Market & Macro

Bank of America Q2 2026 Earnings: The $4.1B Revenue Bridge

Bank of America added $4.115B of Q2 revenue. This source-based analysis separates durable NII and fee growth from the Global Markets accelerator.

Bank of America reported a strong Q2 2026; the useful question is not whether the headline was good. It is where the acceleration came from and how much of it can repeat.

GAAP revenue increased $4.115B year over year to $31.558B. Net interest income supplied $1.327B of that increase. Noninterest income supplied $2.788B. On the company's separate fully taxable-equivalent, or FTE, segment basis, Global Markets generated $2.040B—about 49.4%—of the $4.133B incremental revenue.

Source-derived answer map: Bank of America Q2 2026 earnings release, presentation, and supplement. FTE segment data are non-GAAP and are not interchangeable with the GAAP revenue bridge.

| The 30-second answer | Verified evidence | What remains unproven |

|---|---|---|

| Growth was broad | NII +9%; every operating segment grew revenue | Whether breadth survives weaker trading activity |

| Markets was the accelerator | Global Markets supplied 49.4% of incremental FTE segment revenue | Whether the next revenue increase relies less on Markets |

| Conversion was strong | Expense absorbed 35.1% of incremental GAAP revenue | Whether investment and compensation costs stay controlled |

| Credit held | NCO ratio 0.47% versus 0.55% a year earlier | Whether consumer and commercial credit stay inside the recent range |

