Market & Macro

Alphabet Stock in 2026: Cloud Profits Versus the AI Capex Ramp

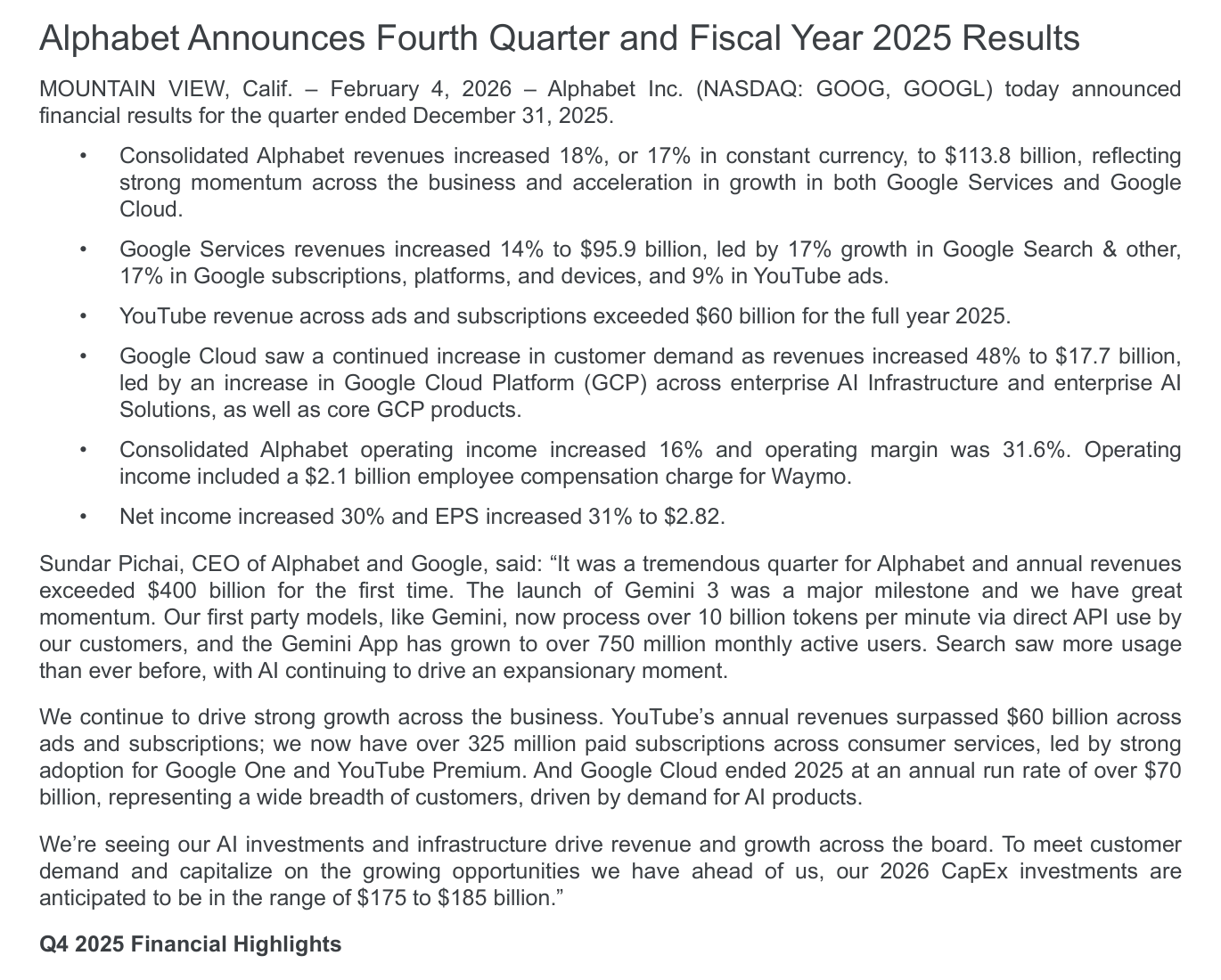

Alphabet's Q4 2025 release showed 48% Google Cloud revenue growth, $5.3 billion of Cloud operating income, and 2026 capex guidance of $175-$185 billion. The 2026 question is whether Search cash flow and Cloud profit stay visible as AI infrastructure spending rises.

