Market & Macro

Citigroup Q2 2026 Earnings: Has the Turnaround Earned a 1.34× TBV Multiple?

Citi reached 13.0% Q2 RoTCE and converted $3.098B of incremental revenue with 20.6% expense capture. The next test is sustaining returns above tangible book.

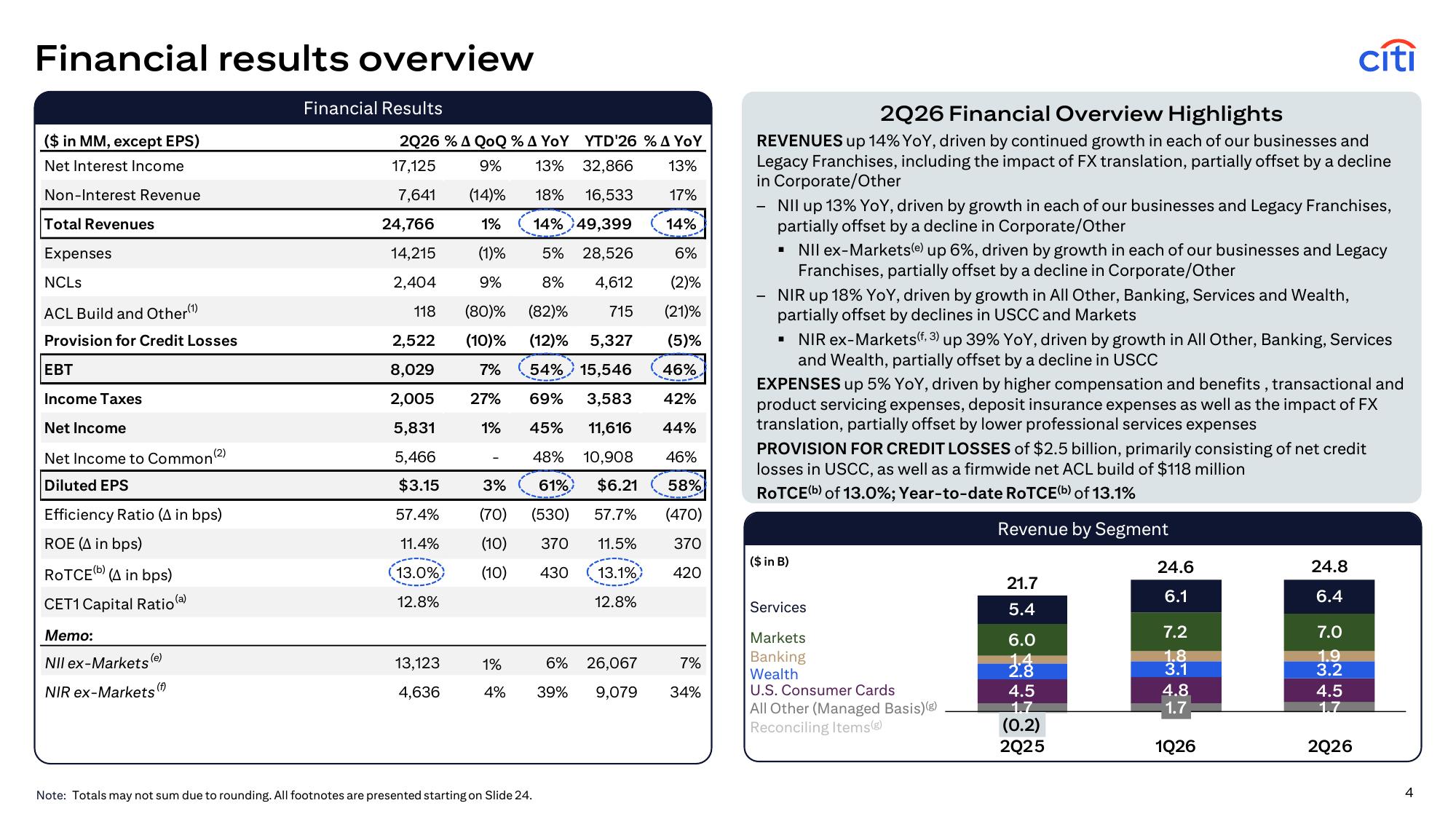

Citigroup's Q2 2026 result is no longer just a restructuring story. Revenue rose 14%, expense rose 5%, pretax income rose 54%, and return on average tangible common equity reached 13.0%. The harder question is whether those returns can persist now that the stock trades above tangible book value.

