Market & Macro

SpaceX IPO in 2026: Public S-1 Versus ETF Proxy Demand

SpaceX's public S-1 was filed on May 20, 2026, shifting the 2026 IPO debate from pre-filing anticipation and Korean ETF packaging toward disclosure quality, valuation discipline, governance, and float risk.

(Sources: SEC EDGAR filing detail for Space Exploration Technologies Corp Form S-1 filed May 20, 2026, SpaceX S-1 registration statement, Reuters via Yahoo Finance on SpaceX IPO details, Reuters via Yahoo Finance on a valuation above $2 trillion, The Korea Times on space-themed ETFs in Korea)

Thesis

The SpaceX IPO story changed materially on May 20, 2026. The older pre-filing framing - retail excitement running ahead of a nonpublic S-1 - is no longer accurate. The SEC filing-detail page now shows a public Form S-1 for Space Exploration Technologies Corp, accepted on May 20, 2026, under accession number 0001628280-26-036936.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

That does not make the analysis simpler. It makes the diligence harder. Before the S-1, the risk was that market participants were reacting to headlines without a filing. After the S-1, the risk is that ETF packaging, retail allocation narratives, and valuation talk keep moving faster than readers can parse the actual disclosure.

Source Evidence Snapshot

The hero image now carries the official SEC filing-detail page. The body evidence assigns two supporting roles: the pre-filing valuation narrative and the Korean ETF packaging signal. The article no longer repeats generic SpaceX operating images because the S-1 is now the primary source.

Report-grade citation: The SEC EDGAR filing detail page lists Space Exploration Technologies Corp as filer, Form S-1, filing date 2026-05-20, accepted time 2026-05-20 16:40:21, and the linked S-1 document. This supersedes the old pre-public-filing frame.

