Market & Macro

Amazon Stock in 2026: AWS Momentum Versus the Capex Bar

Amazon's 2025 Form 10-K and Q4 release show AWS reaccelerating, AWS operating income of $45.6 billion, operating cash flow of $139.5 billion, and a 2026 capex plan near $200 billion. The AMZN debate is whether the AI infrastructure bill earns visible returns.

(Sources: Amazon 2025 Form 10-K PDF, Amazon Q4 2025 results release, Yahoo Finance AMZN quote page)

Amazon's 2026 equity setup is not simply "AWS is accelerating again." The stronger reading is more conditional: AWS momentum is real, but the capex bar is now high enough that Amazon has to keep proving the infrastructure spend converts into durable returns.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

On February 5, 2026, Amazon said Q4 AWS sales rose 24% year over year to $35.6 billion, the fastest AWS growth in 13 quarters. The 2025 Form 10-K also showed full-year AWS net sales of $128.7 billion, up 20% from 2024, and AWS operating income of $45.6 billion.

Those are strong numbers. The tension is that Amazon also said it expects about $200 billion of capex in 2026. In the 10-K, operating cash flow rose to $139.5 billion, but free cash flow fell to $11.2 billion as net property-and-equipment purchases reached $128.3 billion.

Thesis

Amazon remains a high-quality operating business, but AMZN's 2026 debate has moved from cloud growth to cloud returns. AWS is growing faster and still produces a large profit pool. The question is whether the AI and infrastructure buildout can turn that profit pool into attractive returns on a much larger capital base.

That distinction matters because the useful question is free-cash-flow conversion, AWS operating leverage, and whether the market should treat capex as productive reinvestment or as a rising hurdle.

