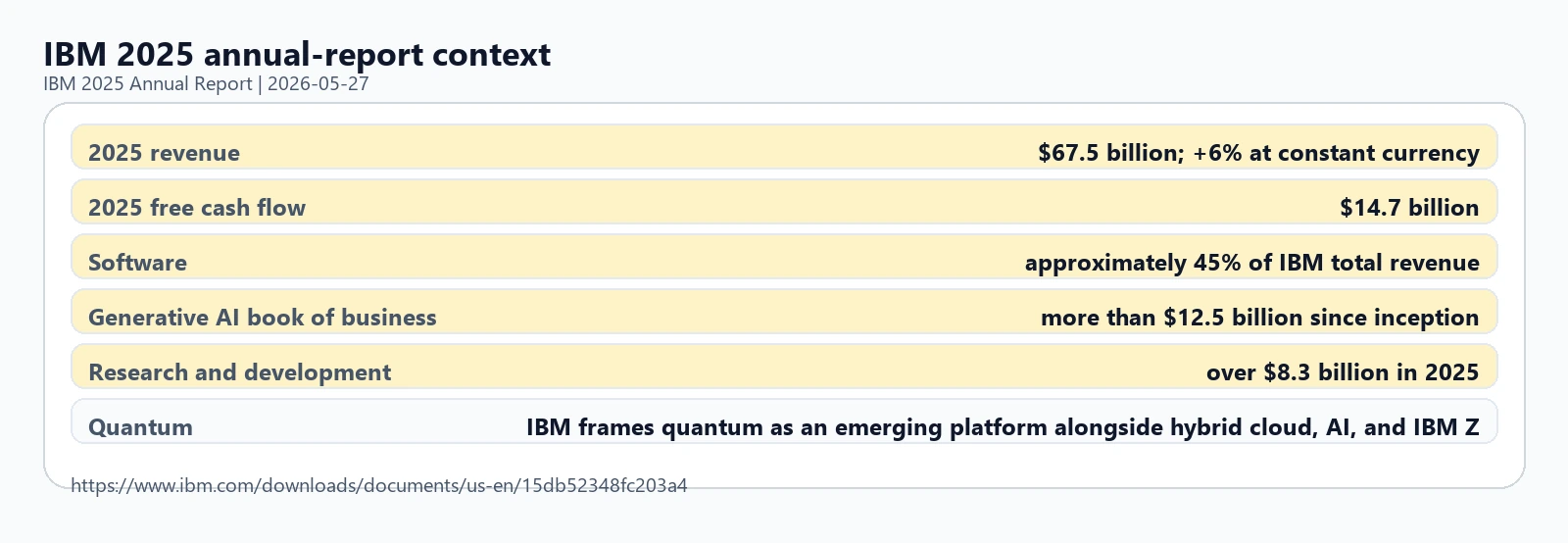

That mix matters. Quantum computing is the story that makes IBM feel newly relevant in 2026, but the current earnings base is still Software, Consulting, Infrastructure, and cash generation. IBM's 2025 Annual Report showed $14.7 billion of free cash flow in 2025, and the Q1 release said management continued to expect 2026 free cash flow to increase by about $1 billion year over year.

The stock case weakens if the next two prints show Software falling below mid-single-digit constant-currency growth or if IBM walks back the full-year free-cash-flow bridge. In that scenario, the quantum roadmap would still be interesting technology, but it would not be enough to underwrite the equity case by itself.

Source Evidence Snapshot

The hero image carries the Q1 operating scorecard. The body evidence keeps four separate roles: current segment growth, cash-flow base, quantum-roadmap timing, and market-positioning context. That structure keeps the article from repeating the same earnings capture while still making the quantum angle visible.

