Market & Macro

JPMorgan Q2 2026 Earnings: Is 23% Adjusted ROTCE Repeatable?

JPMorgan's Q2 ROTCE falls from 29% to 23% after significant items. A source-derived bridge tests how much of the adjusted growth came from Markets.

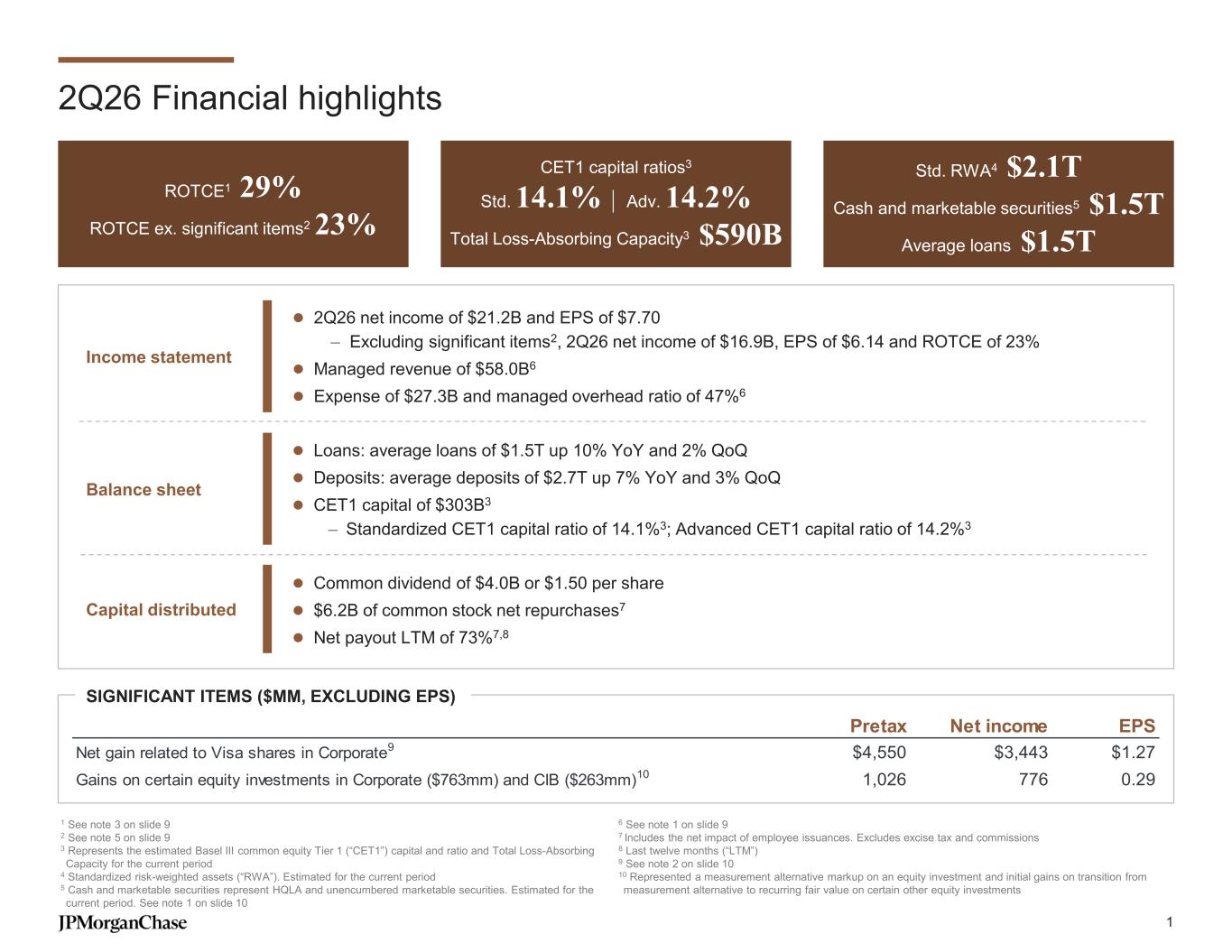

JPMorgan's reported Q2 2026 result is not the number investors should carry forward. The bank earned $21.155B and reported 29% return on tangible common equity, but $4.219B of after-tax Visa and equity-investment gains lifted that result. Removing those items leaves $16.936B of net income, $6.14 of diluted EPS and 23% ROTCE.

That adjusted quarter was still exceptional. The harder test is its composition. Markets supplied about 46% of the adjusted year-over-year increase in managed revenue, while a $341.025 share-price snapshot equaled roughly 3.01× quarter-end tangible book value. At that multiple, a favorable trading quarter is not enough; premium returns must repeat through a less favorable mix.

