Market & Macro

Apple Stock in 2026: iPhone Recovery Versus Buyback Burden

A 2026 Apple stock review that separates valuation pressure, FY26 Q1 category mix, Services margin, operating cash flow, and buyback intensity.

(Sources: Apple FY26 Q1 consolidated financial statements PDF, Apple Investor Relations, Google Finance AAPL quote page)

Thesis

The useful Apple debate in 2026 is no longer whether the business is still elite. The quarter already settled that.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

The useful debate is whether a company this strong, and a stock this large, still has room for another valuation step when so much of the per-share story is being supported by Services mix and one of the biggest repurchase programs in the public market.

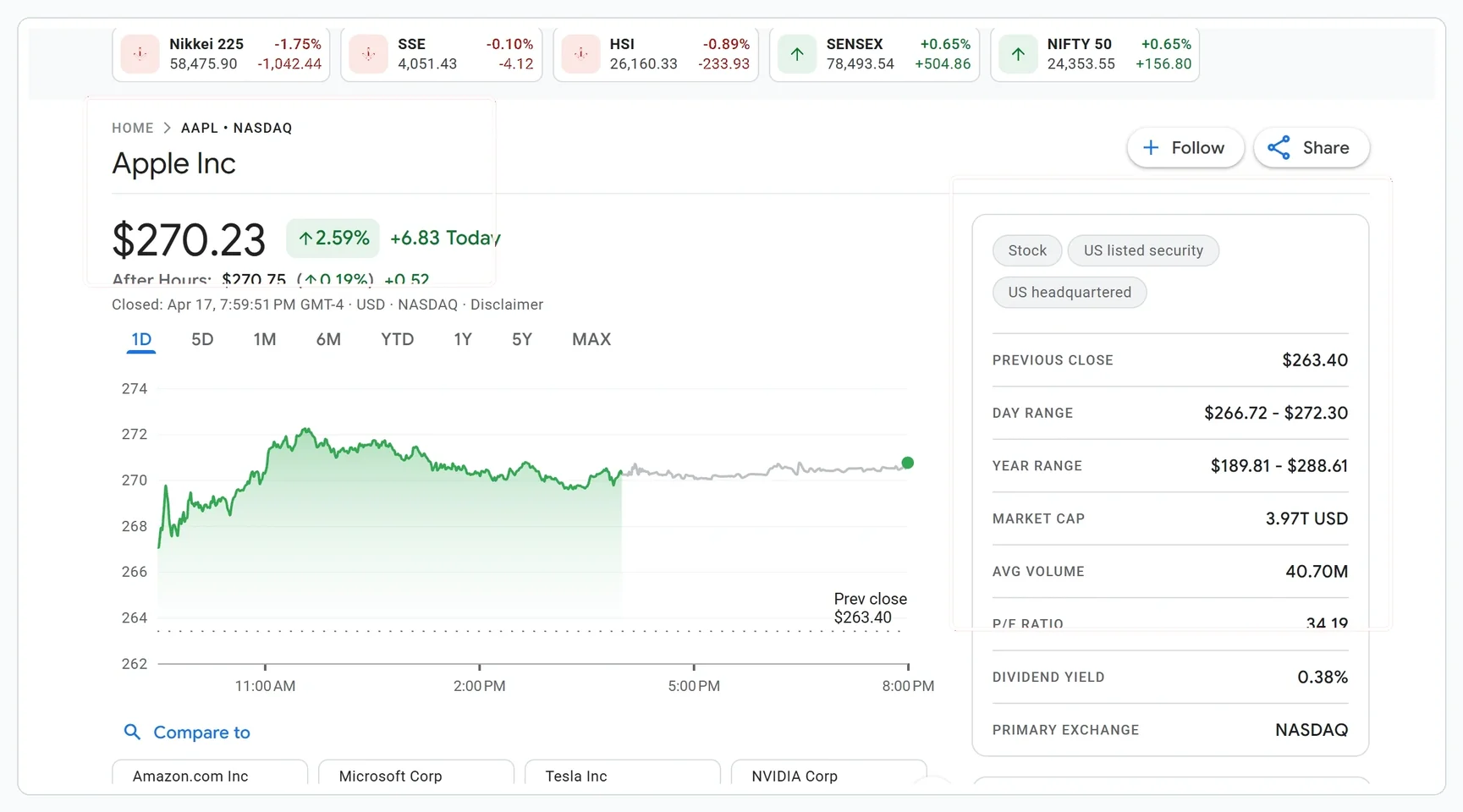

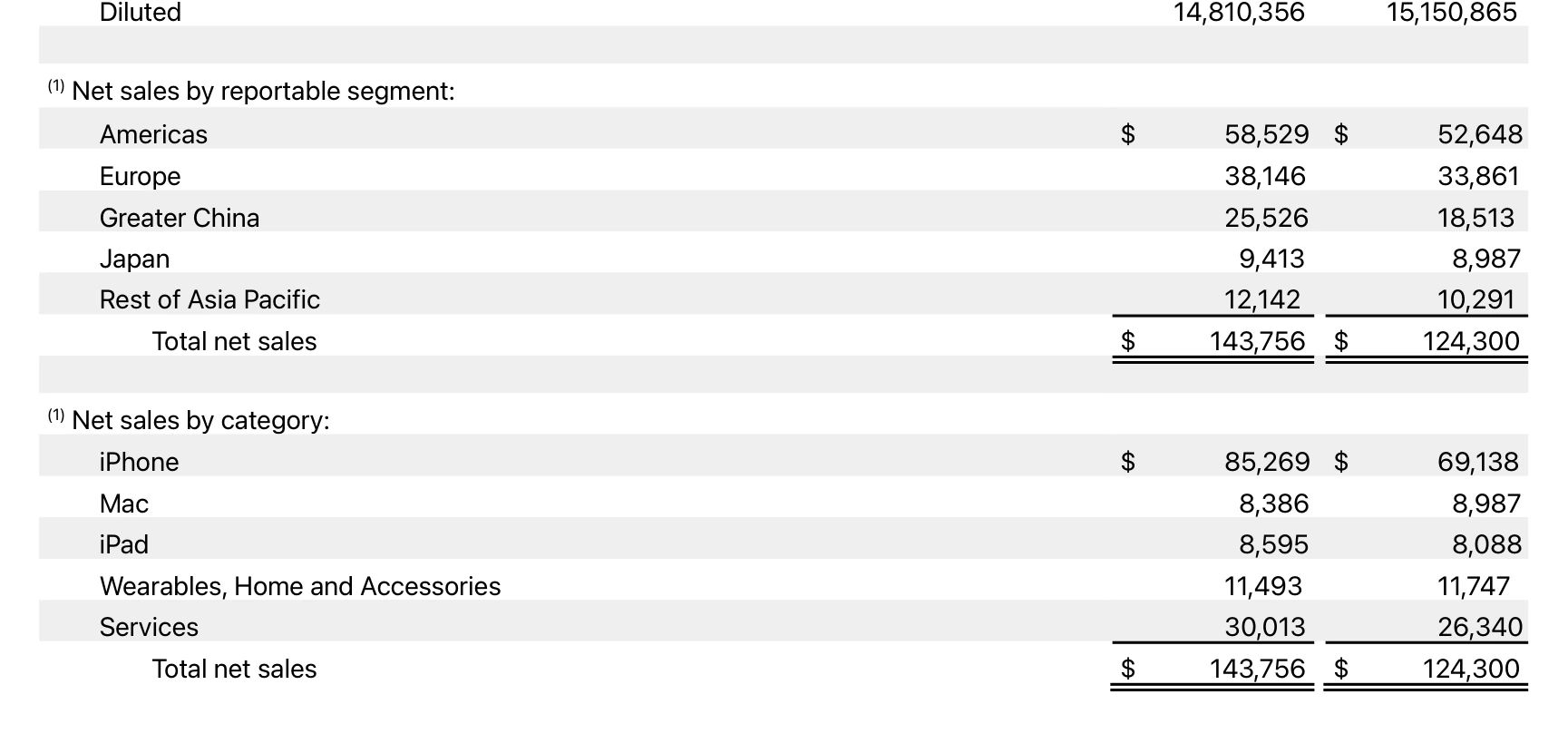

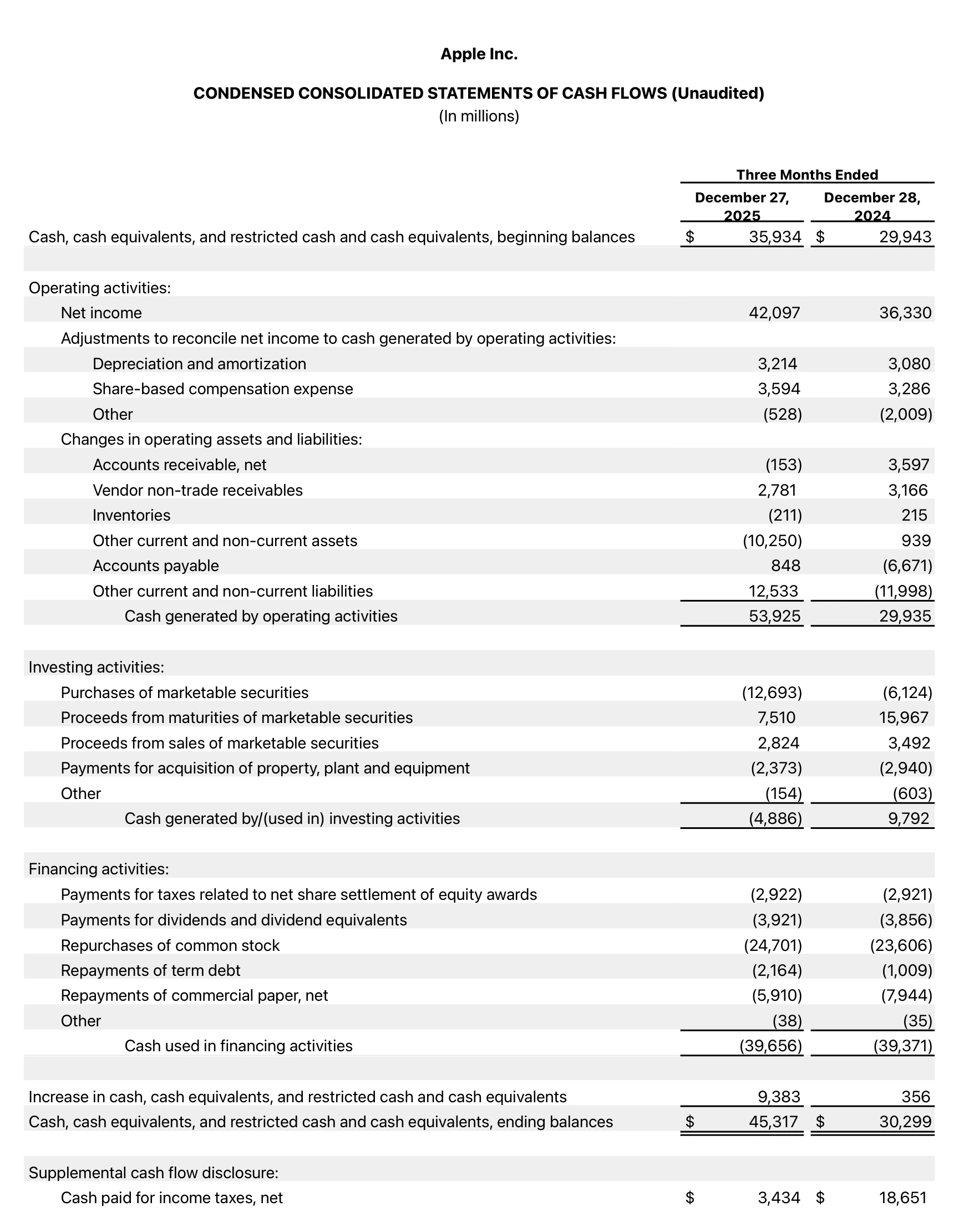

