Market & Macro

Salesforce Stock in 2026: Agentforce ARR Versus Cash-Flow Discipline

A 2026 Salesforce stock review that weighs FY26 cash flow, Agentforce ARR, RPO depth, 10-K AI monetization risk, and the balance-sheet cost of a large ASR.

(Sources: Salesforce FY26 Q4 results release, Salesforce FY26 Form 10-K, Salesforce March 11, 2026 8-K, Public.com CRM stock page, BLS CPI release for March 2026, FOMC minutes, March 17-18, 2026, Salesforce Agentforce pricing page)

Thesis

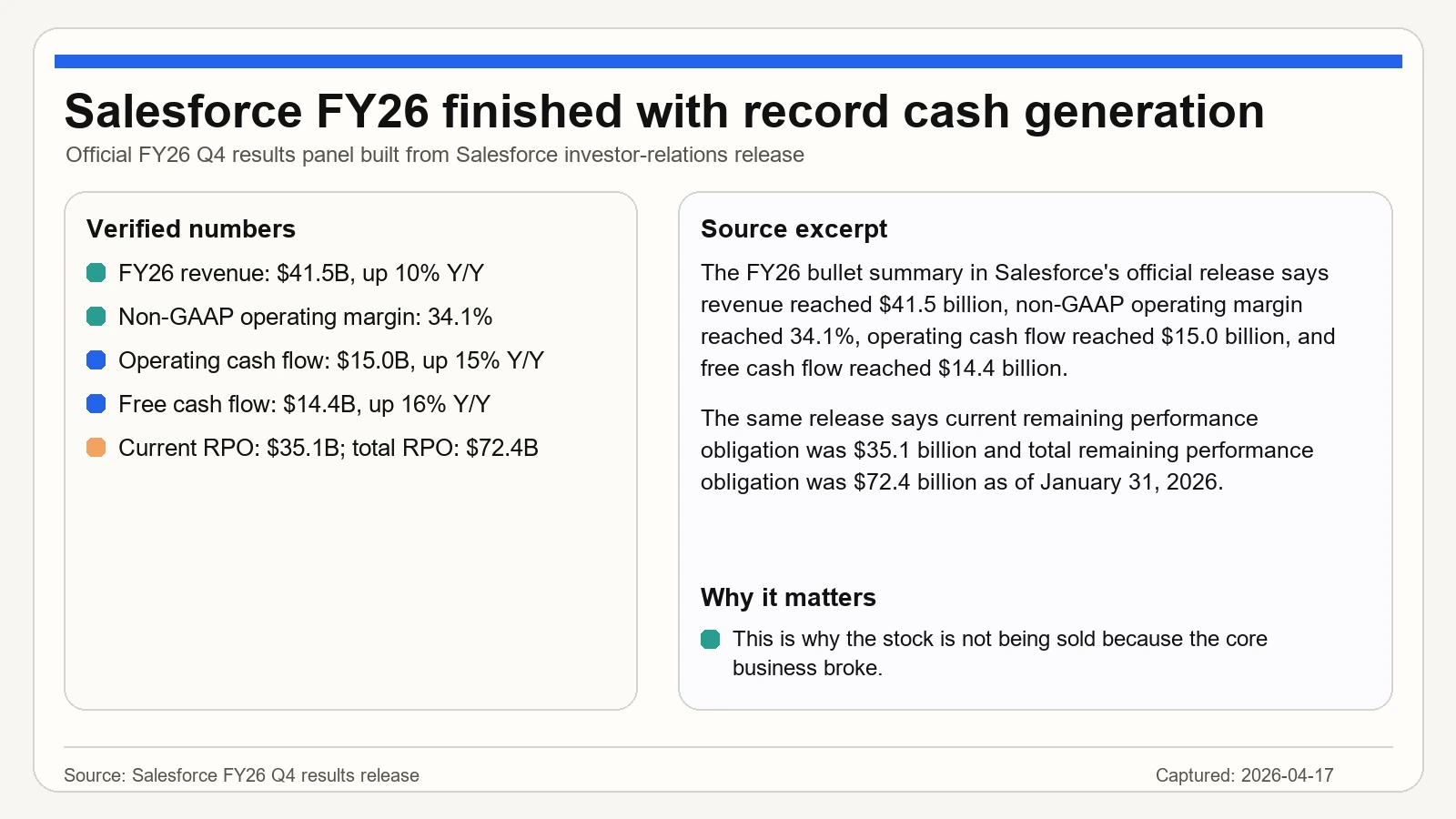

Salesforce is not a broken software company in 2026. Its official FY26 release showed $41.5 billion of revenue, $14.4 billion of free cash flow, $35.1 billion of current remaining performance obligation, and $72.4 billion of total remaining performance obligation.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

The harder question is whether the market should treat CRM as a mature SaaS cash-flow story or as a software platform with a credible second growth curve in Agentforce. That distinction matters because Salesforce can be financially strong and still fail to earn a higher multiple if AI usage does not become a durable revenue pool.