Source-derived answer map: JPMorgan Q2 earnings release, earnings presentation, and article calculations. ROTCE and managed revenue are company non-GAAP measures.

| The 30-second answer | Verified evidence | What remains unproven |

|---|---|---|

| Reported return was gain-assisted | 29% reported ROTCE; $21.155B net income | Whether one-time investment gains recur |

| Adjusted return remained strong | 23% ROTCE; $16.936B net income | Whether 20%+ persists in a quieter Markets quarter |

| Growth leaned on Markets | 46% of adjusted managed-revenue growth | Whether non-Markets growth can carry the next quarter |

| Expectations are demanding | ~3.01× price/TBV | Whether TBV and premium returns compound together |

Thesis

JPMorgan's Q2 supports a constructive but narrower conclusion: 23% ROTCE excluding significant items is strong evidence of franchise quality, not proof of a steady-state return. The result deserves more weight than the 29% headline because it removes the Visa and equity-investment gains. It still deserves a mix discount because Equity Markets revenue rose 86% and management described the environment as particularly favorable.

The countercase is substantial. Net interest income excluding Markets rose 4%. Noninterest revenue excluding Markets rose 19% after significant items. Consumer & Community Banking revenue rose 8%, Commercial & Investment Bank revenue rose 27%, and Asset & Wealth Management revenue rose 19%. Every major business produced record revenue, so the quarter was not only a trading event.

The thesis weakens if Markets normalizes while adjusted revenue grows more slowly than expense, Card Services losses move materially above the roughly 3.2% full-year outlook, adjusted ROTCE falls below the editorial 20% monitoring test and tangible book value per share stalls. That 20% line is not JPMorgan guidance or an investment rating.

Source Evidence Snapshot

JPMorgan's official highlights separate the headline from the decision number. The slide reports 29% ROTCE and 23% ROTCE excluding significant items, then identifies a $4.550B pretax Visa gain and $1.026B of pretax gains on certain equity investments. Their after-tax contributions were $3.443B and $776M.

2026-07-14, captured 2026-07-15. ROTCE, managed revenue and the results excluding significant items are company non-GAAP measures.The after-tax reconciliation is exact: $21.155B - $3.443B - $0.776B = $16.936B. The company rounds that result to $16.9B. Diluted EPS is $7.70; it falls to $6.14 after the adjustment, while ROTCE falls 6 percentage points from 29% to 23%. Removing the gains changes the magnitude, but not the conclusion that the underlying quarter was strong.

Source-derived explanation: JPMorgan Q2 2026 earnings presentation, slides 1 and 9. Nex is an explainer only; the SEC-filed slide above is the proof.

