Market & Macro

How to Read Bank Earnings: Five Gates Beyond EPS

A five-gate method for comparing JPMorgan, Bank of America, and Citi earnings without mixing adjustments, revenue composition, cost conversion, credit denominators, or valuation expectations.

The direct answer: read every bank quarter through five gates—adjustments, revenue mix, cost conversion, credit denominators, and expectations. Q2 2026 shows why. JPMorgan produced the highest adjusted return of the three, while Citi produced the widest gap between revenue growth and expense growth. Neither fact alone identifies the cleaner or more durable earnings system.

Thesis: the best headline number may carry the hardest burden of proof

Bank earnings become comparable only after their definitions become visible. A reported return may contain a gain. Mid-teens revenue growth may come from spread income, recurring fees, trading, or investment banking. A low credit-loss percentage may describe the whole loan book while a higher one describes cards only.

The useful conclusion is therefore narrower than “which bank won the quarter.” First identify what must repeat. Then ask how much durability the market price already requires. The method is falsifiable at the Q3 filings: if adjustments, mix, cost, credit, and price/TBV do not explain the direction of returns and tangible book value per share, the framework needs revision.

Source Evidence Snapshot

| Bank | Q2 return used here | Revenue / expense signal | Market expectation snapshot | First boundary |

|---|---|---|---|---|

| JPMorgan | 23% ROTCE excluding significant items | Adjusted managed revenue +14.8%; expense +15% | ~3.01× price/TBV | Managed revenue and ROTCE are company non-GAAP |

| Bank of America | 17.03% ROTCE | GAAP revenue +15.0%; expense +8.4% | ~2.07× price/TBV | Segment mix is reported separately on an FTE basis |

| Citi | 13.0% RoTCE | GAAP revenue +14.3%; expense +4.7% | ~1.34× price/TBV | Quarterly return is not the target covering the 2029–2031 period |

These rows do not form a ranking. They expose the adjustment, denominator, and expectation attached to each headline.