Thesis

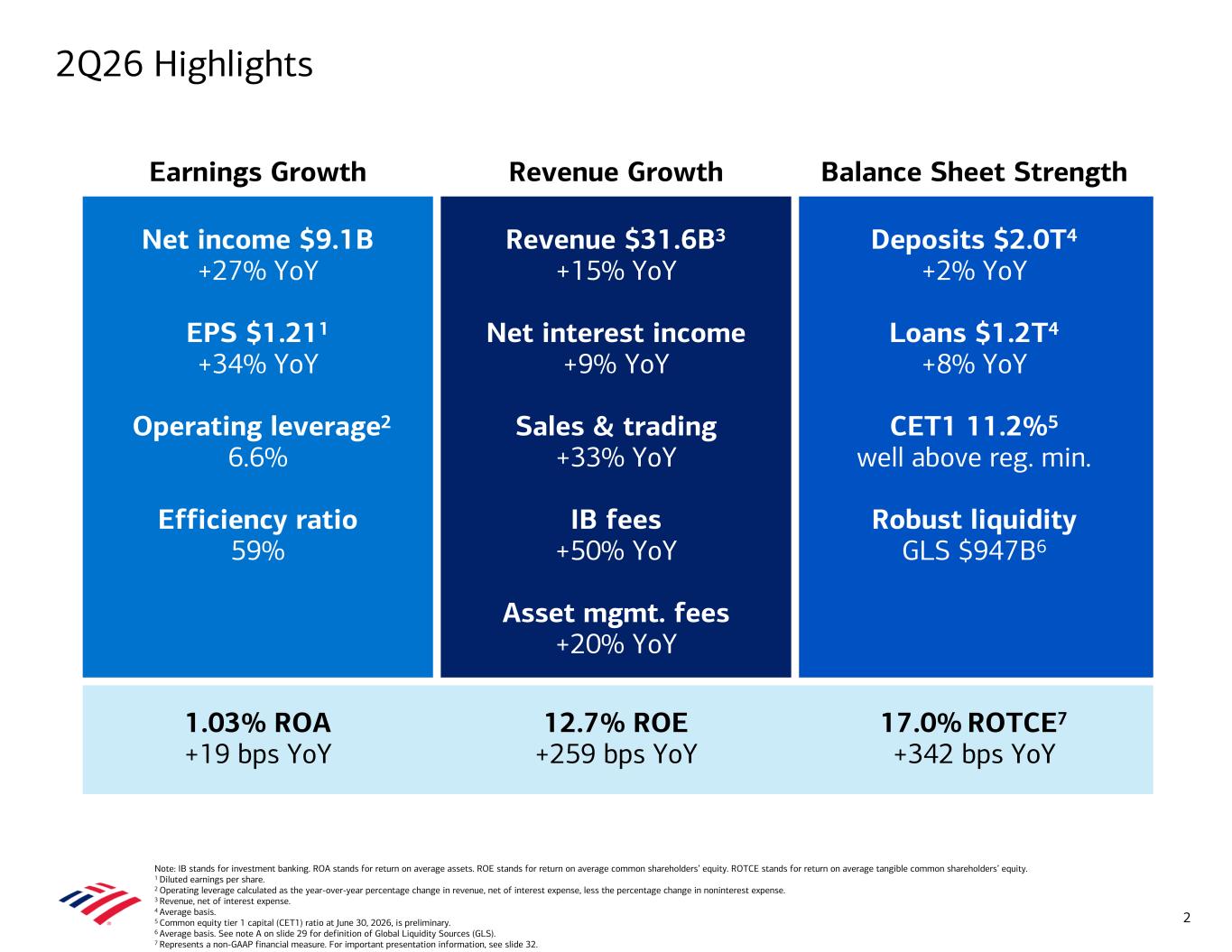

Bank of America's Q2 evidence supports a constructive earnings-quality thesis with a clear mix boundary. The durable engine improved: average loans rose 8%, average deposits rose 2%, NII rose 9%, asset-management fees rose 20%, and all four operating segments increased net income by double digits. Revenue grew faster than expense, producing 6.6% operating leverage and an efficiency ratio near 59%.

The boundary is the source of the acceleration. Global Markets generated nearly half of incremental FTE segment revenue and 57.6% of the increase in consolidated net income. Equities revenue rose 70% to $3.622B, and total sales and trading revenue rose 33% to $7.098B. Those results are economically real, but transaction volume, volatility, client positioning, and market share can make them less mechanically repeatable than spread income or recurring asset-management fees.

The right conclusion is therefore two-part. Q2 was not only a trading spike: core banking, wealth, expense conversion, and credit all improved. It was also not a clean run-rate template. The next filing must show that NII and recurring fees can carry more of the growth if Markets normalizes.

Source Evidence Snapshot

Bank of America's official presentation puts the breadth in one place: net income $9.1B, revenue $31.6B, NII growth of 9%, sales and trading growth of 33%, ROTCE of 17.0%, and an 11.2% CET1 ratio.

Primary-source capture: Bank of America Q2 2026 earnings presentation, slide 2, filed 2026-07-14, captured 2026-07-15. ROTCE and operating leverage are company non-GAAP measures.