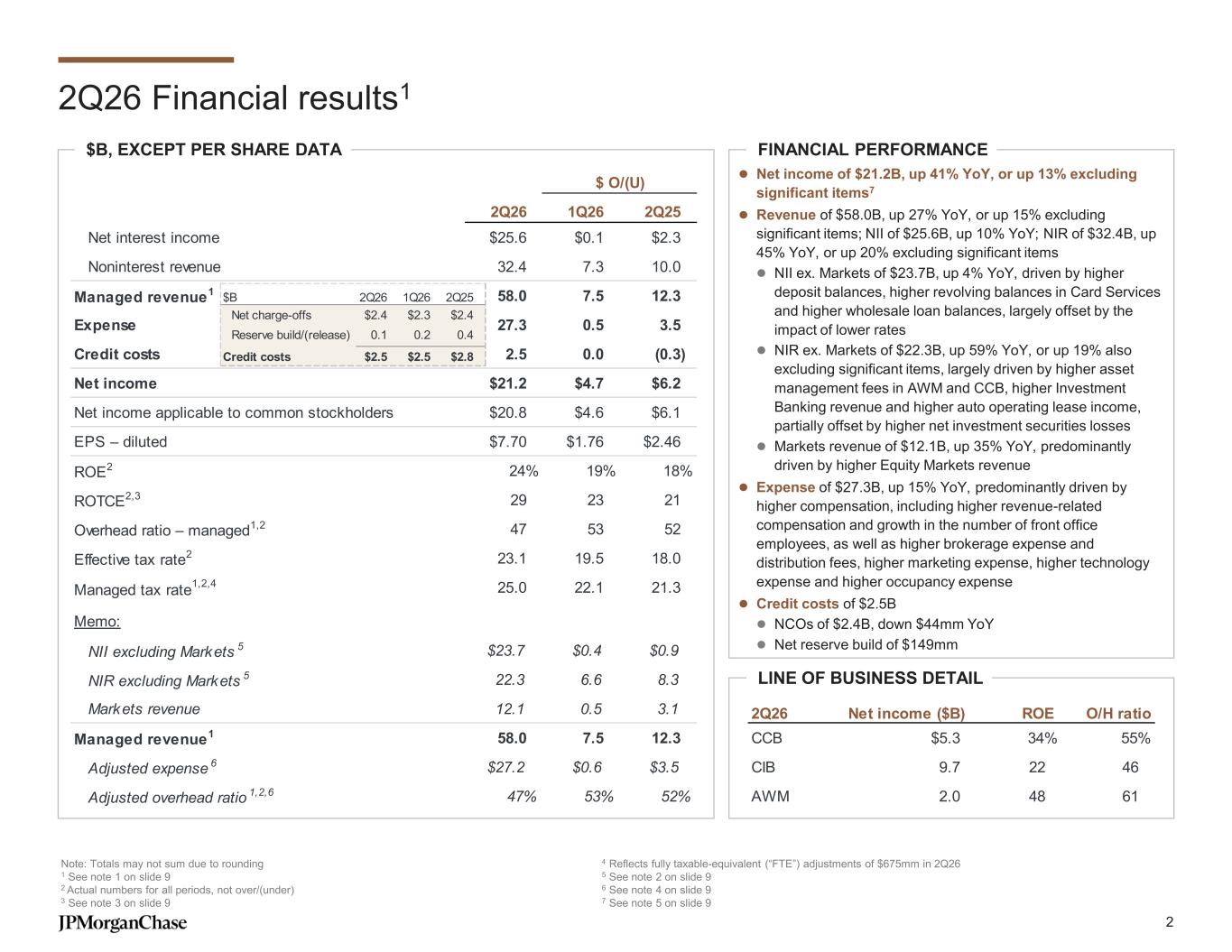

The second official slide shows where the underlying strength came from. Managed revenue was $58.0B, up 27%, or up 15% excluding significant items. NII excluding Markets was $23.7B, up 4%. Noninterest revenue excluding Markets was $22.3B, up 59%, or up 19% after removing significant items. Markets revenue was $12.1B, up 35%, while expense rose 15% and credit costs declined 12%.

2026-07-14, captured 2026-07-15. Values are in USD billions unless shown otherwise; the slide labels company non-GAAP measures.The growth mix can be reproduced from the filing. Managed revenue was $58.022B. Subtracting $5.576B of pretax significant items gives $52.446B of adjusted managed revenue, an article calculation rather than a company-reported subtotal. Against $45.680B in Q2 2025; the adjusted increase was $6.766B.

Fixed Income Markets revenue was $6.053B, up $363M, and Equity Markets revenue was $6.025B, up $2.779B. Markets therefore added $3.142B. Dividing that by the $6.766B adjusted increase gives 46.4%; all non-Markets sources supplied the remaining $3.624B, or 53.6%.

Source-derived visual: JPMorgan Q2 earnings release and earnings presentation, slides 2 and 5. Calculation: $3.142B / $6.766B = 46.4%. This attributes revenue growth; it does not estimate segment profit or forecast the next quarter.

That split is the central tension. Non-Markets sources contributed a majority, which supports durability. Markets still supplied almost half, and Equity Markets provided most of that increase. A quieter client-activity environment can reduce revenue quickly while compensation, technology and occupancy costs adjust more slowly.

