Market & Macro

AMD Data Center Growth: The Profit Test After Q1 2026

AMD Data Center produced 74.6% of Q1 2026 revenue growth and $1.599B of segment operating income. The next test is whether Q2 revenue converts into margin and cash.

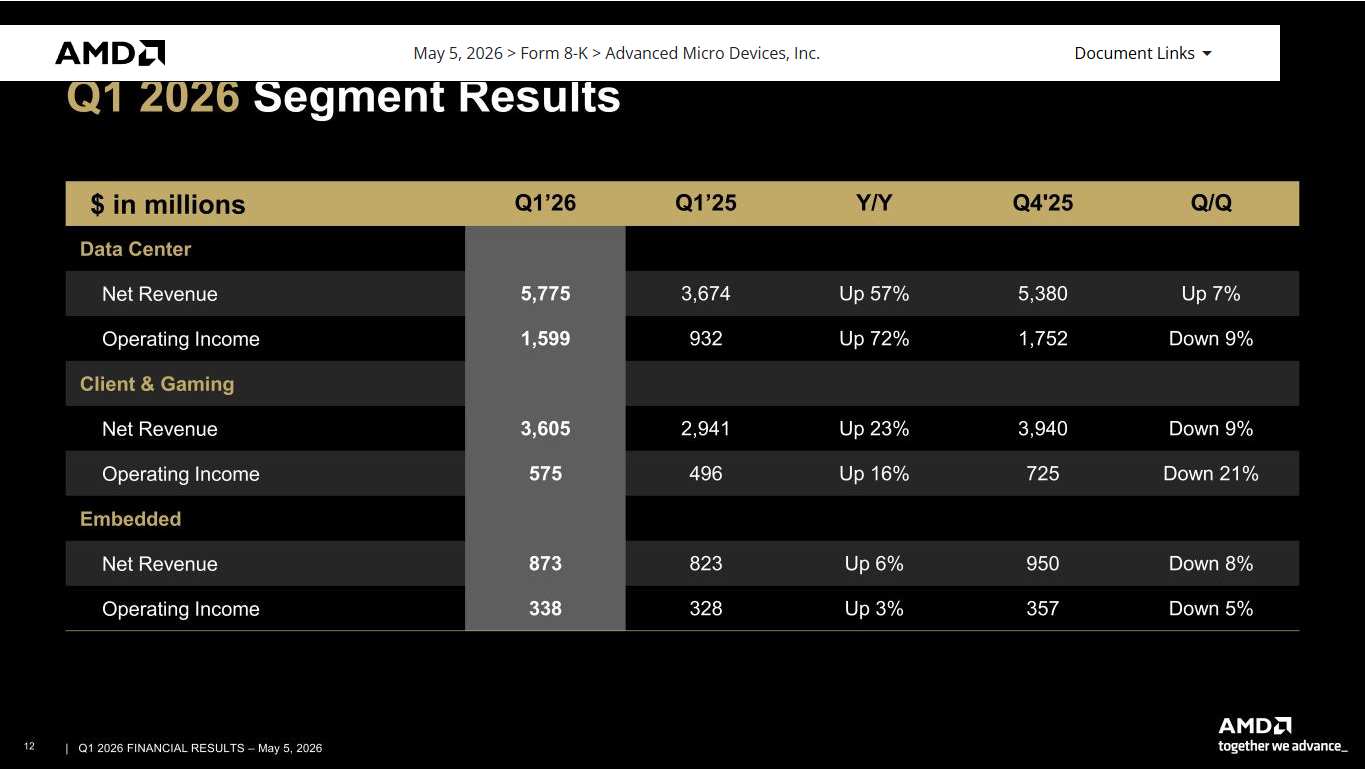

AMD's Data Center business is no longer a side bet inside a PC-chip company. In Q1 2026, it produced $5.775B of revenue—56.3% of AMD's total—and about 74.6% of the company's year-over-year revenue increase. It also generated $1.599B of segment operating income.