(Sources: Alphabet Q4 2025 earnings release PDF, Google Finance GOOG quote page)

Alphabet is no longer only a Search resilience story. The Q4 2025 release makes the 2026 valuation debate more specific: Google Cloud is now large and profitable enough to matter, but the AI infrastructure bill is also large enough to demand proof.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

The official release said Q4 revenue rose 18% to $113.8 billion, net income rose 30% to $34.5 billion, and Google Cloud revenue rose 48% to $17.7 billion. It also said Google Cloud ended 2025 at an annual run rate above $70 billion.

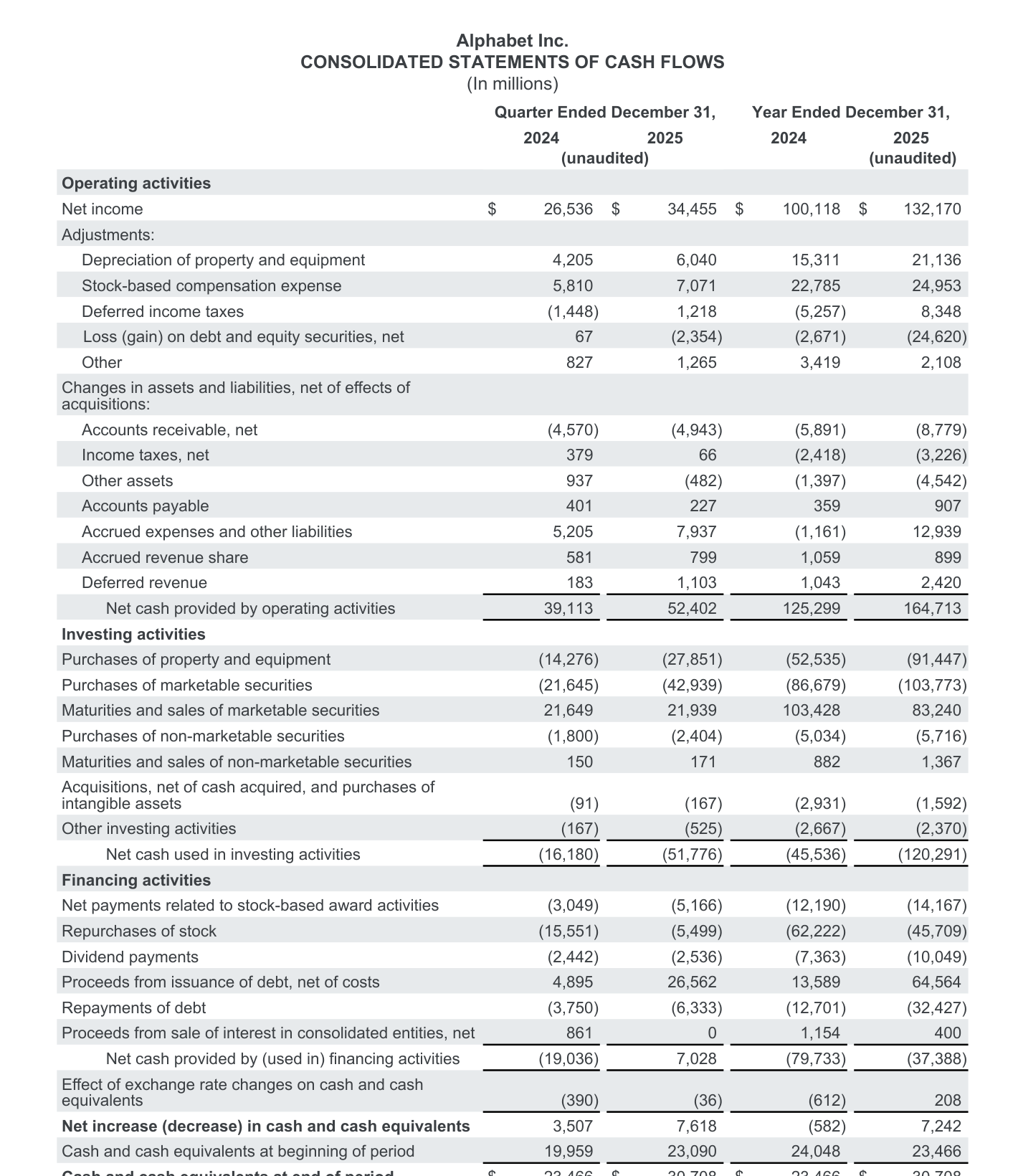

That operating evidence is strong. The same document, however, guided 2026 capital expenditures to $175 billion to $185 billion, after 2025 purchases of property and equipment of $91.4 billion. That is why the right question is not whether Alphabet can spend. It is whether Search cash flow, Cloud profit, and AI monetization can keep the returns on that spend visible.