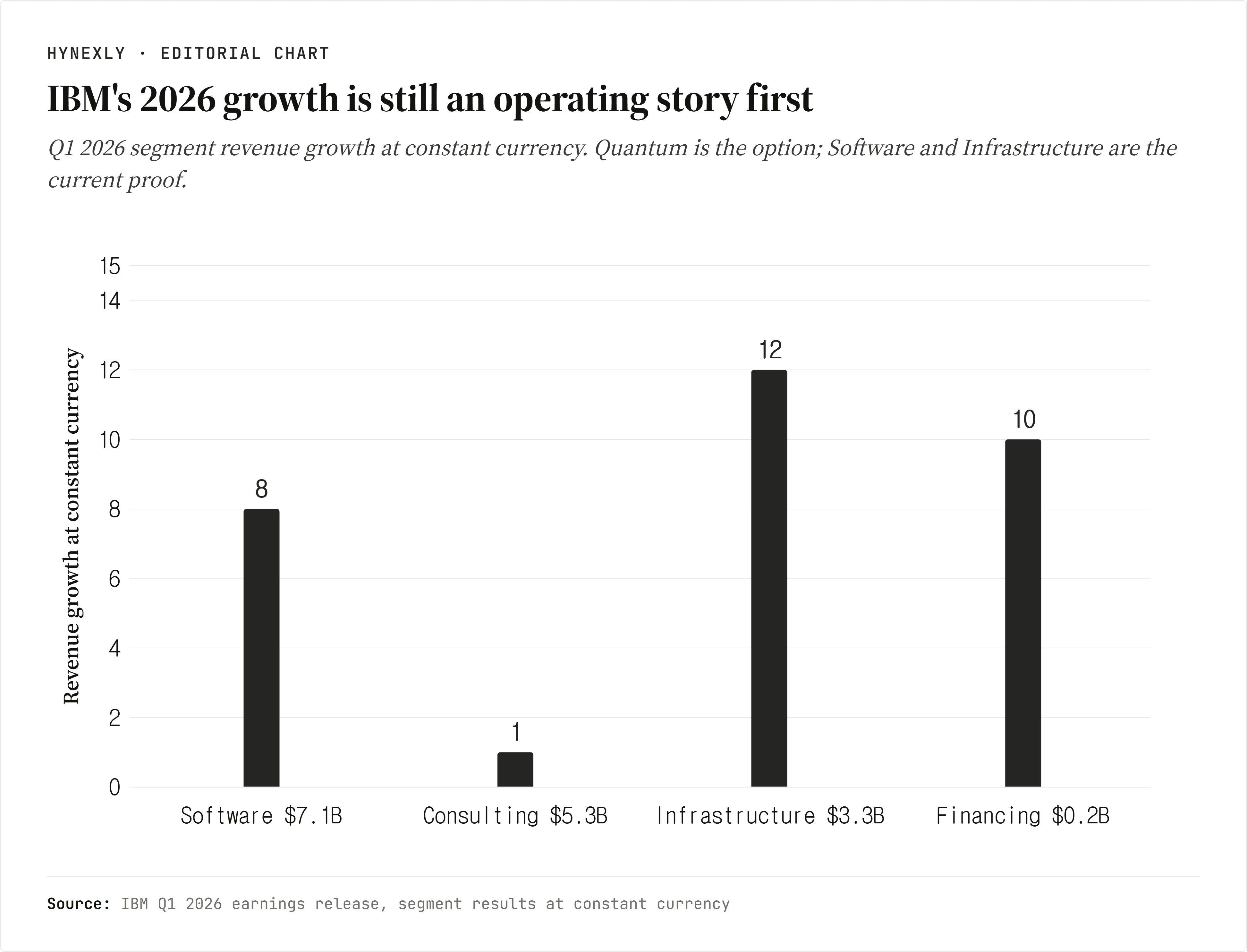

Source chart: IBM Q1 2026 earnings release, captured 2026-05-27. The useful point is the split: Software and Infrastructure carry the operating proof, while Consulting is still a slower line.

The chart explains why IBM is not just a quantum headline. Software grew 8% at constant currency in Q1, and Infrastructure grew 12%. Those are the two lines that give the market something current to underwrite. Consulting at 1% is the watch item because IBM's AI and quantum narrative becomes less powerful if client-services demand stays muted.

IBM's 2025 Annual Report is the better evidence than a product demo because it connects the optionality to the balance sheet. The report showed $67.5 billion of 2025 revenue, $14.7 billion of free cash flow, Software at about 45% of total revenue, and more than $8.3 billion of R&D. That makes quantum a funded option, not a venture-style promise disconnected from current cash generation.