The harder question is what the stock already assumes. A July 14 market snapshot placed AMD near an $881.7B market value. Against approximately $37.454B of trailing reported revenue, that is about 23.5 times revenue before adjusting for net cash. The next filing therefore has to prove more than demand: it has to show that Data Center scale reaches segment margin and company cash flow.

Source-derived visual: AMD Q1 2026 results. Percentages use AMD's reported revenue and segment operating-income values; calculations are editorial.

| The 30-second answer | Verified evidence | What remains unproven |

|---|---|---|

| Data Center is AMD's growth engine | 56.3% of revenue; 74.6% of year-over-year growth | How durable the accelerator and server mix will be |

| The segment is already profitable | $1.599B operating income; 27.7% margin | Whether margin expands with the next revenue step |

| Cash conversion was strong | $2.566B free cash flow; 25.0% margin | Whether Q1 working-capital benefits repeat |

Thesis

The evidence supports a two-part thesis. First, EPYC server CPUs and Instinct accelerators have made Data Center the dominant source of AMD's reported growth. Second, the current equity value requires that growth to compound into a much larger profit and cash-flow base than one quarter can establish.

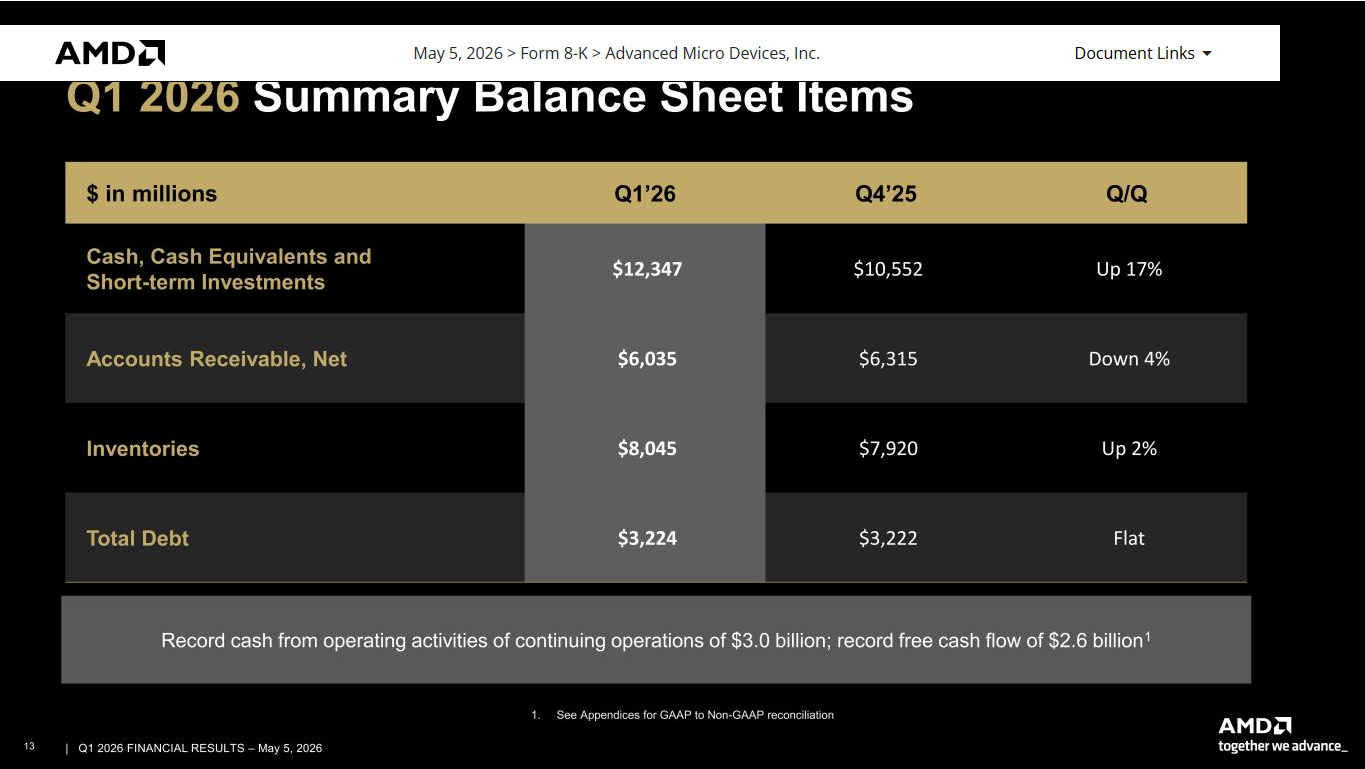

This is not a “revenue without profit” story. Data Center operating margin improved from about 25.4% in Q1 2025 to 27.7% in Q1 2026. AMD also reported record operating cash flow of $2.955B and free cash flow of $2.566B. Those facts are strong counterevidence to the simplest bear case.

But the segment-to-company bridge exposes the remaining work. Data Center operating income equaled 108.3% of consolidated GAAP operating income because Client and Gaming and Embedded profits were offset by $1.036B of central and other costs. The investment question is therefore not whether AI demand exists. It is whether AMD can scale its largest profit pool faster than the costs and capital required to support it.

Source Evidence Snapshot

AMD's official segment table is the cleanest starting point. Data Center revenue rose 57% year over year to $5.775B. Segment operating income rose 72% to $1.599B. Client and Gaming and Embedded also remained profitable, so the company is not dependent on a single segment for every operating dollar.

2026-05-05, captured 2026-07-14. Values are USD millions.The growth contribution is more revealing than the headline growth rate. Total revenue increased from $7.438B to $10.253B, a gain of $2.815B. Data Center increased from $3.674B to $5.775B, a gain of $2.101B. Dividing those two changes produces an estimated 74.6% contribution.