Using the Public.com market-cap snapshot of $163.93 billion and Salesforce's FY26 free cash flow of $14.4 billion, CRM traded at roughly an 8.8% free-cash-flow yield. That figure frames the setup: the cash engine is visible, but the valuation reset still depends on Agentforce becoming large enough to change the growth profile.

Source Evidence Snapshot

The hero image carries the official FY26 revenue, margin, free-cash-flow, and RPO proof. The body evidence keeps the two most decision-useful visuals: Agentforce monetization evidence and Salesforce's own 10-K risk language. The ASR and related debt are handled as a source note in the capital-structure discussion rather than as a third finance screenshot.

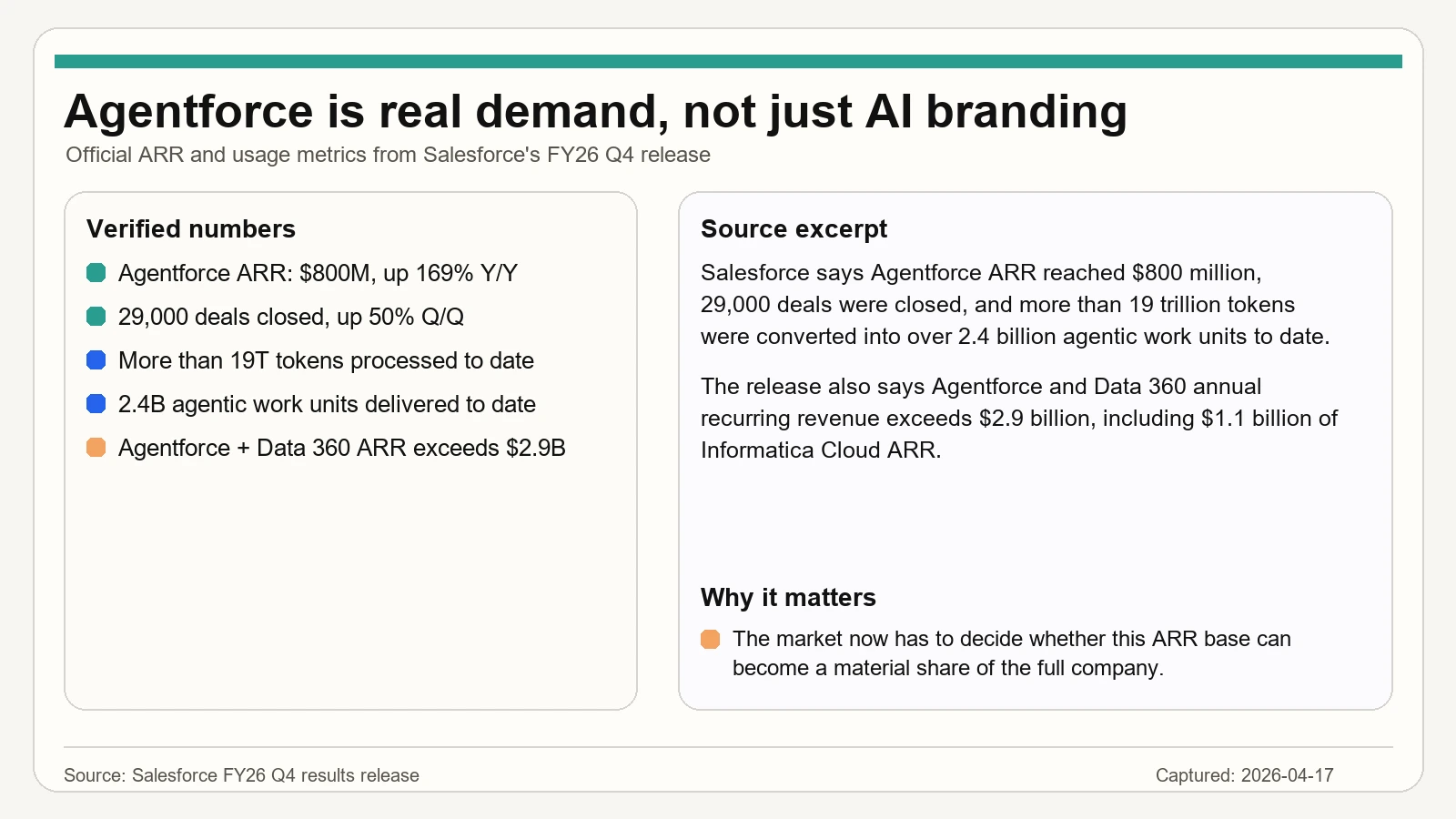

Source capture: Salesforce FY26 Q4 results release, captured 2026-04-17. The official AI highlights showed Agentforce ARR of $800 million, more than 29,000 deals closed, more than 19 trillion tokens processed to date, more than 2.4 billion agentic work units delivered, and combined Agentforce and Data 360 ARR above $2.9 billion.

Open source.

Source capture: Salesforce FY26 Q4 results release, captured 2026-04-17. The official AI highlights showed Agentforce ARR of $800 million, more than 29,000 deals closed, more than 19 trillion tokens processed to date, more than 2.4 billion agentic work units delivered, and combined Agentforce and Data 360 ARR above $2.9 billion.

Open source.

This panel is the clearest reason not to dismiss Agentforce as a branding exercise. It does not prove final margin durability, but it does show that Salesforce has moved the AI product cycle into measurable ARR and usage metrics.