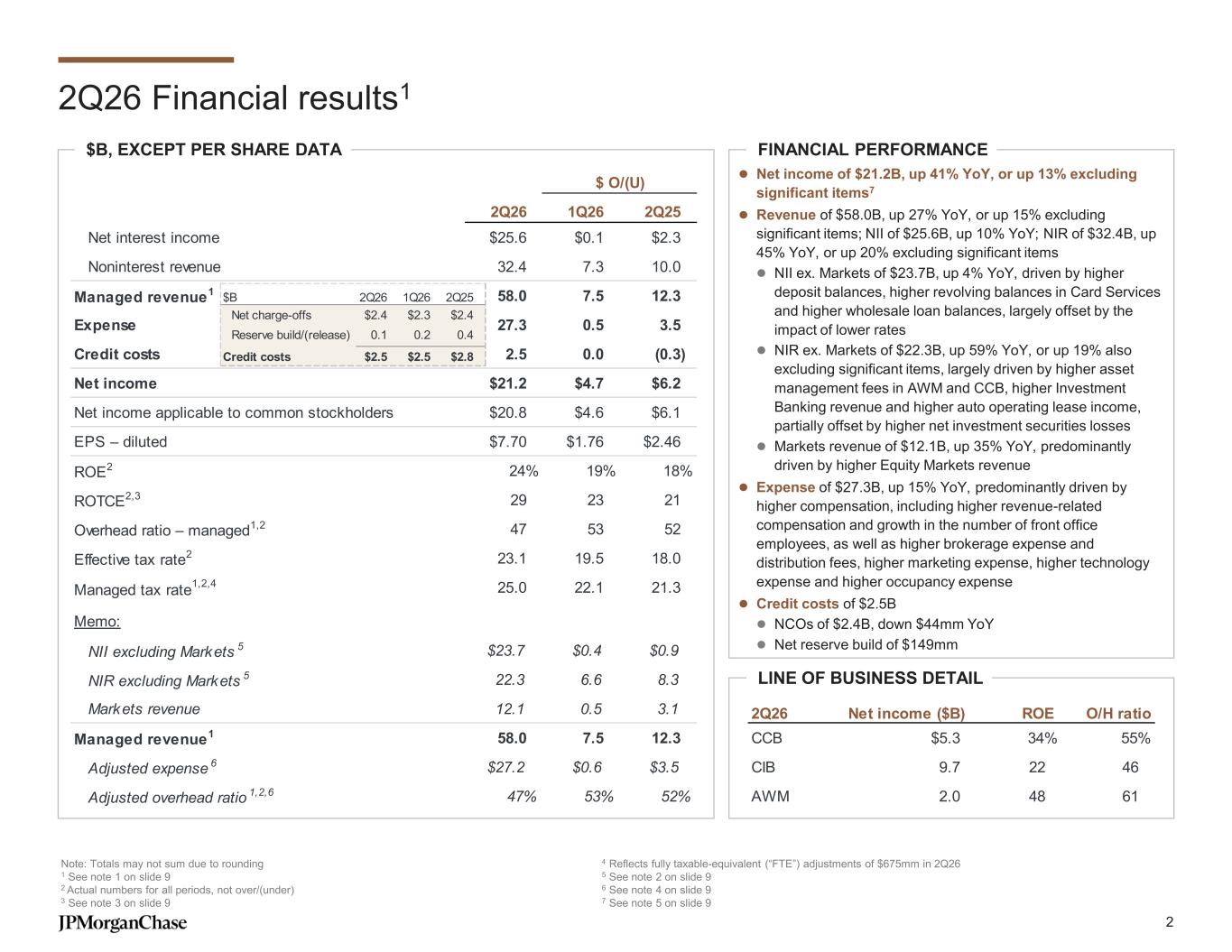

Proof one: JPMorgan's 29% headline falls to 23% after disclosed gains

JPMorgan's official presentation reports $21.155B of net income and 29% ROTCE, then identifies $4.219B of after-tax Visa and equity-investment gains. Excluding those significant items leaves $16.936B of net income and 23% ROTCE.

2026-07-14, captured 2026-07-15. Managed revenue and ROTCE are company non-GAAP measures; the related article shows the significant-item reconciliation.The adjustment changes the magnitude, not the fact that the quarter was strong. It also changes the comparison question. The right input is not 29% versus another bank's unadjusted return; it is 23% with the adjustment disclosed, followed by a test of revenue mix and costs.

Gate 1 — remove gains and preserve each definition

Start with the earnings release and presentation reconciliation. JPMorgan reported $58.022B of managed revenue. Subtracting $5.576B of pretax significant items gives $52.446B, an article calculation. Against $45.680B a year earlier, adjusted managed revenue increased $6.766B, or 14.8%.

Bank of America and Citi do not require that same significant-item removal for the comparison used here, but their labels still differ. Bank of America's consolidated bridge is GAAP while its business-segment revenue is fully taxable-equivalent, or FTE. Citi writes RoTCE; JPMorgan and Bank of America write ROTCE. All three returns and tangible book values are company non-GAAP measures.

The first gate cannot prove future durability. It prevents an avoidable category error before the deeper work begins.

Gate 2 — separate the durable engine from the cyclical accelerator

JPMorgan's Fixed Income and Equity Markets revenue increased $3.142B. That was 46.4% of the $6.766B adjusted managed-revenue increase. Bank of America's Global Markets generated $2.040B, or 49.4%, of the $4.133B increase on the separate FTE segment basis.

Those contributions are real earnings, not accounting noise. They are also influenced by client activity, volatility, issuance, market share, and compensation. The comparable question is not whether Markets is “good” or “bad.” It is whether non-Markets NII and recurring fees can carry more of the next increase if activity cools.

The company-specific JPMorgan mix test and Bank of America revenue bridge preserve the exact denominators. This hub keeps their conclusions separate and reuses only the common reading order.