Apple's official FY26 first-quarter release showed $143.8 billion of revenue and diluted EPS of $2.84, both record December-quarter results. The financial statements also showed $85.269 billion of iPhone revenue, $30.013 billion of Services revenue, and $53.925 billion of operating cash flow. Google Finance still showed AAPL at $270.23 at the April 17, 2026 close, with a $3.97 trillion market cap and a 34.19x trailing P/E. That is the setup. Apple is not being valued like a mature name that lost its edge. It is being valued like a premium cash engine that still has to prove how much additional valuation support is left.

That 46.4% figure is the cleanest way to frame the setup. Apple's business is still excellent. But the equity story is still not just about product demand. It is also about how aggressively that demand gets turned into per-share support.

Source Evidence Snapshot

The hero image already carries the Google Finance market-context panel. The body evidence keeps two non-overlapping visual roles: category mix and cash-return proof. Headline revenue, net income, and diluted EPS remain cited as a source note because the category capture already uses the same financial-statement page.

Source note: Apple FY26 Q1 consolidated financial statements PDF, captured 2026-04-19 from page 1. The record December-quarter revenue, net income, and diluted EPS remain the operating baseline; the visual stack avoids showing the same page twice.

This panel matters because it shows the quarter was not carried by one narrow line item. iPhone, Services, and China all mattered at the same time.

This is the evidence that keeps the buyback discussion central. Apple's quarter was strong in the business, but it was also still strong in the capital-return machine.

What the Street is Pricing

The market is pricing Apple as a premium cash engine, not as a tired hardware company. The strongest reason not to get lazy with the Apple bear case is how broad the quarter was.