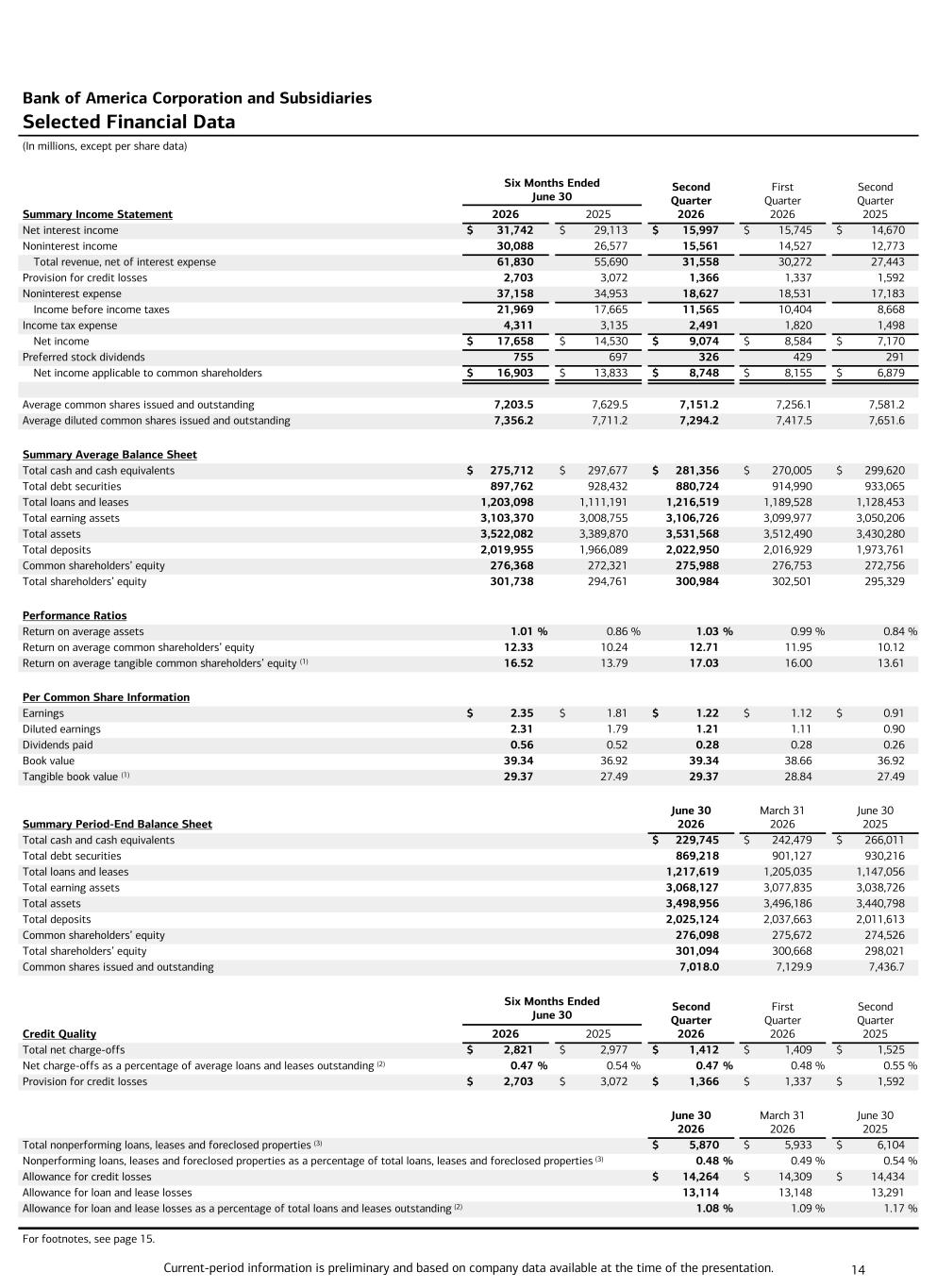

The GAAP bridge is more informative than the percentage headline. Revenue rose from $27.443B to $31.558B. NII rose from $14.670B to $15.997B, contributing 32.2% of the increase. Noninterest income rose from $12.773B to $15.561B, contributing 67.8%.

Source-derived visual: Bank of America Q2 2026 earnings release. Calculations: $15.997B - $14.670B = $1.327B; $15.561B - $12.773B = $2.788B.

The selected-financial-data table confirms the same bridge and adds the cost and credit lines. Noninterest expense rose to $18.627B from $17.183B, while provision for credit losses declined to $1.366B from $1.592B.

Primary-source capture: Bank of America Q2 2026 earnings release, page 14, filed 2026-07-14, captured 2026-07-15. Values are USD millions except per-share data and ratios.

The FTE segment table answers the mix question. Global Markets revenue rose from $5.982B to $8.022B, a $2.040B increase. GWIM added $934M, Global Banking $547M, Consumer Banking $523M, and All Other improved by $89M. These values sum to the $4.133B FTE revenue increase; they should not be mixed with the $4.115B GAAP bridge.

Source-derived visual: Bank of America Q2 2026 supplemental information, quarterly results by business segment. Segment revenue is reported on an FTE basis, a company non-GAAP measure.

This is the same category discipline used in the guide to reading AI revenue claims: a reported consolidated figure, a management presentation basis, and an article calculation can all be useful, but they must remain visibly separate.

Expense conversion was also material. The $1.444B increase in expense absorbed 35.1% of the $4.115B GAAP revenue increase, leaving a $2.671B incremental spread before the change in provision and tax. Provision declined by $226M. Reported pretax income rose $2.897B.

Article calculation from the Q2 2026 earnings release. The $2.671B spread is not company-reported pre-provision net revenue; it is simply incremental revenue minus incremental noninterest expense.