The cleanest evidence is the conversion bridge. Citi added $3.098B of revenue between Q2 2025 and Q2 2026 while adding $638M of expense. Expense therefore absorbed 20.6% of incremental revenue. A $350M decline in provision for credit losses then helped pretax income rise by $2.810B.

Source-derived answer map: Citi Q2 2026 results, earnings presentation, and Google Finance market snapshot. RoTCE and tangible book value are company non-GAAP measures.

| The 30-second answer | Verified evidence | What remains unproven |

|---|---|---|

| Returns improved | Q2 RoTCE 13.0%; YTD RoTCE 13.1% | Whether the result persists through a less favorable revenue mix |

| Conversion was strong | Expense captured 20.6% of incremental revenue | Whether the efficiency ratio can move below 55% over time |

| Growth was broad | All five businesses increased revenue | Whether U.S. Consumer Cards can grow faster than its cost base |

| Expectations rose | Price was about 1.34× quarter-end TBV | Whether capital returns still grow TBV per share above that valuation |

Thesis

Citi's Q2 evidence supports the turnaround thesis, but changes the burden of proof. The bank no longer needs only to show that simplification and expense control are working. It now needs to show that client-driven growth, operating efficiency and capital productivity can sustain a return profile worthy of a premium to tangible book value.

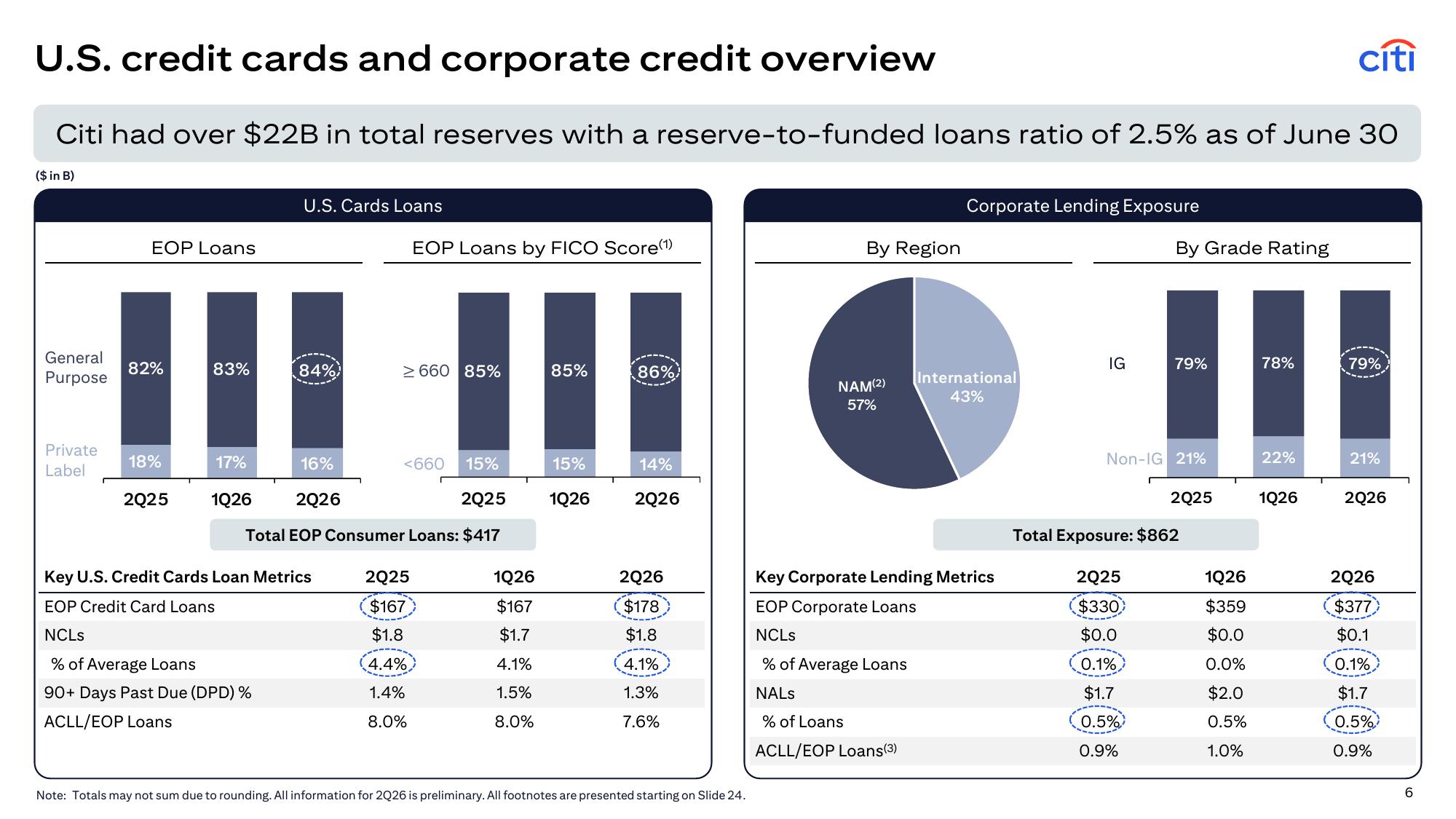

The constructive case has three parts. First, revenue growth was broad: Services rose 18%, Markets 17%, Banking 34%, Wealth 13% and U.S. Consumer Cards 1%. Second, revenue grew much faster than expense, lifting the efficiency ratio to 57.4% from 62.7%. Third, credit did not deteriorate enough to offset the operating improvement: provision declined 12%, the card net credit loss rate improved to 4.1% from 4.4%, and 90-day-plus card delinquencies declined to 1.3% from 1.4%.