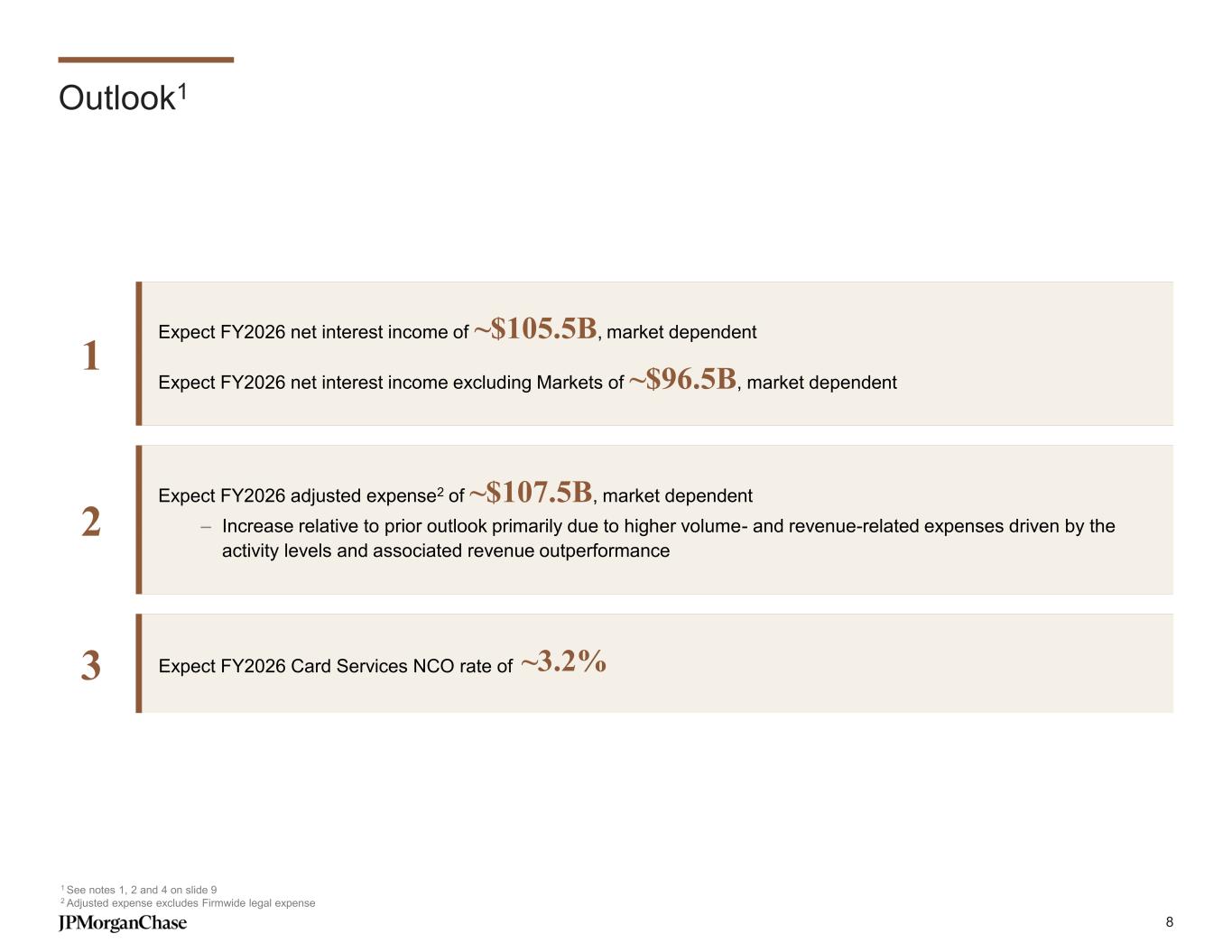

Management's outlook makes that cost boundary visible. JPMorgan expects about $105.5B of 2026 NII, about $96.5B of NII excluding Markets, about $107.5B of adjusted expense and a roughly 3.2% Card Services net charge-off rate. The adjusted-expense outlook increased because activity and revenue outperformed; it is market dependent rather than a fixed budget.

2026-07-14, captured 2026-07-15. All outlook figures are forward-looking, market dependent and use company definitions.What the Street Is Pricing

At 2026-07-14 16:36:37 UTC, Google Finance displayed JPMorgan at $341.025; JPMorgan reported Q2 tangible book value of $113.35 per share and book value of $133.01 per share. The resulting ratios are about 3.01× tangible book and 2.56× book value.

Source-derived market snapshot: Google Finance and JPMorgan Q2 2026 earnings presentation, slides 3 and 9. Calculation: $341.025 / $113.35 = 3.01×. This is expectation context, not a fair-value estimate.

| Expectation bridge | Value | Boundary |

|---|---|---|

| Price / tangible book value | ~3.01× | Timestamped price divided by quarter-end company TBV |

| Price / book value | ~2.56× | $341.025 / $133.01 |

| Reported Q2 ROTCE | 29% | Includes significant gains; company non-GAAP |

| Q2 ROTCE excluding significant items | 23% | One favorable quarter; company non-GAAP |

| TBV per share growth | 10% YoY | Historical growth, not a forward return promise |

The multiple does not prove overvaluation. It shows the expectation hurdle. A bank near 3× tangible book has less room to rely on discount closure than the Citi Q2 turnaround case. It needs high returns, capital growth and resilience to work together.

Capital remains strong but not static. Standardized CET1 was 14.1%, down from 14.3% in Q1 as higher risk-weighted assets absorbed 71bp of the ratio bridge. Net income added 102bp and capital distributions used 50bp. JPMorgan also returned $10.2B through dividends and net repurchases. Those distributions are sustainable only if earnings and TBV continue to replenish the base.

This mix-and-cost test complements the Bank of America Q2 revenue bridge. BAC's question was whether broad revenue converted after expense and provision. JPMorgan's question is whether a much higher adjusted return persists when the most favorable revenue engine cools.