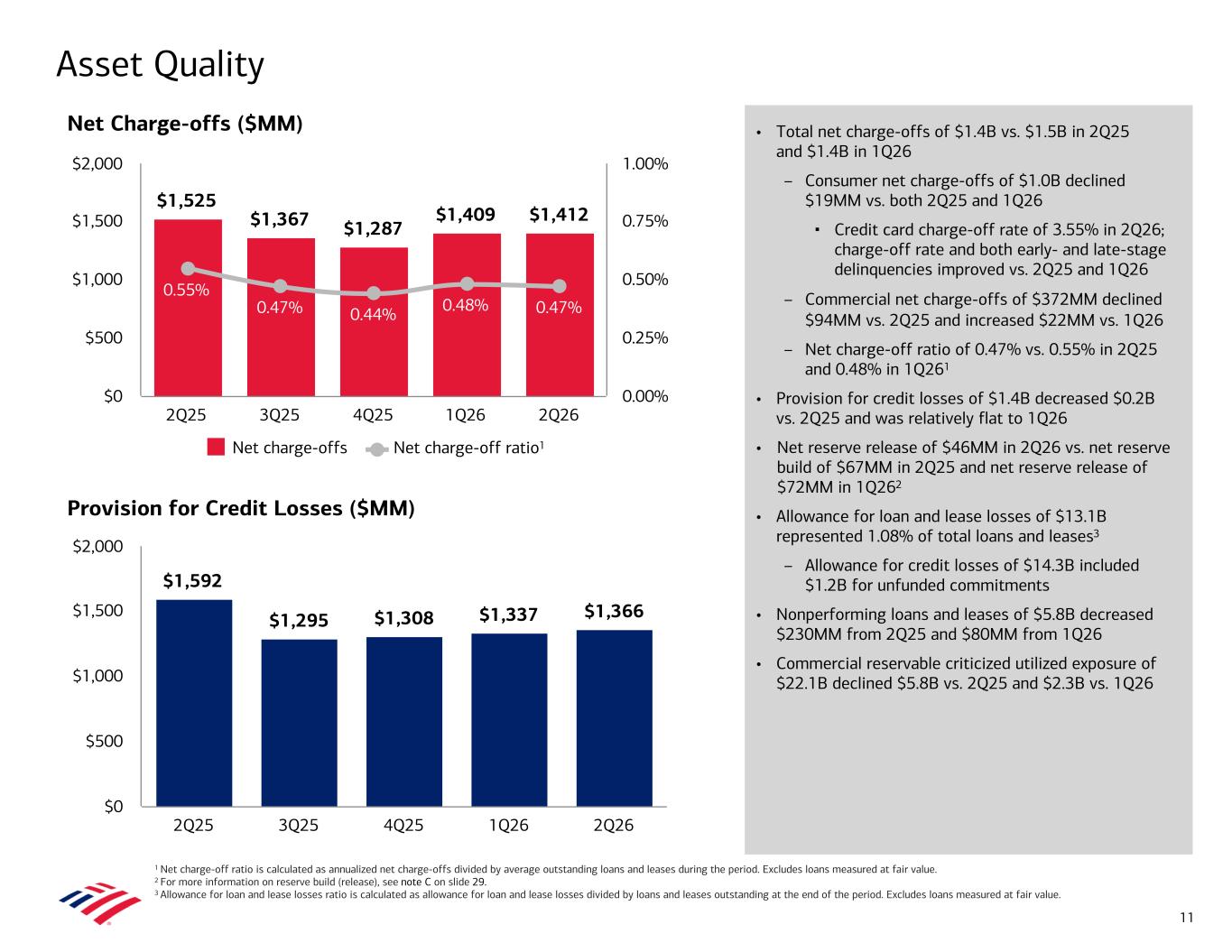

Credit did not provide a hidden warning. Net charge-offs were $1.412B, almost flat sequentially and down from $1.525B a year earlier. The annualized NCO ratio improved to 0.47% from 0.55%. Provision was close to charge-offs, and the company recorded a $46M net reserve release.

Primary-source capture: Bank of America Q2 2026 earnings presentation, slide 11, filed 2026-07-14, captured 2026-07-15. The NCO ratio is annualized and excludes loans measured at fair value.

The strongest countercase to the mix concern is visible here. The bank did not fund a Markets surge by accepting obviously worse credit or letting costs match revenue. Credit-card charge-offs and both early- and late-stage delinquencies improved year over year and sequentially. The question is durability, not whether Q2 quality was fictional.

What the Street Is Pricing

This section uses a timestamped public market snapshot rather than private consensus, analyst commentary, or a share-price objective.

At 2026-07-14 11:00:59 EDT, Google Finance displayed BAC at $60.92 and a market capitalization near $432.11B. Bank of America reported tangible book value of $29.37 per common share at quarter-end and Q2 net income of $9.074B. The Qualcomm expectations analysis uses the same public-snapshot boundary without turning market data into a rating.

| Expectation bridge | Value | Boundary |

|---|---|---|

| Price / tangible book value | ~2.07× | $60.92 / $29.37; TBV is non-GAAP |

| Price / book value | ~1.55× | $60.92 / $39.34 |

| Market cap / annualized Q2 net income | ~11.9× | $432.11B / ($9.074B × 4) |

| Annualized Q2 net income / market cap | ~8.4% | Single-quarter annualization, not a forecast yield |

| Q2 ROTCE | 17.03% | Company non-GAAP return measure |

The price-to-TBV ratio says that the market is assigning substantial value above current tangible common equity. That can be rational if a 17% class ROTCE, positive operating leverage, and controlled credit persist. The ratio becomes less forgiving if returns fall because Markets normalizes before core revenue and expense efficiency compensate.