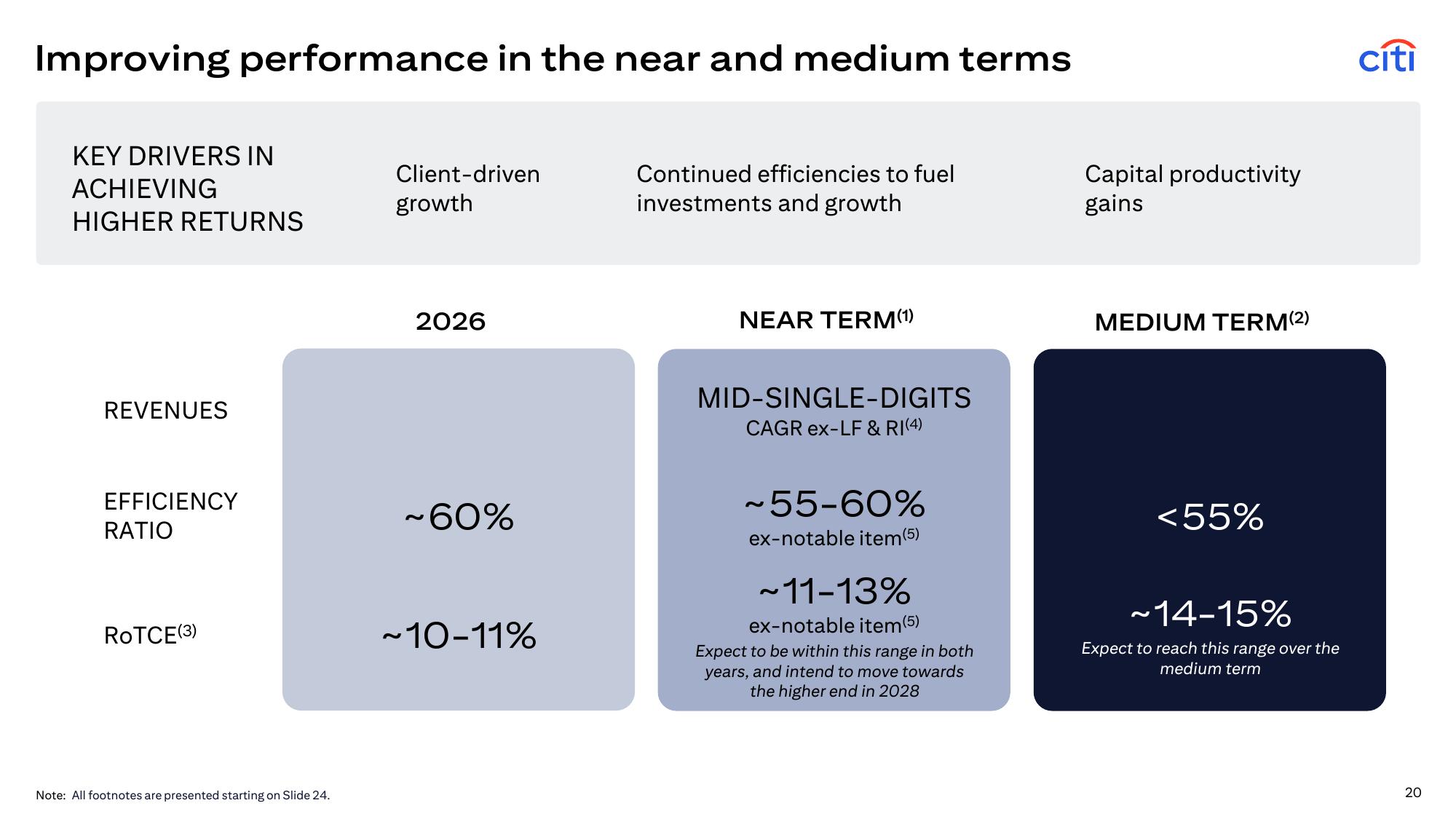

The boundary is valuation and duration. A single 13.0% RoTCE quarter is above Citi's 10–11% full-year RoTCE range for 2026; however, the company defines its 14–15% medium-term target as 2029–2031; the market snapshot near 1.34× tangible book therefore implies that investors are no longer paying only for a discount to close. They are paying for years of return improvement that still has to be delivered.

Source Evidence Snapshot

Citi's official overview puts the quarter's major lines on one page. Revenue was $24.766B, expense $14.215B, provision $2.522B, pretax income $8.029B, net income $5.831B and diluted EPS $3.15; the same page reports 13.0% RoTCE, a 57.4% efficiency ratio and 12.8% CET1.

2026-07-14, captured 2026-07-15. RoTCE is a company non-GAAP measure.The year-over-year bridge separates operating conversion from the credit benefit. Revenue rose from $21.668B to $24.766B. Expense rose from $13.577B to $14.215B. The $2.460B difference is a simple article calculation, not company-reported pre-provision net revenue. Provision then declined from $2.872B to $2.522B, reconciling exactly to the $2.810B increase in pretax income.

Source-derived visual: Citi Q2 2026 results and key metrics. Calculations: $24.766B - $21.668B = $3.098B; $14.215B - $13.577B = $0.638B; $2.872B - $2.522B = $0.350B.

The mix was broad enough to distinguish Citi from a one-desk trading result. Banking was the fastest-growing business at 34%, driven by investment banking. Services and Markets each added scale, while Wealth also grew double digits. U.S. Consumer Cards was the weak point: revenue rose only 1% while expense rose 10%.

Source-derived visual: Citi Q2 2026 results. Percentages are company-reported year-over-year revenue growth rates.

Credit provides both support and a warning. Citi reported more than $22B of total reserves and a 2.5% reserve-to-funded-loans ratio. U.S. card loans increased to $178B from $167B, the net credit loss rate improved to 4.1% from 4.4%, and 90-day-plus delinquencies improved to 1.3% from 1.4%. Corporate loans increased to $377B from $330B while non-accrual loans remained 0.5% of loans.