Thesis

Alphabet's 2026 setup is evidence-supported but more demanding. Search and Google Services still supply the core cash engine, while Google Cloud now contributes a real profit pool. That combination can support a larger AI buildout, but only if the business keeps showing operating leverage as capex rises.

The evidence is not a simple bull case. It is a return-on-capital case. Cloud revenue and operating income show that the AI and cloud push is already producing measurable profit. The 2026 capex range means the analysis should assume a much heavier infrastructure year. The stock needs both sides of that equation to remain true.

Source Evidence Snapshot

The hero image carries the capex-guidance excerpt. The body evidence focuses on the two operating checks that keep the investment debate grounded: Cloud profitability and cash-flow capacity.

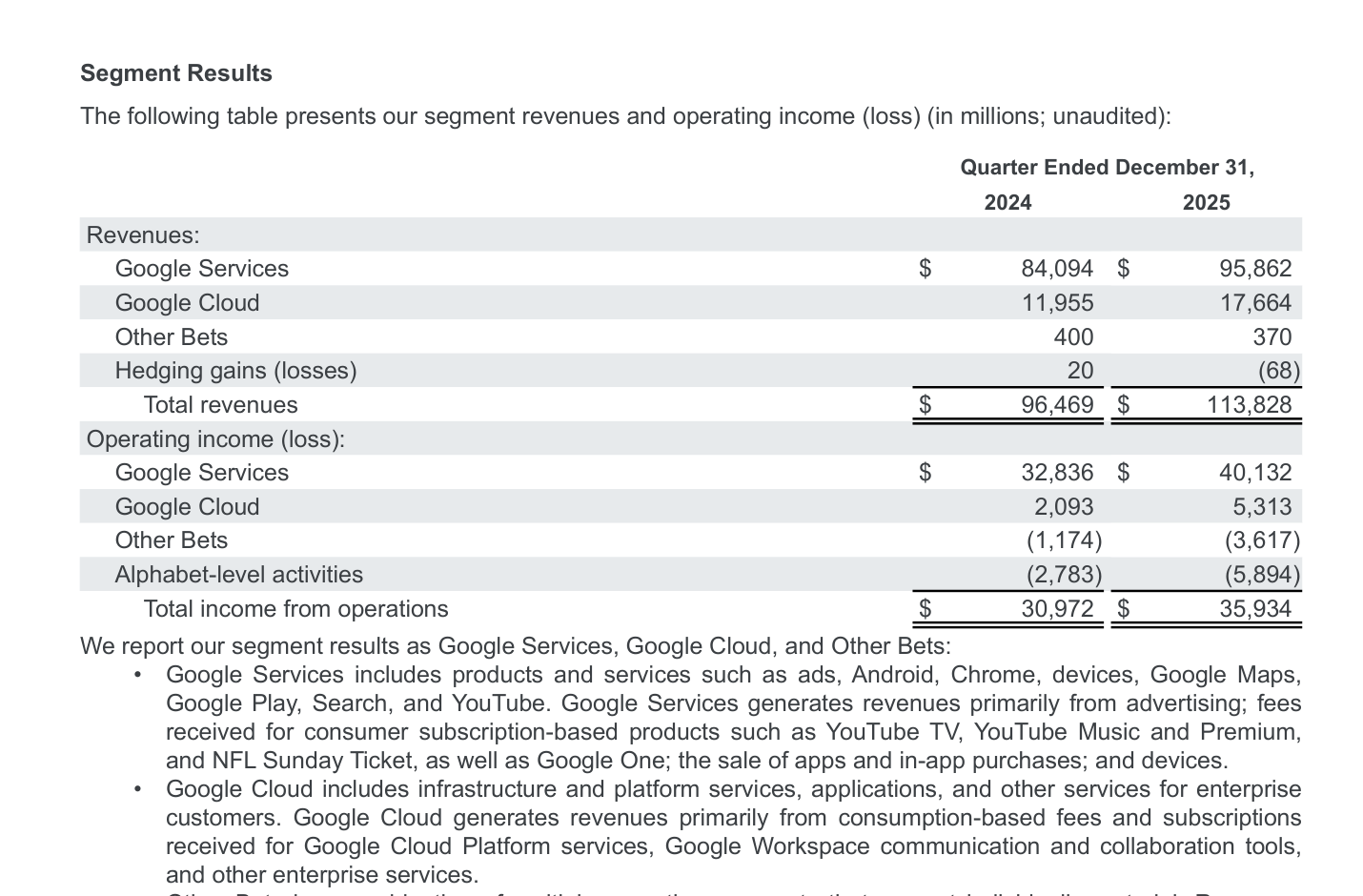

Source capture: Alphabet Q4 2025 earnings release, captured 2026-04-08 from the segment results table. The marked rows show Google Cloud revenue of $17.7 billion and Google Cloud operating income of $5.3 billion.

Open source.

Source capture: Alphabet Q4 2025 earnings release, captured 2026-04-08 from the segment results table. The marked rows show Google Cloud revenue of $17.7 billion and Google Cloud operating income of $5.3 billion.

Open source.

Source capture: Alphabet Q4 2025 earnings release, captured 2026-04-08 from the cash-flow statement. The marked lines show $52.4 billion of Q4 operating cash flow and $91.4 billion of 2025 purchases of property and equipment.

Open source.

Source capture: Alphabet Q4 2025 earnings release, captured 2026-04-08 from the cash-flow statement. The marked lines show $52.4 billion of Q4 operating cash flow and $91.4 billion of 2025 purchases of property and equipment.

Open source.

What the Street is Pricing

The market is no longer treating Alphabet like a company with no AI option. That is the right starting point. The debate is whether the current premium is supported by business-unit evidence rather than by AI language alone.

Google Cloud is the cleanest proof point. Revenue reached $17.7 billion in the quarter, operating income reached $5.3 billion, and the annual run rate moved above $70 billion. That means Cloud is no longer a side story. It is now large enough to influence Alphabet's margin and capital-allocation narrative.