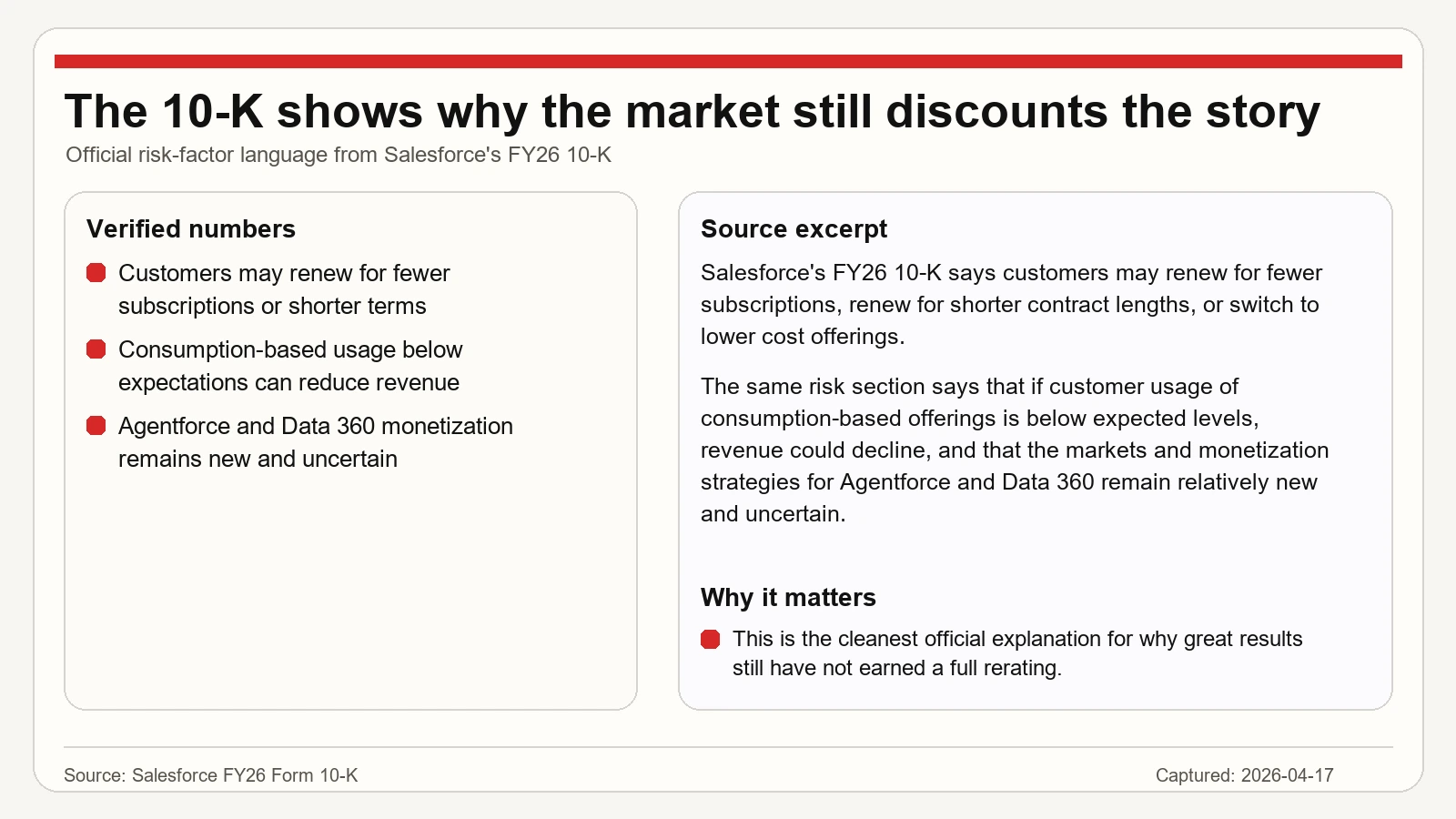

Source capture: Salesforce FY26 Form 10-K, captured 2026-04-17. The risk-factor section states that customers may renew for fewer subscriptions or lower-cost offerings, consumption-based usage may fall below expectations, and the markets and monetization strategies for Agentforce and Data 360 remain relatively new and uncertain.

Open source.

Source capture: Salesforce FY26 Form 10-K, captured 2026-04-17. The risk-factor section states that customers may renew for fewer subscriptions or lower-cost offerings, consumption-based usage may fall below expectations, and the markets and monetization strategies for Agentforce and Data 360 remain relatively new and uncertain.

Open source.

This is the counterweight to the Agentforce evidence. Salesforce's own filing says the transition to newer AI and data monetization models still carries execution risk.

Capital-return source note: Salesforce's March 11, 2026 8-K describes $25 billion of accelerated share repurchase agreements, expected net proceeds of about $24.885 billion from the related offering, and a $6 billion five-year senior unsecured term-loan agreement. The buyback improves the per-share argument only if the cash engine and AI transition remain strong enough to keep the balance sheet from becoming part of the downside case.

What the Street is Pricing

The market is not pricing Salesforce as distressed. It is also not pricing it as a clean AI compounder.

At the captured Public.com market cap of $163.93 billion, Salesforce traded at about 4.0x FY26 revenue and about an 8.8% FY26 free-cash-flow yield. That combination says the market gives credit to the current business, but still requires proof before attaching a higher AI software multiple.

The Street is effectively asking three questions at once: whether Agentforce ARR can move from $800 million to a more material share of total revenue, whether Data 360 can reinforce that adoption, and whether Salesforce can maintain operating discipline while integrating Informatica and funding a large ASR.