Gate 3 — measure how much growth expense absorbed

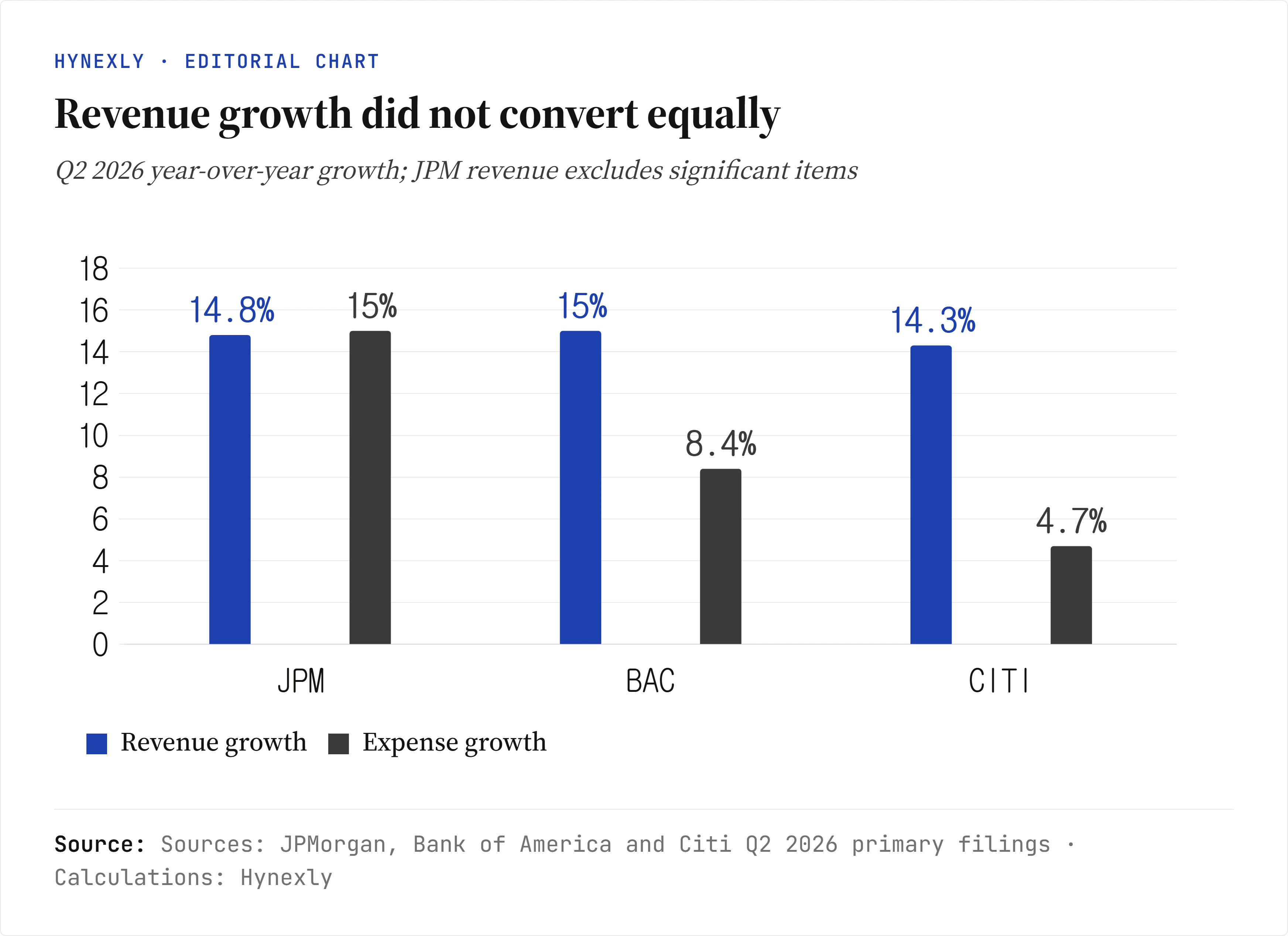

The three banks all produced roughly mid-teens revenue growth, but conversion differed.

(4.115 / 27.443) - (1.444 / 17.183) = 6.59%p. Citi uses exact GAAP changes: (3.098 / 21.668) - (0.638 / 13.577) = 9.60%p. Sources were filed or published 2026-07-14; units are year-over-year percentages.JPMorgan's rounded adjusted-revenue and expense growth were both about 15%, so its growth-cost gap was approximately 0%p. Bank of America's exact gap was 6.59%p. Citi's was 9.60%p. That does not make Citi the best franchise: restructuring, investment needs, provision, taxes, and capital intensity still matter. It does show that a high quarterly return and strong incremental conversion answer different questions.