What the Street is Pricing

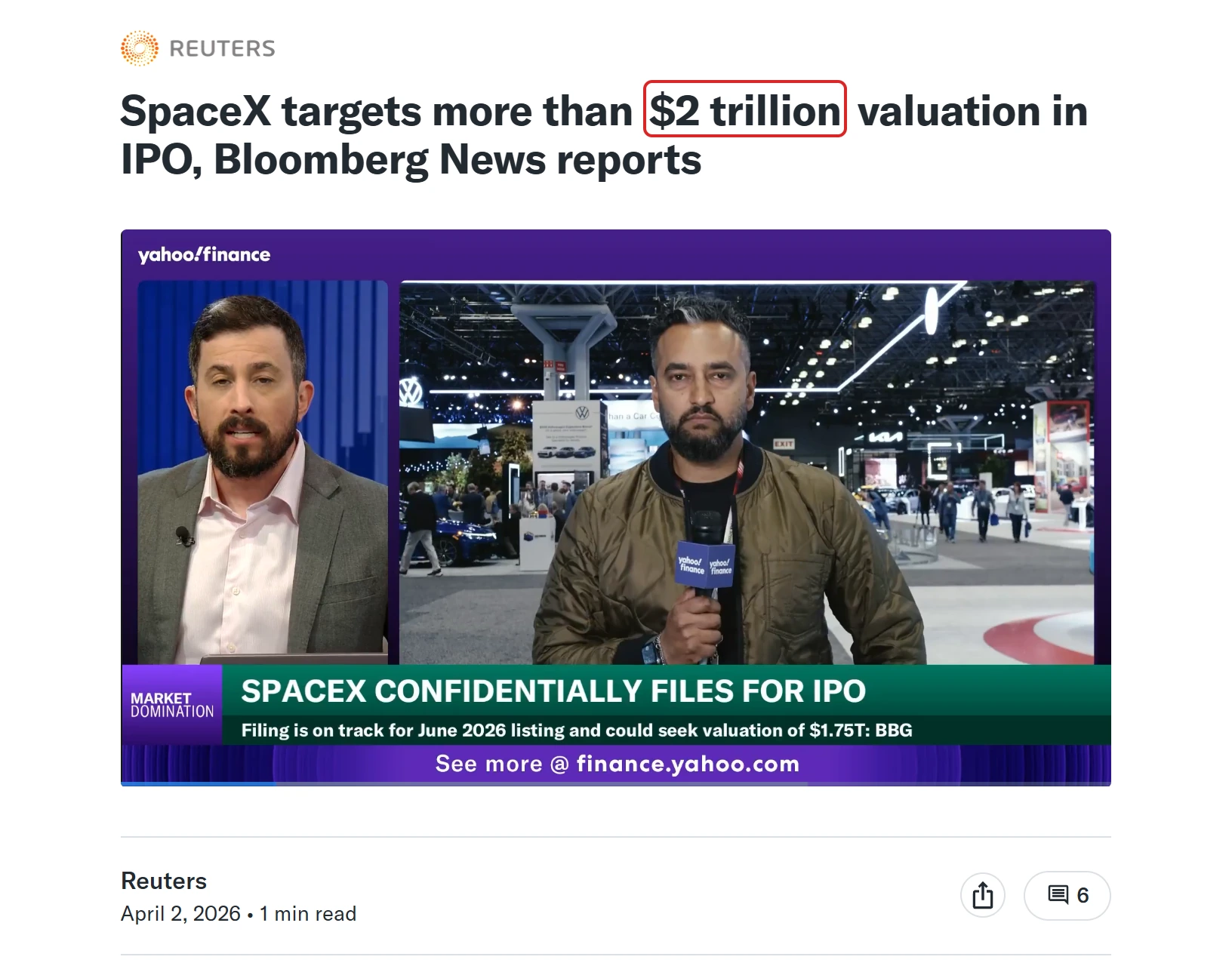

There is no ordinary sell-side valuation table for a company that is not yet trading. What the market is pricing is visible through reported valuation talk, expected retail access, and proxy demand. Earlier Reuters reporting described an aggressive IPO setup and later reports pointed to valuation figures moving above $2 trillion; Korean ETF managers were already packaging space-themed exposure before the S-1 became public.

Now that the S-1 is public, that same demand has to be tested against filing evidence. The important question is not whether SpaceX has a powerful brand or an intense investor following. It does. The question is whether public investors can stay disciplined around valuation, governance, float, and risk-factor disclosure after the filing becomes readable.

This is also why proxy products need tighter language. A space-themed ETF can express demand for the SpaceX narrative, but it is not the same as direct SpaceX economics. After May 20, the right comparison is no longer "ETF wrapper demand versus no filing." It is "ETF wrapper demand versus the actual S-1."

That frame also protects readers from a common IPO mistake. Scarcity can make a deal feel de-risked because everyone appears to want access. It does not answer whether the first public float is large enough, whether governance terms leave minority holders with ordinary protections, or whether the final price range already capitalizes several years of execution. Those are filing questions, not brand questions.

Risks to the Thesis

| Risk | Confirming signal |

|---|---|

| Filing risk | S-1 amendments add or sharpen risk factors, governance constraints, or offering terms that weaken the first valuation story. |

| Valuation discipline breaks | Reported valuation talk keeps rising even if the S-1 does not support the same risk-adjusted economics. |

| Float and allocation distort trading | A small effective float or heavy retail allocation creates price action that reflects scarcity more than fundamentals. |

| ETF wrappers overstate exposure | Korean or global space-themed funds market the SpaceX theme while holding mostly adjacent companies or indirect proxies. |

The core risk is no longer lack of a filing. It is the gap between the emotional clarity of the SpaceX brand and the slower, less exciting work of underwriting a public registration statement.

What Flips the Call

The next trigger is the first meaningful S-1 amendment and the final offering mechanics: price range, share count, float, lockup, governance terms, and any updated risk-factor language. Those details will decide whether the current demand looks like disciplined public-market underwriting or a scramble for scarce exposure.

The call improves if amendments clarify the offering without adding material new concerns and if the price range leaves room for public investors to underwrite risk rather than simply chase scarcity. The call weakens if amendments sharpen governance or concentration concerns while valuation talk remains detached from the filing.

SpaceX IPO demand is real, but the public S-1 moved the debate from anticipation to evidence. Every ETF wrapper or proxy exposure should now be held against that filing record.