Search still matters even more. Google Services revenue was $95.9 billion in the quarter, and the broader company generated $52.4 billion of operating cash flow. Those numbers explain why Alphabet can fund a large buildout without a near-term funding problem.

That cash engine also changes how the capex question should be judged. A smaller company would be evaluated first on financing risk. Alphabet should be evaluated first on evidence quality: whether Cloud utilization, Search monetization, and AI product adoption are visible enough to make the larger capital base look intentional rather than defensive.

The stock is therefore pricing a balance: Search remains durable, Cloud keeps compounding, and AI infrastructure improves both businesses over time. If that balance holds, the capex ramp can look like reinvestment. If it breaks, the same capex ramp becomes the first valuation pressure point.

Risks to the Thesis

The main risk is not that Alphabet lacks cash. It is that spending rises faster than visible returns. A 2026 capex range of $175 billion to $185 billion is too large to leave in the footnotes. It has to produce evidence in Cloud growth, AI product usage, Search monetization, or operating leverage.

The second risk is that Cloud profit expansion slows while infrastructure intensity remains high. A fast-growing but less profitable Cloud segment would make the AI buildout feel more like a margin drag than a growth engine.

The third risk is timing. Even if AI demand is real, data-center capacity, chips, power, and internal deployment can arrive unevenly. If the cost curve shows up before the revenue curve, the market can compress the multiple before the long-term thesis has failed.

What Flips the Call

The case strengthens if Google Cloud keeps growing at a high rate while operating income expands, Google Services keeps producing large operating cash flow, and management ties the capex range to concrete demand indicators rather than broad AI ambition.

The case weakens if capex guidance rises again without matching Cloud operating leverage, Search monetization softens, or Alphabet has to explain the buildout more as capacity catch-up than as profitable demand capture.

That is the cleanest read for GOOG in 2026. Alphabet has the cash engine and the Cloud proof points to defend a major AI buildout. The test is whether the earnings curve remains visible while the capex curve rises.