The annualized-quarter multiple is deliberately crude. A bank's earnings vary with rates, credit, markets activity, taxes, and capital actions. It is useful only as an expectation gauge: the snapshot does not require Q2 trading revenue to repeat forever, but it does require the franchise to replace cyclical strength with other earnings if it fades.

For a second large-bank comparison, the Citigroup Q2 turnaround test asks a different valuation question: what must a bank prove after the stock has moved above tangible book value?

Risks to the Thesis

The first risk is Markets normalization. Global Markets supplied 49.4% of incremental FTE segment revenue, and equities revenue rose 70%. A lower-volatility or lower-activity quarter could reduce that contribution quickly.

The second risk is rate and deposit repricing. NII improved because of Markets activity, higher loan and deposit balances, and fixed-rate asset repricing, partly offset by lower interest rates. Deposit competition or a different yield-curve path can change that balance.

The third risk is expense catch-up. Q2 expense growth of 8% stayed below revenue growth of 15%, but compensation, technology, brand, and growth investments continue. Operating leverage narrows if revenue normalizes while those costs remain.

The fourth risk is credit lag. The 0.47% NCO ratio and improving card delinquencies are constructive, but charge-offs typically respond after borrower stress appears. Commercial criticized exposure improved, yet credit can turn after revenue momentum slows.

The fifth risk is expectation. A price near 2.07× tangible book value leaves less room for simultaneous deterioration in ROTCE, operating leverage, and credit than a lower multiple would.

| Risk path | Q2 evidence | What would weaken the thesis |

|---|---|---|

| Markets mix | 49.4% of incremental FTE revenue | Markets falls and other segments do not replace it |

| Core NII | +9% YoY | NII stalls despite loan and deposit growth |

| Expense | +8% versus revenue +15% | Expense growth catches or exceeds revenue growth |

| Credit | NCO ratio 0.47% | NCOs and delinquencies move above the recent range together |

| Return expectation | ROTCE 17.03%; price/TBV ~2.07× | ROTCE compresses without a lower expectation multiple |

What Flips the Call

Bank of America has scheduled its Q3 2026 results for 2026-10-14. The next test should separate core revenue, business mix, expense conversion, and credit rather than focus on one earnings-per-share number.

Editorial decision visual based on Bank of America Q2 2026 results and the official 2026 reporting calendar. These are editorial monitoring tests, not company guidance.

The conclusion becomes more constructive if NII and recurring wealth or service fees remain positive, non-Markets segments carry a larger share of incremental revenue, revenue continues to outgrow expense, and the NCO ratio stays near or below the recent 0.44%–0.55% band.

The conclusion weakens if another outsized Markets quarter is necessary to keep consolidated revenue growing, expense growth catches revenue, and charge-offs or delinquencies rise together. One mix shift alone does not invalidate the thesis. A simultaneous failure of core growth, operating leverage, and credit would.

The decision boundary is simple: Q2 proved that Bank of America can combine a durable banking engine with a powerful Markets accelerator. Q3 must show that the engine can keep moving when the accelerator is used less aggressively.

Methodology, Sources & Disclosure

This article separates GAAP consolidated data, FTE segment data, company non-GAAP measures, public market data, and article calculations. The GAAP revenue bridge uses reported net interest income and noninterest income. The segment bridge uses the company's FTE basis and is never added to or substituted for GAAP revenue. Expense capture divides the year-over-year increase in noninterest expense by the increase in GAAP revenue. The annualized-quarter market ratio multiplies one quarter of net income by 4 and is not a forecast.

- Bank of America Q2 2026 earnings release, filed

2026-07-14 - Bank of America Q2 2026 earnings presentation, filed

2026-07-14 - Bank of America Q2 2026 supplemental information, filed

2026-07-14 - Bank of America 2026 financial reporting dates, published

2025-05-07 - Google Finance BAC market snapshot, observed

2026-07-14 11:00:59 EDT

Facts and links were rechecked as of 2026-07-15. AI assisted with structure and consistency checks; the official sources, calculations, captures, EN/KO parity, and final wording require human review before production deployment. No sponsorship or affiliate relationship with Bank of America is disclosed. This is general information, not individualized investment advice; it does not issue an investment rating or share-price objective.