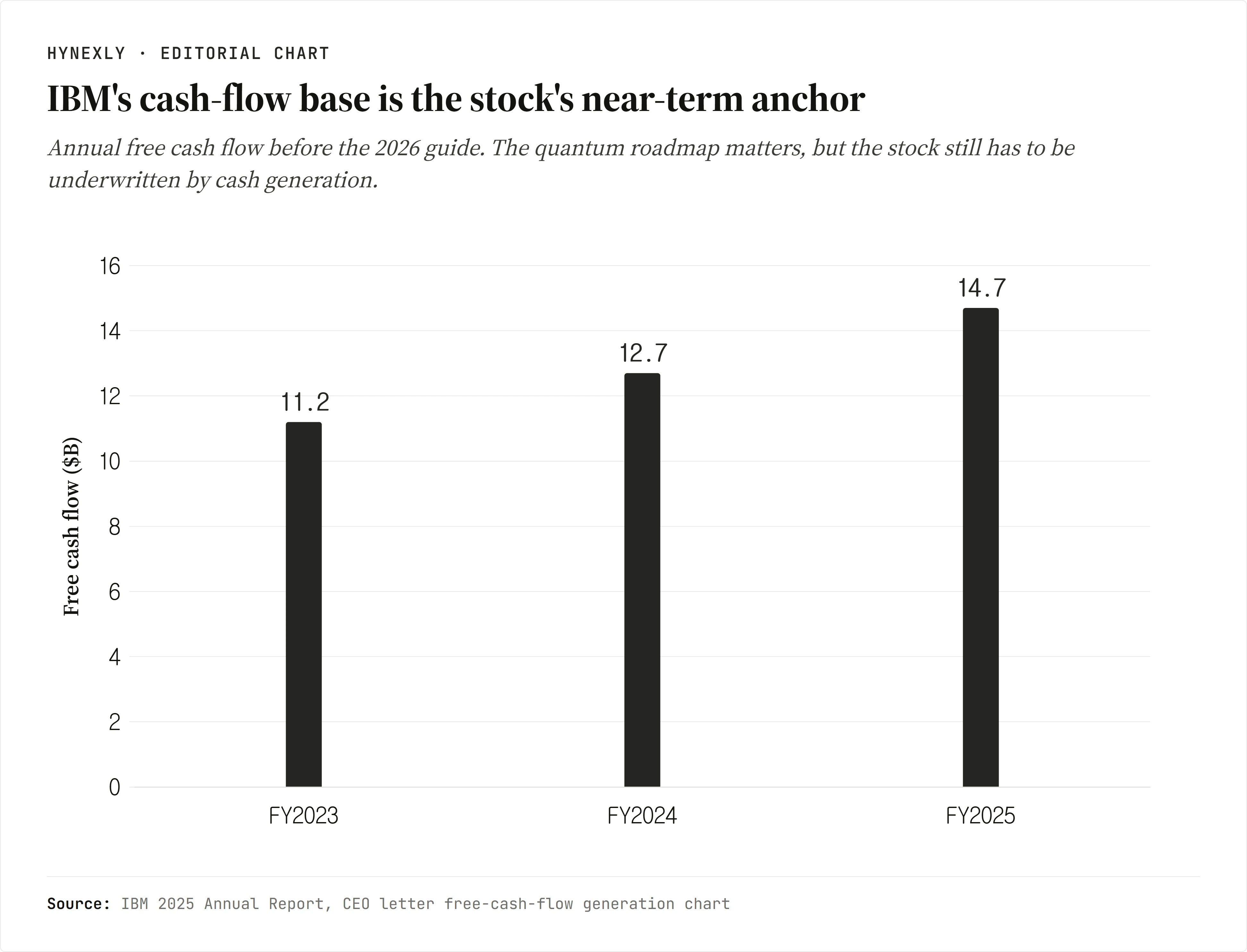

Source chart: IBM 2025 Annual Report, captured 2026-05-27. The chart uses the annual free-cash-flow figures IBM disclosed for FY2023, FY2024, and FY2025.

The free-cash-flow trajectory is the stock's near-term anchor. IBM generated $11.2 billion in 2023, $12.7 billion in 2024, and $14.7 billion in 2025. That is why the 2026 guide matters more than quantum headlines in the next few quarters.