Source Evidence Snapshot

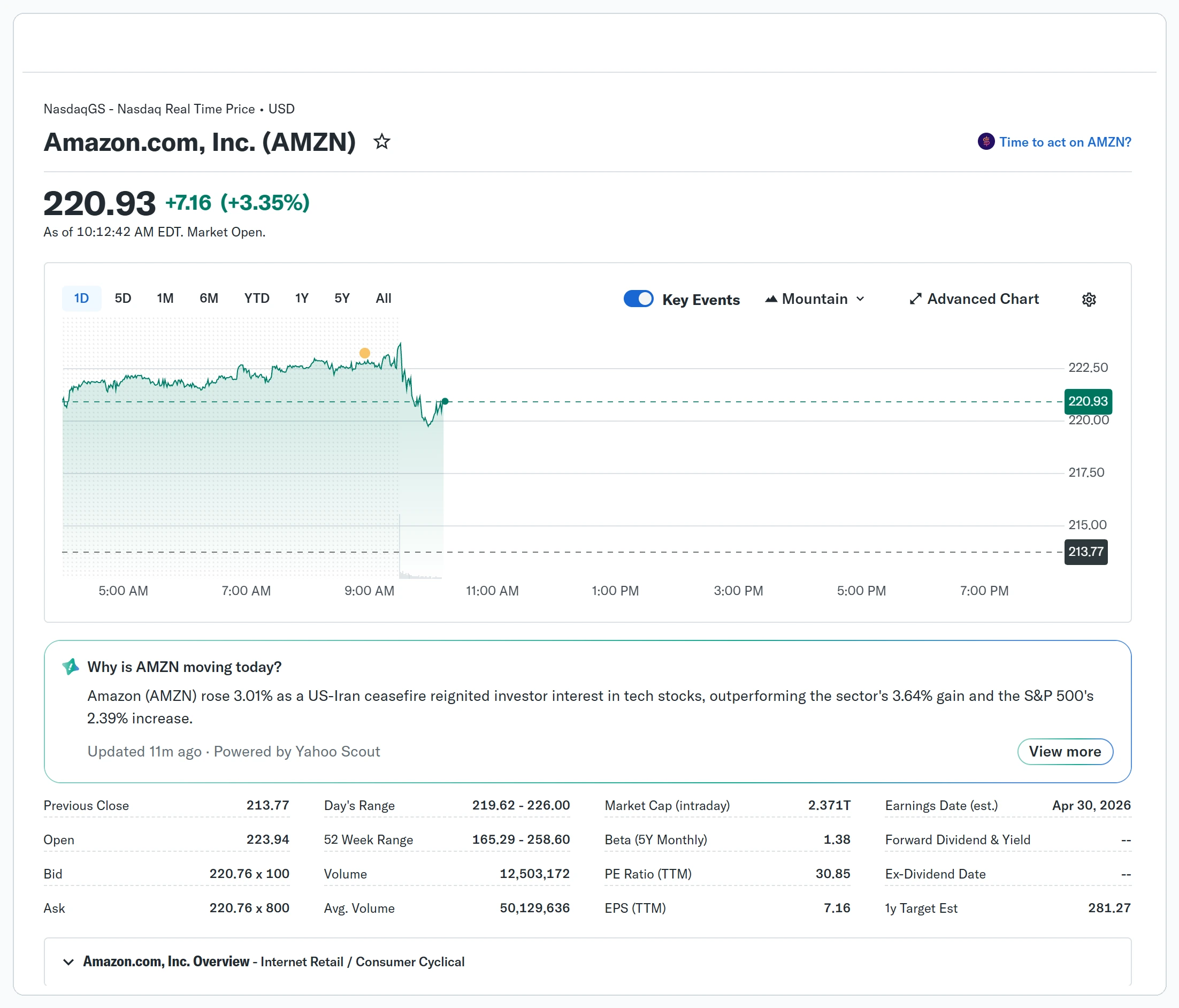

The hero image carries the market quote context. The body evidence avoids repeating that panel and focuses on the two official checks that matter most for the thesis: AWS operating income and free-cash-flow conversion under heavier capex.

Source capture: Amazon 2025 Form 10-K, captured 2026-04-08 from the AWS segment table. The marked row shows AWS operating income of $45.6 billion in 2025.

Open source.

Source capture: Amazon 2025 Form 10-K, captured 2026-04-08 from the AWS segment table. The marked row shows AWS operating income of $45.6 billion in 2025.

Open source.

The free-cash-flow reconciliation is kept as a linked source note instead of a second ultra-wide table crop: Source capture: Amazon 2025 Form 10-K, captured 2026-04-08 from the free-cash-flow reconciliation. The cited values are $139.5 billion of operating cash flow, $128.3 billion of net property-and-equipment purchases, and $11.2 billion of free cash flow.

What the Street is Pricing

The market is already giving Amazon credit for being one of the major platforms in cloud and AI infrastructure. That is why the 2026 hurdle is higher. A reaccelerating AWS segment is necessary, but it is no longer enough by itself.

The constructive evidence starts with AWS. Full-year net sales rose to $128.7 billion, and Q4 sales rose 24% to $35.6 billion. AWS operating income rose to $45.6 billion, so the segment is not merely buying growth with low-margin capacity. It is still a major profit engine.

The complication is that Amazon is spending into that demand very aggressively. The company said the year-over-year decline in free cash flow was primarily due to a $50.7 billion increase in purchases of property and equipment, largely tied to artificial intelligence investment.

That makes the evidence bar different from a normal growth-cycle story. Amazon does not need to prove that AWS has demand; the Form 10-K and Q4 release already show that. It needs to prove that incremental infrastructure produces durable customer lock-in, higher service density, and enough utilization to make the free-cash-flow dip look temporary rather than structural.

So the market is pricing two things at once: AWS as a durable AI infrastructure platform, and Amazon as a company that can absorb a much heavier capex cycle without permanently weakening free-cash-flow conversion.

Risks to the Thesis

The first risk is that capex arrives before utilization. A $200 billion capex year can still be rational, but only if capacity, customer demand, and AI services convert into revenue with enough visibility. If deployment runs ahead of monetization, the stock can be pressured even while AWS remains healthy.

The second risk is margin mix. AWS operating income is large, but Amazon specifically noted that higher technology infrastructure spending partly offset the benefit from higher AWS sales. That line matters because it shows the profit pool is already absorbing a heavier infrastructure load.

The third risk is free-cash-flow interpretation. Operating cash flow of $139.5 billion confirms a powerful business, but free cash flow of $11.2 billion shows how much capex can change the shareholder-return lens. A wide gap can be tolerated for a while. It cannot be ignored indefinitely.

What Flips the Call

The case strengthens if AWS stays near the current growth range, AI services improve utilization, and management gives clearer evidence that the 2026 capex plan is producing high-return capacity rather than simply matching rival spending.

The case weakens if AWS growth slows before the capex wave produces visible returns, free-cash-flow conversion stays compressed without better return evidence, or management's explanation shifts from demand capture to capacity catch-up.

Quarterly evidence should therefore focus less on the headline capex number and more on utilization, backlog conversion, and whether AWS profit expands after the spending step-up.

That is the clean AMZN read for 2026. AWS momentum is real, the cash engine is real, and the capex bar is also real. The 2026 framework now has to show that all three can coexist.