Source-derived visual: AMD Q1 2026 results and the same release's Q1 2025 comparisons. Calculation: (5.775 − 3.674) / (10.253 − 7.438) = 74.64%. Company values are rounded.

That 74.6% figure does not mean every Data Center dollar is AI-accelerator revenue. AMD says growth was driven by EPYC processors and Instinct GPUs, but it does not report those product families as separate revenue lines. Readers should not turn a segment number into a product number. The site's guide to reading AI revenue claims explains why the denominator matters.

For a cross-company view of realized results, guidance, and long-term targets, use the AI infrastructure evidence map before comparing headline figures.

The profit bridge adds a second boundary. AMD reports segment operating income before central and other items. Adding the three segment profits and subtracting the $1.036B all-other loss reconciles to $1.476B of consolidated GAAP operating income.

Source-derived visual: AMD Q1 2026 Form 10-Q. The bridge uses $1.599B + $0.575B + $0.338B − $1.036B = $1.476B.

Cash conversion was the strongest company-level evidence in the quarter. AMD ended Q1 with $12.347B of cash, cash equivalents, and short-term investments versus $3.224B of total debt. It generated $2.955B of operating cash flow from continuing operations and $2.566B of free cash flow after $389M of property-and-equipment purchases.

2026-05-05, captured 2026-07-14. Values are USD millions; free cash flow is AMD's non-GAAP measure reconciled in the appendix.What the Street Is Pricing

This article does not use a private consensus database, analyst price targets, or a rating. It uses a dated market snapshot to show the size of the expectation embedded in the equity value.

At 10:31 UTC on July 14, Investing.com's AMD quote showed $534.39 per share and an indicated market value near $881.7B. Market prices move continuously; this is a timestamp, not a permanent valuation input.

| Valuation bridge | Value | Boundary |

|---|---|---|

| FY2025 revenue | $34.639B | Company-reported |

| Add Q1 2026 revenue | +$10.253B | Company-reported |

| Remove Q1 2025 revenue | −$7.438B | Company-reported |

| Approximate trailing revenue | $37.454B | Article calculation |

| Market value / trailing revenue | ~23.5× | Snapshot; not enterprise value or a forward multiple |

A high revenue multiple does not prove overvaluation on its own. It indicates that investors are paying for future growth, margin expansion, and competitive durability that trailing statements cannot yet contain. AMD's record Q1 free cash flow makes that expectation more credible, while the size of the multiple makes misses more consequential.