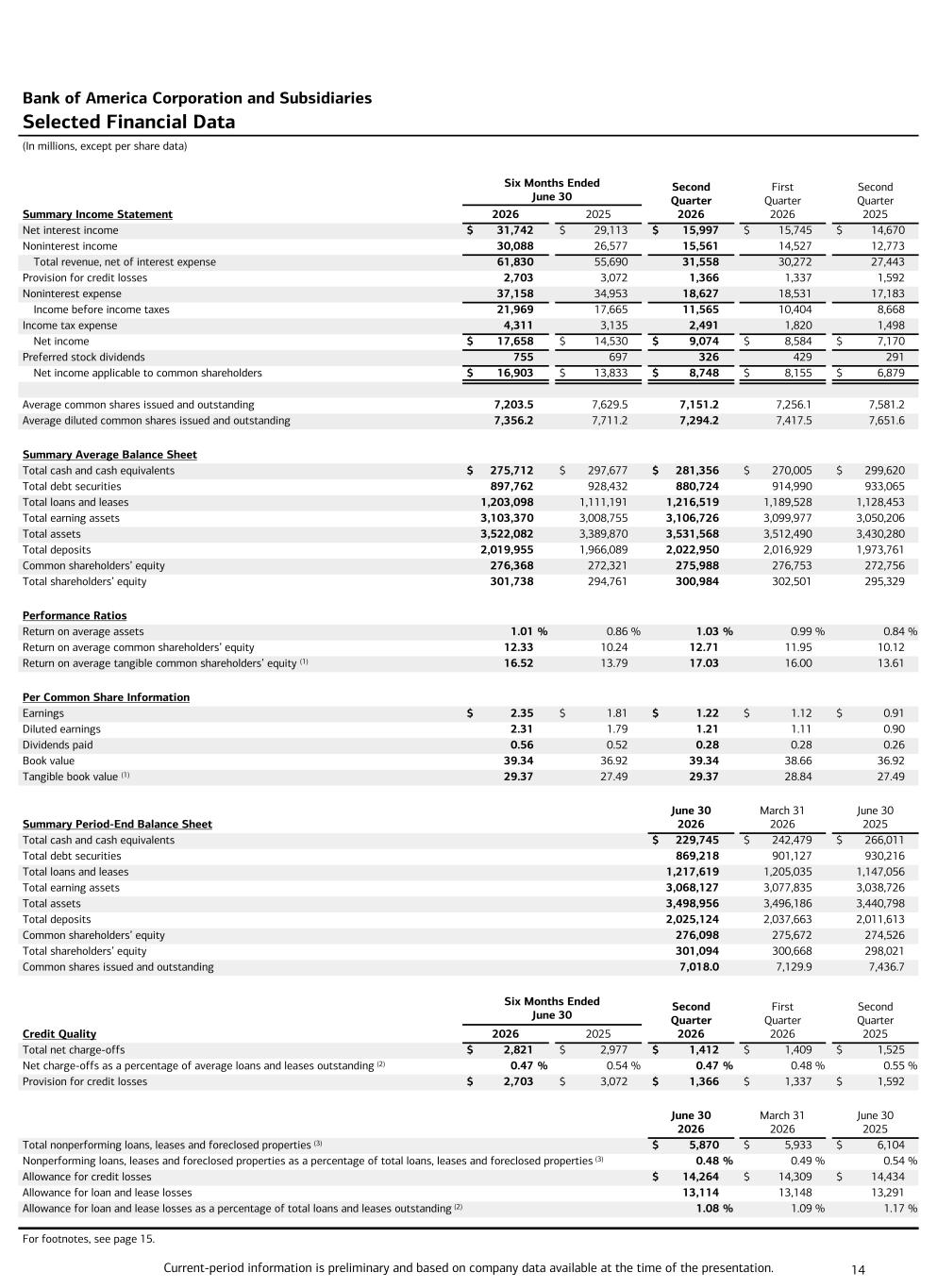

Proof two: Bank of America's GAAP bridge keeps cost and credit beside revenue

Bank of America reported revenue of $31.558B versus $27.443B, noninterest expense of $18.627B versus $17.183B, and provision for credit losses of $1.366B versus $1.592B.

2026-07-14, captured 2026-07-15. Values are USD millions except per-share data and ratios.The table makes the mechanism visible: revenue added $4.115B, expense absorbed $1.444B, and provision declined $226M. What it cannot prove is how those relationships behave when Markets slows, rates change, or borrower stress appears later.

Gate 4 — match every credit percentage to its portfolio

Three percentages that look ready for a leaderboard are not comparable. JPMorgan's 3.34% is a Card Services net charge-off rate. Bank of America's 0.47% is a consolidated net charge-off ratio. Citi's 4.1% is a card net credit loss rate.

