Market & Macro

Tesla Stock in 2026: Physical AI Ambition Versus Auto Margin Evidence

Tesla's Q4 2025 update pairs a $44.1 billion cash base and physical AI roadmap with falling automotive revenue. The 2026 issue is whether robotaxi and Optimus evidence can support a trillion-dollar valuation without treating SpaceX as Tesla revenue.

(Sources: Google Finance quote page for Tesla, Tesla Q4 and Full Year 2025 Update, SpaceX Falcon User's Guide)

Thesis

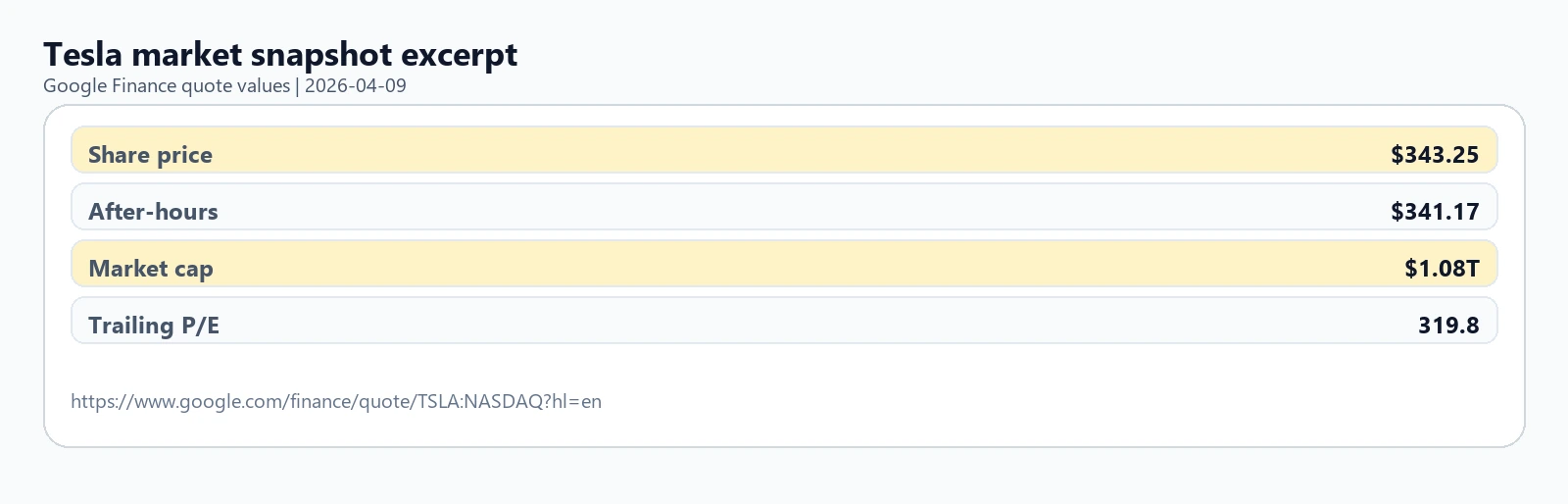

Tesla's 2026 equity setup is not a clean auto recovery story. The captured quote page showed a roughly $1.08 trillion market cap while Tesla's own Q4 2025 update showed automotive revenue still falling. That gap is the evidence burden: the market is paying for a physical AI platform before the non-auto contribution is fully visible in the numbers.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

The defensible read is narrower than the usual Tesla-versus-SpaceX narrative. SpaceX can explain why the market keeps giving Elon Musk-led programs execution credit, but Tesla's filings do not make SpaceX a Tesla revenue source. The stock still has to earn its own premium through robotaxi, Optimus, energy, AI infrastructure, and better automotive margin evidence.

Source Evidence Snapshot

The quote page showed Tesla at $343.25, after-hours trading at $341.17, and a market cap of roughly $1.08 trillion. That is the correct starting point. Tesla was not being priced like a normal cyclical auto maker in this snapshot.

The company evidence is more mixed than the valuation headline. Q4 2025 automotive revenue was $17.693 billion, down 11% year over year. Total revenue was $24.901 billion, down 3%. Operating margin was 5.7%, operating cash flow was $3.813 billion, and cash, cash equivalents, and investments ended the quarter at $44.059 billion.

This is not a weak balance-sheet story. It is also not a clean auto-growth story. Tesla's own numbers force the article to separate financial resilience from valuation support.

The article now leaves the Falcon visual evidence in the dedicated SpaceX IPO piece. Here, SpaceX is only a cited execution-context source. The relevant boundary is simple: SpaceX documents operational scale under the same founder, but Tesla's own filings do not disclose SpaceX revenue in Tesla's operating model.