2026-07-14, captured 2026-07-15. Q2 information is preliminary as labeled by Citi.The countercase is that absolute net credit losses still rose 8% year over year to $2.404B as loan balances expanded. Better ratios do not eliminate the risk that losses rise later if borrower stress follows growth. That lag matters when the valuation already assumes improving returns.

Citi's own target slide is the clearest boundary. Management targets an efficiency ratio near 60% and RoTCE near 10–11% for 2026; 55–60% efficiency and 11–13% RoTCE during 2027–2028 and below 55% efficiency with 14–15% RoTCE for the 2029–2031 period.

2026-07-14, captured 2026-07-15. These targets are forward-looking non-GAAP measures subject to macro and market conditions.

Source-derived visual: Citi Q2 2026 earnings presentation, slides 4 and 20. Citi defines 2027–2028 as near term and 2029–2031 as medium term.

What the Street Is Pricing

This section uses a timestamped public market snapshot rather than private research, named analyst opinions or a share-price objective. The Qualcomm expectations analysis applies the same boundary to a different business model.

At 2026-07-14 16:08:50 UTC, Google Finance displayed Citi at $135.01, with a market capitalization near $239.83B and a trailing price-to-earnings ratio near 16.69; Citi reported Q2 tangible book value of $100.89 per share and book value of $114.74 per share.

| Expectation bridge | Value | Boundary |

|---|---|---|

| Price / tangible book value | ~1.34× | $135.01 / $100.89; TBV is non-GAAP |

| Price / book value | ~1.18× | $135.01 / $114.74 |

| Q2 RoTCE | 13.0% | One quarter; company non-GAAP measure |

| 2026 RoTCE target | 10–11% | Forward-looking company target |

| Medium-term RoTCE target | 14–15% | Applies to 2029–2031; not the next quarter |

The 1.34× price-to-TBV ratio changes the debate. When a bank trades below tangible book, a credible repair can create value by closing a discount. Above tangible book, the market increasingly requires returns that exceed the cost of equity and remain durable through credit and market cycles. Q2 moved Citi closer to that proof, but did not complete it.