The correct comparison is directional. JPMorgan's Q2 Card Services rate was above its roughly 3.2% full-year outlook, though a quarter and a full-year forecast are not interchangeable. Bank of America's consolidated ratio improved from 0.55% to 0.47%. Citi's card rate improved from 4.4% to 4.1%, while companywide net credit losses still increased 8%.

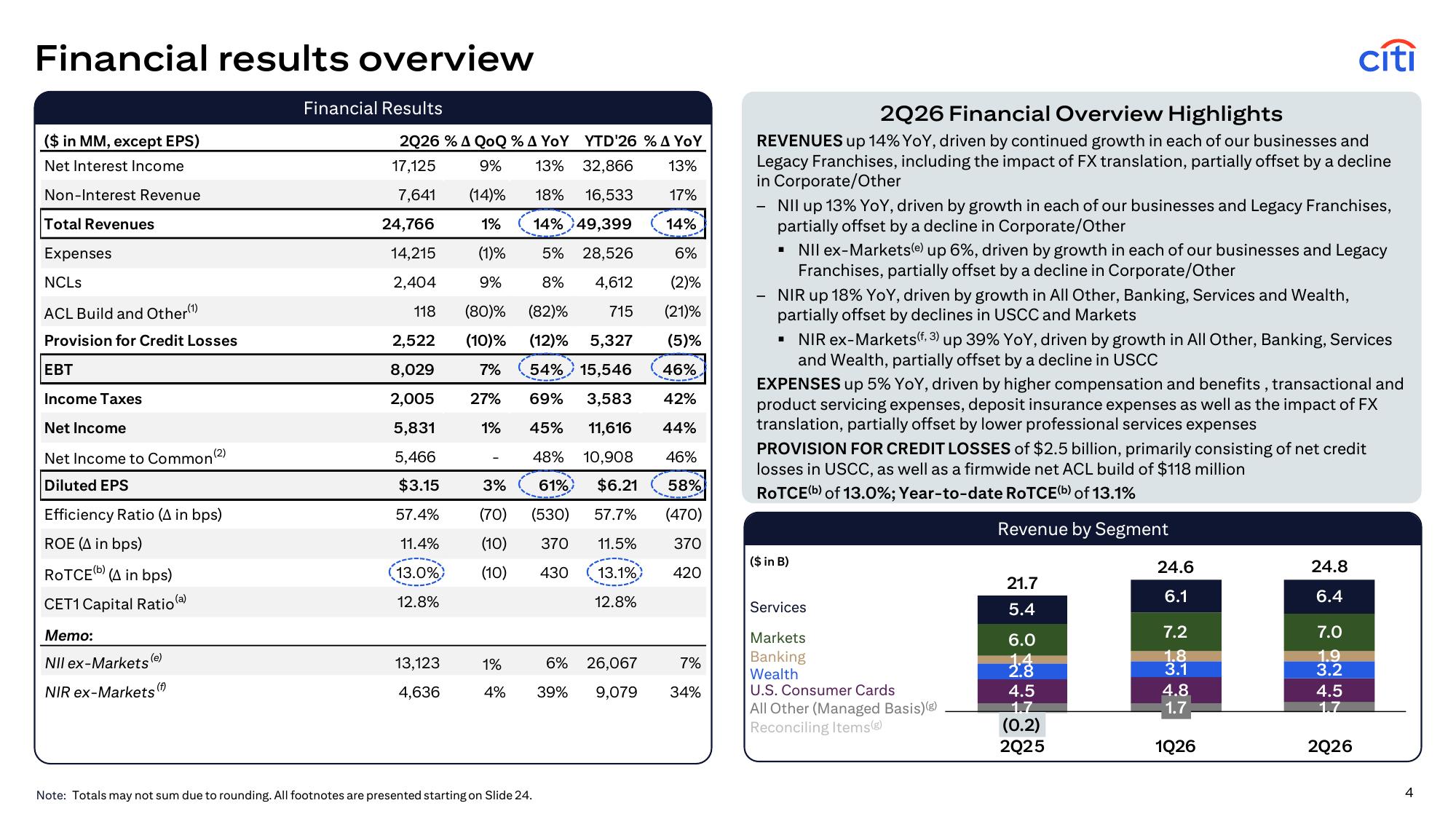

Proof three: Citi shows why conversion and credit must remain separate

Citi's official overview reports revenue of $24.766B, expense of $14.215B, provision of $2.522B, pretax income of $8.029B, and 13.0% RoTCE.