Apple's FY26 Q1 10-Q said iPhone revenue rose 23% year over year to $85.269 billion, Services revenue rose 14% to $30.013 billion, and Greater China revenue rose 38% to $25.526 billion. That combination is not a cosmetic beat. It says the hardware engine, the high-margin Services engine, and the region investors worry about most all contributed in the same quarter.

This matters because the market does not have to make a heroic assumption to believe Apple's business is still world-class. The official numbers already show that. If only Services had worked, investors could argue the installed base was masking hardware fatigue. If only iPhone had worked, investors could argue the mix was not improving. But the quarter showed both demand and mix strength together.

That does not make the stock automatically cheap. It does make the business easier to trust.

Services margin still supports the premium

The most important line in the Q1 2026 10-Q may be the gross-margin table.

Apple said Products gross margin was 40.7%, Services gross margin was 76.5%, and total gross margin was 48.2%. That spread is one of the clearest reasons Apple still deserves to trade above ordinary hardware companies. Services does not need to become the majority of revenue to matter. It only needs to remain a large enough mix component to keep group profitability unusually strong.

But the same section is also where the nuance lives. Apple said product gross margin improved because of a different mix of products, but that benefit was only partially offsetting tariff costs. It also said future gross margins can face volatility and downward pressure. In other words, Services still justifies the quality premium, but the filing does not say the margin story is risk-free.

That is the right way to read the stock. Apple is not losing its economic quality. It is defending a premium-quality profile while the external cost environment still matters.

Valuation leaves less room for a simple recap

This is where the market-context panel matters more than a simple recap implies.

Google Finance showed AAPL at $270.23 at the April 17, 2026 close, with a 34.19x trailing P/E and a $3.97 trillion market cap. That is not the setup of a hated stock waiting for basic reassurance. It is the setup of a stock already priced as a durable compounder.

That does not mean the shares cannot go higher. It means the burden of proof is different. The next updates no longer need Apple to prove it can still ship at scale. They need to show that China can keep improving, Services can keep protecting the mix, and costs such as tariffs do not eat enough of the benefit to flatten the valuation story.

This is why the current Apple debate is more interesting than a simple "great quarter" recap. Great quarters alone are not enough for megacaps at this size. The stock needs repeatability.

Risks to the Thesis

The repurchase argument is not a simple negative. The risk is that too much of the per-share story depends on a huge cash engine staying huge while the valuation already reflects premium execution.

Apple's financial statements showed $53.925 billion of quarterly operating cash flow, and the 10-Q said the company repurchased 93 million shares for $25.0 billion during the quarter while paying $3.9 billion of dividends and dividend equivalents. The diluted weighted-average share count fell to 14.810 billion from 15.151 billion a year earlier, a decline of about 2.2%.

That matters because Apple is not only compounding through products and Services. It is also compounding by shrinking the share base with exceptional consistency. When the business is this large, that per-share support can materially shape how quickly EPS compounds even if topline growth normalizes.

This is also why the current setup is more balanced than a one-sided bullish or bearish case. One side argues that a great quarter solves everything. The other argues that repurchases are masking a weaker core. The better reading is that the core is strong and repurchases are still a major reason the stock remains such a powerful per-share machine.

What Flips the Call

There are four things worth tracking next.

First, the framework needs the Greater China rebound to continue. One good quarter helps, but the valuation benefits much more if China stops looking like a chronic drag.

Second, Services needs to keep defending the mix. A 76.5% Services gross margin is powerful, but it matters most if that level continues to offset the lower economics of the product side.

Third, buybacks need to stay credible. Apple can support per-share growth aggressively because the cash engine is huge. If that cash engine weakens, the stock has to lean more heavily on pure operating growth.

Fourth, the framework needs tariff and cost pressure to stay visible. Apple explicitly said product gross-margin gains were only partially offsetting tariffs, and R&D expense rose 32% year over year to $10.887 billion. Those costs do not break the story, but they do explain why a premium multiple can still feel capped.

Current editorial read

Apple's business does not look fragile in 2026. The official numbers are too strong for that.

The harder question is whether a stock already trading around $270, 34x trailing earnings, and nearly $4 trillion of market value can still rerate easily from here. The answer is more conditional than a simple optimistic reading implies.

The FY26 Q1 print made the quality of the underlying business obvious. But the stock already prices a lot of that quality at 34x trailing earnings and nearly $4 trillion of market value, which means the next valuation step depends on three things holding together at once: the repurchase engine staying funded by the cash machine, the 38% Greater China rebound continuing rather than reverting, and tariff cost pressure not eroding the margin gains the company itself flagged. The setup is high-quality on the operating side, but the burden of proof on the multiple now sits with the next two prints, not with this one.