Capital return adds a second expectation. Citi repurchased $4.0B of common shares in Q2 and returned about $5.0B including dividends, a 92% payout ratio. Common shares outstanding declined 8.9% year over year to 1.677B, yet Citi explicitly said repurchases were dilutive to tangible book and book value per share. Buying above per-share book values can still reduce share count and support per-share earnings, but it raises the hurdle for organic capital generation to keep TBV per share rising.

This is the same evidence discipline used in the Bank of America Q2 revenue bridge: reported figures, management targets, public market data and article calculations remain visibly separate.

The JPMorgan Q2 adjusted-return test shows the other end of the bank-return spectrum: a 23% adjusted ROTCE quarter paired with a price near 3.01× tangible book still requires a revenue-mix test.

Risks to the Thesis

The first risk is that revenue breadth narrows. Markets revenue rose 17% and equities revenue rose 45%. A quieter trading or underwriting environment could remove part of the quarter's operating leverage before slower-moving efficiency gains replace it.

The second risk is U.S. Consumer Cards. Revenue rose 1%, expense rose 10%, and card loans increased 7%. The net credit loss rate improved, but the business needs revenue growth and credit performance to absorb acquisition and engagement costs.

The third risk is credit lag. Net credit losses rose 8% even as ratios improved. If loan growth slows and losses rise together, provision could reverse from a $350M year-over-year benefit into a drag.

The fourth risk is the capital-return trade-off. Citi's $30B repurchase authorization can reduce share count, but repurchases above tangible book make per-share book accretion harder. Earnings generation must offset that arithmetic.

The fifth risk is time. The 14–15% RoTCE target applies during 2029–2031 and a 1.34× TBV snapshot discounts some progress years before the endpoint, leaving less room for simultaneous misses in efficiency, credit and business growth.

| Risk path | Q2 evidence | What would weaken the thesis |

|---|---|---|

| Revenue mix | Five businesses grew; Markets +17% | Services, Banking and Wealth slow together as Markets normalizes |

| U.S. Cards | Revenue +1%; expense +10% | Loss rates rise before revenue catches cost growth |

| Credit | NCLs +8%; provision −12% | Provision and NCL ratios rise together |

| Capital | $4B repurchased; TBV/share +7% YoY | TBV/share stalls while buybacks remain above TBV |

| Return duration | Q2 RoTCE 13.0% | YTD returns fall below the RoTCE range for 2026 |

What Flips the Call

Citi lists its Q3 2026 earnings call for 2026-10-13. The next filing should be tested against returns, efficiency, breadth and per-share capital—not one earnings-per-share headline.

Editorial decision visual based on Citi Q2 2026 results, the earnings presentation, and the official investor calendar. These are editorial monitoring tests, not Citi guidance.

The conclusion becomes more constructive if year-to-date RoTCE remains inside or above the 10–11% full-year target, the efficiency ratio stays near or below the roughly 60% guide, Services, Banking and Wealth grow without an outsized Markets quarter, card loss indicators remain controlled, and TBV per share keeps rising after repurchases.

The conclusion weakens if core business growth slows, expense growth catches revenue, provision and loss ratios rise together, and TBV per share stalls while the stock remains above tangible book. One weaker Markets quarter would not invalidate the thesis. A simultaneous failure of breadth, efficiency, credit and capital accretion would.

The decision boundary is simple: Q2 proved that Citi can produce a 13% quarter with strong conversion. Q3 must show that the result belongs to a repeatable earnings system rather than a favorable quarter inside a long target horizon.

Methodology, Sources & Disclosure

The operating bridge uses Citi's reported GAAP revenue, expense, provision and pretax income. Expense capture divides the year-over-year expense increase by the revenue increase. Price-to-book ratios use one public share-price snapshot and quarter-end company values; they are not fair-value estimates. RoTCE, tangible book value and management return targets are company non-GAAP measures. The article does not treat a quarterly actual as proof that a multi-year target has been achieved.

- Citi Q2 2026 results and key metrics, published

2026-07-14 - Citi Q2 2026 earnings presentation, published

2026-07-14 - Citi Q2 2026 financial supplement, published

2026-07-14 - Citi Investor Relations, checked

2026-07-15 - Google Finance Citigroup market snapshot, observed

2026-07-14 16:08:50 UTC

Facts, calculations and links were rechecked as of 2026-07-15. AI assisted with structure and consistency checks; the official sources, calculations, captures, EN/KO parity and final wording require human review before production deployment. No sponsorship or affiliate relationship with Citigroup is disclosed. This is general information, not individualized investment advice; it does not issue an investment rating or share-price objective.