What the Street is Pricing

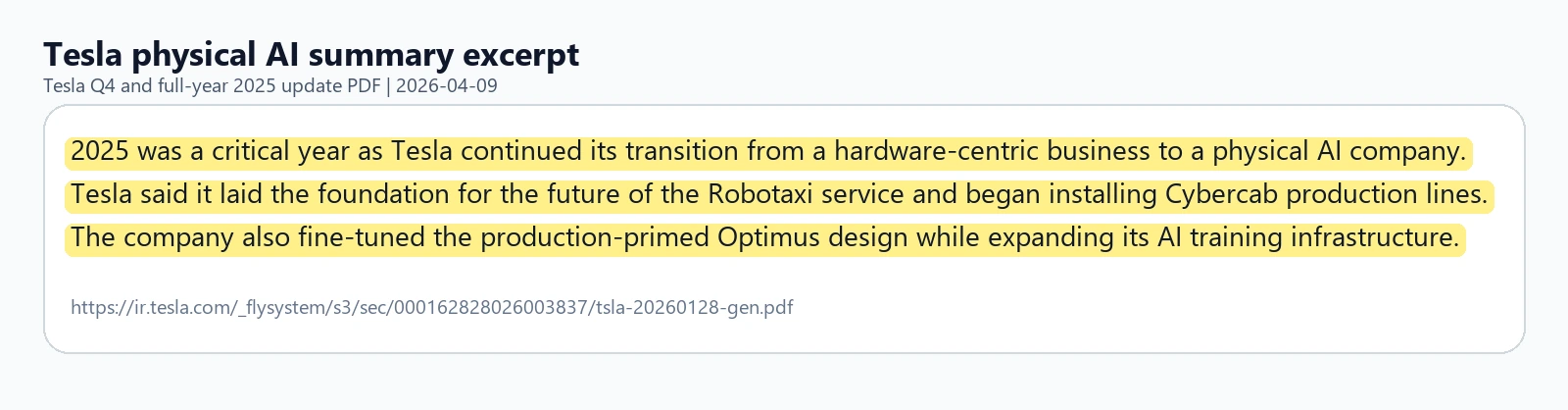

The market is pricing Tesla as an operating company plus a long-dated option on physical AI. That option is visible in Tesla's own language. The Q4 2025 update said 2025 was a critical year in the company's transition from a hardware-centric business to a physical AI company, and it highlighted FSD (Supervised), Robotaxi service, Cybercab production-line installation, Optimus development, and expanded AI training infrastructure.

That framing explains why the valuation discussion does not stop at auto revenue. If the market valued Tesla only on the Q4 automotive line, the market-cap figure would be much harder to reconcile. The premium depends on the belief that Tesla can turn vehicles, autonomy, robots, energy systems, and AI compute into a broader real-world platform.

Public consensus valuation data was not part of the reviewed evidence, so this is not an article about a single valuation output. The observable market evidence here is the captured market cap, the official company financial table, and Tesla's own physical AI framing.

That makes the next few quarters less about slogan quality and more about whether the physical AI language starts producing measurable operating markers.

Risks to the Thesis

The first risk is that the physical AI story stays mostly narrative. Robotaxi, Cybercab, and Optimus language can support a premium only if commercialization evidence becomes more concrete. A roadmap is not the same thing as a durable revenue stream.

The second risk is that automotive weakness lasts longer than the market tolerates. Full-year automotive revenue fell 10%, and Q4 automotive revenue fell 11%. A high cash balance helps fund the roadmap, but it does not erase pressure in the core business.

The third risk is that the SpaceX halo gets overused. SpaceX's Falcon record is useful context for how the market thinks about founder-led execution. It is not a Tesla asset, Tesla segment, or Tesla cash-flow source. Treating it like one would weaken the stock thesis.

The fourth risk is valuation compression. Even a strong technology company can underperform if the market prices in too much operating progress before the operating data arrives.

What Flips the Call

The thesis improves if Tesla shows measurable robotaxi expansion, clearer Optimus commercialization milestones, stable or improving automotive margin, and cash generation that keeps funding the roadmap without stressing the balance sheet. In that case, the physical AI premium would have more operating support.

The thesis weakens if automotive revenue keeps declining, robotaxi and Optimus remain mostly promotional, or quarterly cash generation deteriorates while the market cap still assumes platform-level success.

Tesla still trades with a premium that auto revenue alone does not explain. The premium is not automatically wrong, but it now needs company-specific operating evidence. SpaceX can explain part of the market's willingness to wait; it cannot do Tesla's evidence work for it.