That is a more precise debate than "is Salesforce relevant?" Relevance is already supported by the FY26 numbers. The open issue is whether the new AI layer can change the company's medium-term growth algorithm.

Risks to the Thesis

The largest risk is that Agentforce stays real but not large enough. A product can produce impressive early ARR and still fail to move the consolidated growth rate if renewal pressure, seat rationalization, or lower-cost product substitution offsets the new revenue pool.

The second risk is margin dilution. Agentforce, Data 360, Informatica integration, and AI infrastructure can all require investment. If Salesforce protects growth by spending more than the market expects, the cash-flow yield may look less compelling.

The third risk is capital structure. The $25 billion ASR signals confidence, but the related debt funding means the framework has to keep leverage and interest expense in view rather than treating the repurchase as a purely mechanical upside lever.

The macro backdrop also matters. The March 2026 CPI release and March FOMC minutes point to energy-driven inflation pressure and equity-market concern around AI business-model disruption. Valuation resets are harder when software multiples face discount-rate pressure.

What Flips the Call

The Salesforce setup improves if Agentforce and Data 360 keep expanding from measurable adoption into a clearly material revenue layer while current RPO remains strong. The next proof point is not another AI announcement; it is ARR, usage, renewal, and margin evidence showing that the new layer is additive.

The setup weakens if Agentforce growth slows, consumption revenue disappoints, Informatica integration pressures margins, or the ASR starts to look more like leverage-supported financial engineering than confidence in durable cash generation.

For now, CRM is best framed as a strong cash-flow company with a real AI revenue option that still needs scale proof. The official numbers support the business quality. They do not yet settle the valuation question.