2026-07-14, captured 2026-07-15. RoTCE and the efficiency ratio are company non-GAAP measures; dollar values are USD billions unless noted.Citi's $3.098B revenue increase and $638M expense increase produced the strongest growth-cost gap in this comparison. Provision also declined $350M, helping pretax income rise $2.810B. The strongest counterevidence is duration: the 13.0% quarter is not proof of Citi's 14–15% medium-term target for the 2029–2031 period, and credit losses can lag revenue momentum.

What the Street is Pricing: price/TBV turns quality into a durability test

At the timestamped 2026-07-14 snapshots used in the underlying articles, JPMorgan traded near 3.01× quarter-end tangible book value per share, Bank of America near 2.07×, and Citi near 1.34×.

2026-07-14; TBV/share and returns are quarter-end company non-GAAP measures. The ratios are expectation gauges, not fair-value estimates or price targets.The map explains why the highest return does not settle the debate. JPMorgan's premium multiple requires premium returns and tangible capital compounding to persist. Citi's lower multiple requires less current return, but its move above tangible book shifts the case from discount closure toward sustained improvement. Bank of America sits between them and must show that core NII and fees can replace some of the Markets accelerator.

Risks to the Thesis

The strongest risk is false comparability. The framework uses a mix of managed revenue, GAAP revenue, FTE segments, differently named return measures, and different credit portfolios. Labels reduce that risk but do not erase it.

The second risk is over-rewarding short-term operating leverage. A bank can keep expense growth low by delaying technology, controls, talent, or customer acquisition. A wider one-quarter revenue-cost gap is evidence of conversion, not a full efficiency judgment.

The third risk is treating price/TBV as valuation truth. Tangible book excludes assets and franchise value that can matter, while a high-return bank may rationally trade at a premium. The ratio only identifies how much durable return the market appears to require.

The fourth risk is cycle timing. Credit losses often arrive after revenue slows, while Markets strength can disappear before annual guidance changes. One favorable quarter cannot prove a through-cycle earnings system.

What Flips the Call

| Gate | Current Q2 evidence | More constructive evidence | Framework warning |

|---|---|---|---|

| Adjustments | JPM 23% ROTCE excluding significant items | High returns persist without new gains | Reported and adjusted results diverge again |

| Revenue mix | Markets supplied ~46% JPM and ~49% BAC incremental growth on their stated bases | Non-Markets NII and fees carry more growth | Consolidated growth depends on another outsized Markets quarter |

| Cost conversion | Growth-cost gap ~0%p JPM, 6.59%p BAC, 9.60%p Citi | Revenue keeps outrunning necessary expense | Expense catches revenue as activity cools |

| Credit | Mixed card and consolidated ratios improved or stayed near outlook | Losses, delinquencies, and provision remain controlled | Loss ratios and provision rise together |

| Expectations | Price/TBV ~3.01× JPM, 2.07× BAC, 1.34× Citi | ROTCE and TBV/share compound together | Returns fade while premium multiples remain |

Source-derived decision visual: JPMorgan and Citi list Q3 results for 2026-10-13; Bank of America lists 2026-10-14. The watch items are editorial tests based on the Q2 filings, not company guidance or investment ratings.

The method becomes more useful if Q3 confirms the boundaries identified here: JPMorgan maintains adjusted return with less Markets help, Bank of America preserves core growth and conversion, and Citi sustains breadth without credit or capital deterioration. It weakens if those gates fail to explain the direction of returns and TBV/share better than the EPS headline.

Methodology, Sources & Disclosure

This article reconciles primary Q2 2026 releases reviewed on 2026-07-15. Revenue-growth minus expense-growth is an editorial calculation. JPMorgan's revenue input removes disclosed pretax significant items; Bank of America and Citi use exact GAAP year-over-year changes. Price/TBV uses one public price snapshot and quarter-end company TBV/share. No ratio is a fair-value estimate.

- JPMorgan: earnings release, presentation, and Q3 calendar

- Bank of America: earnings release, supplement, and 2026 reporting dates

- Citi: results, presentation, and investor calendar

AI assisted with source organization, deterministic chart production, bilingual consistency checks, and editorial compression. Every material number is tied to the primary-source ledger and requires human review before production deployment. The article provides no position-specific recommendation. This is general information, not individualized investment advice.