Risks to the Thesis

The first risk is Markets normalization. Markets revenue rose 35%; Equity Markets rose 86% while Fixed Income Markets rose 6%. If equity financing and client activity normalize, the largest adjusted growth contributor can fade quickly.

The second risk is operating leverage after a strong quarter. Expense rose 15%, largely because of compensation, front-office growth, brokerage, distribution, marketing, technology and occupancy. Management raised the adjusted-expense outlook because activity was high. Revenue-linked cost is rational during strength, but becomes a risk if revenue falls first.

The third risk is consumer credit. Card Services' Q2 net charge-off rate was 3.34%, while the full-year outlook is about 3.2%. A quarterly rate and a full-year outlook are not directly interchangeable, but a sustained move higher would challenge the credit assumption behind premium returns.

The fourth risk is the valuation-capital interaction. TBV per share rose 10% year over year, but the stock snapshot was near 3.01× TBV. If risk-weighted assets keep expanding, distributions remain high and TBV growth slows, the valuation can lose support even without an earnings collapse.

| Risk path | Q2 evidence | What would weaken the thesis |

|---|---|---|

| Markets mix | 46% of adjusted revenue growth; Equities +86% | Adjusted growth becomes Markets-dependent as non-Markets fees and NII slow |

| Expense | Adjusted expense $27.2B; FY outlook ~$107.5B | Expense grows faster than adjusted revenue after activity cools |

| Card credit | Q2 NCO rate 3.34%; FY outlook ~3.2% | Loss performance moves materially above the outlook |

| Capital | CET1 14.1%; TBV/share +10% YoY | RWA and distributions outpace retained earnings and TBV growth |

| Return duration | Adjusted ROTCE 23% | Adjusted ROTCE falls below 20% with weaker mix and conversion |

What Flips the Call

JPMorgan schedules its Q3 2026 earnings call for 2026-10-13. The next report should be tested against five linked variables rather than diluted EPS alone.

Editorial decision visual based on the Q2 earnings release, earnings presentation, and official earnings calendar. The 20% ROTCE line is an editorial monitoring test, not company guidance.

| Watch item | Current evidence | Constructive condition | Weakening condition |

|---|---|---|---|

| Adjusted ROTCE | 23% in Q2 | Near or above 20% with less help from Markets | Below 20% alongside weaker conversion |

| Revenue mix | Non-Markets supplied 54% of adjusted growth | Non-Markets remains the majority | Markets exceeds half as other growth slows |

| Adjusted expense | $27.2B Q2; ~$107.5B FY outlook | Tracks near outlook and grows slower than revenue | Outruns adjusted revenue after activity cools |

| Card Services credit | 3.34% Q2 NCO; ~3.2% FY outlook | Full-year path remains consistent with outlook | Loss rate and provision rise together |

| Tangible book value | $113.35, up 10% YoY | Continues growing after distributions | Stalls while RWA and payouts rise |

The conclusion becomes more constructive if JPMorgan holds adjusted ROTCE near or above 20% while non-Markets sources remain the majority of growth, expense tracks near the outlook, card losses remain consistent with the full-year path and TBV per share continues to compound.

It weakens if Markets normalizes and all four supports fail together: adjusted revenue no longer outruns expense, consumer credit moves above the planned path, adjusted ROTCE drops below the editorial test and TBV stalls. One quieter trading quarter would not flip the thesis. A weaker earnings system would.

Methodology, Sources & Disclosure

The significant-item bridge subtracts JPMorgan's disclosed after-tax Visa and equity-investment gains from reported net income. The adjusted managed-revenue calculation subtracts the disclosed $5.576B pretax gains from managed revenue, then compares the result with Q2 2025; the Markets contribution uses the exact Fixed Income and Equity Markets changes in the presentation. Price-to-book ratios use one timestamped public price and quarter-end company values; they are not fair-value estimates.

- JPMorgan Q2 2026 earnings release, filed

2026-07-14 - JPMorgan Q2 2026 earnings presentation, filed

2026-07-14 - JPMorgan Q2 2026 financial supplement, filed

2026-07-14 - JPMorganChase 2026 earnings calendar, checked

2026-07-15 - Google Finance JPMorgan market snapshot, observed

2026-07-14 16:36:37 UTC

Facts, calculations, image captures and links were rechecked as of 2026-07-15. AI assisted with structure, chart production and EN/KO consistency checks; the official sources, calculations and final wording require human review before production deployment. No sponsorship or affiliate relationship with JPMorgan Chase is disclosed. This is general information, not individualized investment advice; it does not issue an investment rating or share-price objective.