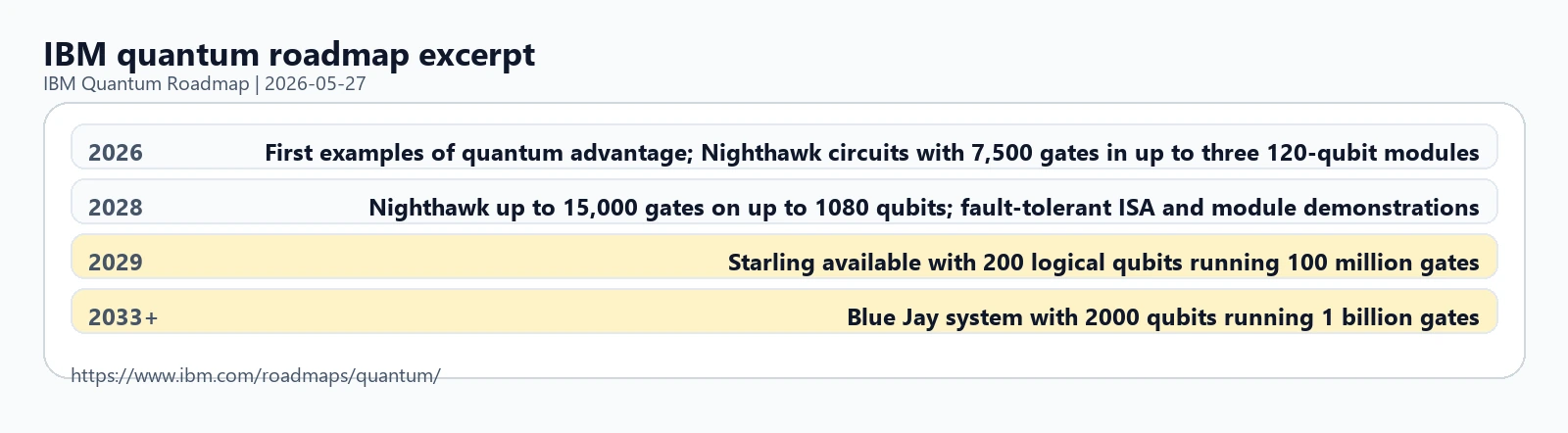

The roadmap is still important. IBM says the community will demonstrate first examples of quantum advantage in 2026, Nighthawk will run circuits with 7,500 gates, and Starling will be available in 2029 with 200 logical qubits running 100 million gates. That is the strategic reason IBM belongs in a quantum-computing discussion. The valuation question is how much credit to give those milestones before the revenue model is visible.

What the Street is Pricing

Nasdaq's official quote response captured on May 27, 2026 showed IBM at $250.69, with a market cap of 235,619,840,843 dollars and a 52-week range of $324.90 to $212.34.

That market cap is roughly 16x IBM's 2025 free cash flow. If IBM delivers the full-year 2026 bridge of about $1 billion of incremental free cash flow, the simple cash-flow multiple would move closer to the mid-teens. That is not a speculative quantum multiple by itself. It is closer to a mature software-and-infrastructure company that has a long-dated technology option attached.

The Nasdaq one-year marker displayed $297.50, but that should be treated as a market-data field, not as an article conclusion. The more useful pricing read is the spread between current cash-flow proof and future quantum optionality. At a roughly $235.6 billion market cap, IBM has room to be valued as a durable software-led cash generator. It does not have room for Software to stall while investors wait for quantum revenue.