The useful interpretation is conditional: if Data Center remains most of incremental growth and its operating margin expands, consolidated profit can scale quickly. If revenue grows but segment margin stalls or central costs consume the incremental profit, the current expectation becomes harder to defend.

Risks to the Thesis

The first risk is product-mix opacity. Data Center combines EPYC CPUs and Instinct GPUs. Both can grow while carrying different margins, supply requirements, and customer timing. The segment result proves economics at the combined level, not for either product family.

The second risk is execution and supply. AMD's filing identifies export controls, memory and component availability, third-party manufacturing, yields, and large-customer dependence among material risks. Those are not generic disclaimers when accelerator ramps require advanced packaging, high-bandwidth memory, and synchronized system deployments.

The third risk is working capital. Inventory reached $8.045B, up 2% from Q4, while quarterly revenue was flat sequentially. That does not establish excess inventory; it may support future ramps. It does mean free-cash-flow quality should be tested again when Q2 revenue arrives.

The fourth risk is cost absorption. Data Center supplied more segment operating income than AMD retained at the consolidated operating line. Stock-based compensation, acquired-intangible amortization, research investment, and other central costs can keep company earnings from scaling as quickly as segment revenue.

| Risk path | Current evidence | What would make it worse |

|---|---|---|

| Product mix | One Data Center segment | Faster revenue with no margin improvement |

| Supply and deployment | Large CPU and GPU ramps | Delays, constrained HBM/packaging, or guide slippage |

| Working capital | $8.045B inventory | Inventory rises faster than revenue and cash flow falls |

| Central costs | $1.036B all-other loss | Segment profit grows but consolidated margin stalls |

| Expectation risk | ~23.5× trailing revenue snapshot | Any combination of slower growth and weaker cash conversion |

What Flips the Call

AMD will report Q2 2026 results after the market close on August 4. Management guided revenue to $11.2B plus or minus $0.3B and non-GAAP gross margin to about 56%. Those are company targets. The segment-margin and cash tests below are editorial monitoring thresholds, not AMD guidance.

Source-derived decision visual: AMD Q1 2026 results and AMD's Q2 reporting-date announcement. Only the revenue range is company guidance.

The conclusion becomes more constructive if revenue reaches the guided range, Data Center operating margin rises above Q1's 27.7%, and free cash flow grows with revenue without a disproportionate inventory build. That combination would show scale reaching both the segment and the company.

The conclusion weakens if revenue falls below $10.9B, or if Data Center revenue grows while its operating margin remains at or below 27.7%. It also weakens if free cash flow drops materially because working capital absorbs the benefit of higher sales.

The decision boundary is simple: AMD has already proved that Data Center is the growth engine. On August 4, it must show that the engine is becoming a larger source of profit and cash—not merely a larger source of revenue.

Methodology, Sources & Disclosure

This article separates company-reported results, company guidance, third-party market data, article calculations, and editorial monitoring thresholds. Growth contribution divides the Data Center revenue change by the consolidated revenue change. The profit bridge reconciles reported segment operating income to consolidated GAAP operating income. The trailing-revenue calculation adds Q1 2026 and removes Q1 2025 from FY2025 revenue.

- AMD Q1 2026 financial results,

2026-05-05 - AMD Q1 2026 earnings slides,

2026-05-05 - AMD Form 10-Q for the quarter ended 2026-03-28, filed

2026-05-06 - AMD FY2025 financial results,

2026-02-03 - AMD Q2 2026 reporting-date announcement,

2026-07-08 - Investing.com AMD market snapshot, observed

2026-07-14 10:31 UTC

Facts and links were rechecked as of 2026-07-14. AI assisted with structure and consistency checks; the official sources, calculations, captures, EN/KO parity, and final wording require human review before production deployment. No sponsorship or affiliate relationship with AMD is disclosed. This is general information, not individualized investment advice; it does not issue a rating or share-price objective.