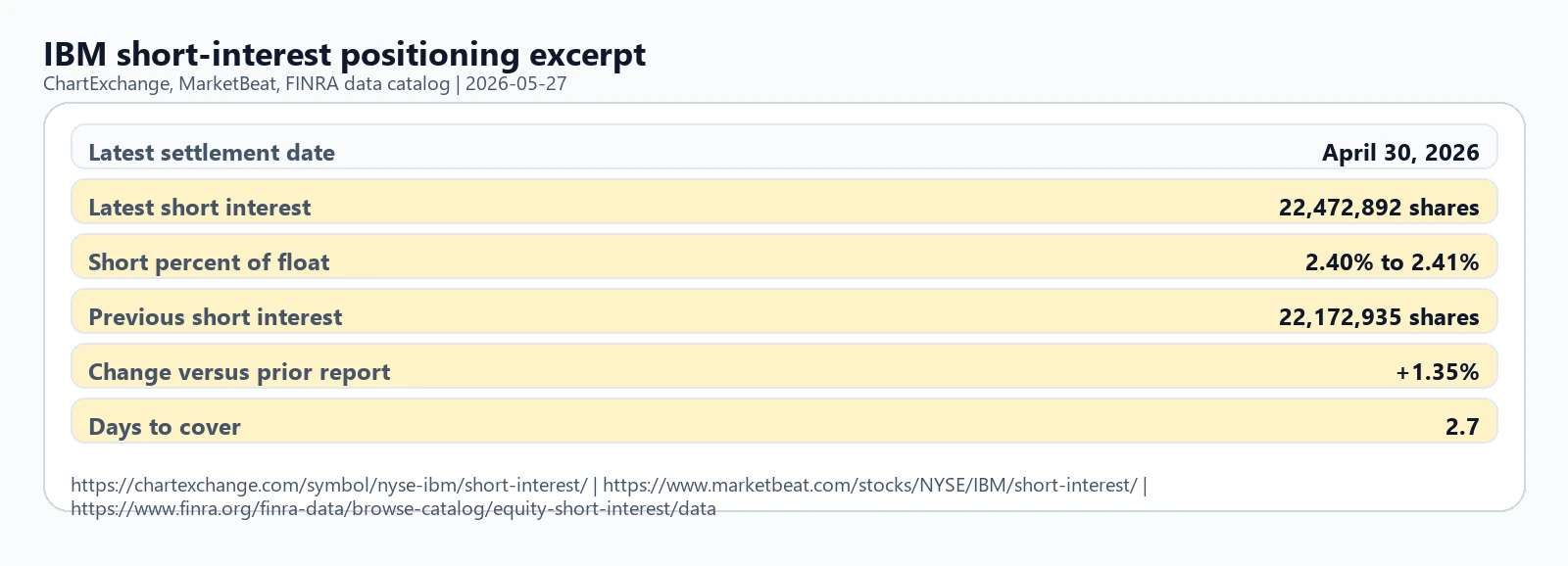

Short interest also argues against making this a positioning-led story.

The retained evidence showed 22,472,892 shares short as of April 30, 2026, or about 2.4% of float, with 2.7 days to cover. That is a useful disagreement marker, but it is not a squeeze-led setup. The stock has to work on operating execution.

Risks to the Thesis

| Risk | Confirming signal |

|---|---|

| Software growth normalizes too quickly | Software revenue growth falls below mid-single digits at constant currency in the next two earnings releases. |

| Free cash flow stops improving | IBM no longer expects 2026 free cash flow to rise by about $1 billion year over year, or Q2/Q3 cash conversion fails to support that bridge. |

| Consulting remains a drag | Consulting stays near 1% constant-currency growth while AI and automation demand fails to convert into visible backlog or revenue acceleration. |

| Quantum stays too far from revenue | The 2026 quantum-advantage milestone produces research visibility but no credible enterprise-use-case evidence that can support future commercial adoption. |

| Balance-sheet flexibility narrows | Debt rises further after acquisitions while cash generation disappoints, making R&D, dividends, and portfolio investment harder to balance. |

The main risk is not that IBM lacks a quantum roadmap. It has one. The risk is that investors assign too much near-term value to that roadmap while the current financial engine shows only modest acceleration.

What Flips the Call

IBM Investor Relations lists the IBM 2Q 2026 Earnings Announcement with a preliminary date of July 22, 2026. That is the next clean checkpoint.

Three numbers carry the weight. First, Software constant-currency growth needs to stay comfortably above the company average. Second, Infrastructure needs to prove Q1 was not just a one-quarter IBM Z-driven spike. Third, free cash flow needs to keep the full-year bridge intact.

The quantum evidence has a different clock. In 2026, the important question is whether IBM can show first examples of quantum advantage with enough specificity that enterprise buyers can understand future use cases. In 2029, Starling is the larger technical milestone. Between those dates, the stock still has to be valued on Software, Consulting, Infrastructure, and cash flow.

That is the practical read. IBM is a legitimate quantum-computing name, but the 2026 equity case is not "quantum wins someday." It is "software-led cash flow keeps funding the option while the roadmap becomes more concrete." If that bridge holds, IBM remains one of the cleaner large-cap ways to follow quantum computing without relying on a pre-revenue pure play. If the bridge breaks, the quantum story becomes a headline rather than a thesis.