Market & Macro

Broadcom AI Revenue: Nearly Half the Company, Mix Still Hidden

Broadcom AI semiconductor revenue reached $10.8B, about 48.7% of Q2 FY2026 revenue and roughly 88.5% of annual growth, but accelerator, networking, margin, and customer concentration remain hard to separate.

Broadcom's AI growth is real and financially dominant. In Q2 FY2026, AI semiconductor revenue reached $10.8B, or about 48.7% of $22.187B in total revenue. A source-derived bridge suggests AI produced roughly 88.5% of the company's year-over-year dollar increase.

The missing evidence matters just as much. Broadcom combines custom AI accelerators and AI networking in the same number, and it does not disclose product-level AI revenue or AI-specific margins. Investors can verify the scale of the engine, but not yet which component powers it or at what profitability.

For a denominator-matched view, the AI infrastructure evidence map compares this realized but aggregated figure with Nvidia's reported Data Center revenue and Qualcomm's future goal.

Source-derived visual: Broadcom Q2 FY2026 financial results. Editorial calculation: $10.8B / $22.187B = 48.68%. The company identifies custom accelerators and AI networking as growth drivers but does not provide their individual revenue.

| The 30-second answer | Verified evidence | Still missing |

|---|---|---|

| AI is now a company-scale engine | $10.8B and 143% year-over-year growth | Accelerator versus networking split |

| The next step is larger | Q3 FY2026 AI guide of $16.0B | AI-specific gross or operating margin |

| Concentration is material | One distributor at 42%, up from 29% | Final end-customer economics by AI program |

Thesis

The correct thesis has two parts. First, Broadcom has converted AI demand into reported revenue at a scale that now explains most of the company's growth. Second, the disclosure is not granular enough to tell whether that growth is balanced across accelerators and networking, or whether the expanding semiconductor mix improves long-run earnings quality.

That distinction prevents two common errors. Treating every AI dollar as equally durable ignores product mix, customer timing, and margin. Treating the combined number as too opaque to matter ignores the fact that it is already almost half of company revenue.

The investable question is therefore not “Is Broadcom exposed to AI?” It is whether the verified growth can remain large while product mix, margin quality, and concentration become easier—not harder—to underwrite.

Source Evidence Snapshot

The issuer's own statement sets the factual boundary. Broadcom reported $10.8B of AI semiconductor revenue, up 143%, driven by custom AI accelerators and AI networking. It also guided Q3 FY2026 AI semiconductor revenue to $16.0B, or growth above 200%.

2026-06-03, captured 2026-07-14. The image preserves the issuer's original wording and values.The statement proves scale and direction, not composition. It does not say how much of the $10.8B came from custom accelerators, how much came from networking, whether one grew faster, or whether either carries the consolidated semiconductor margin.

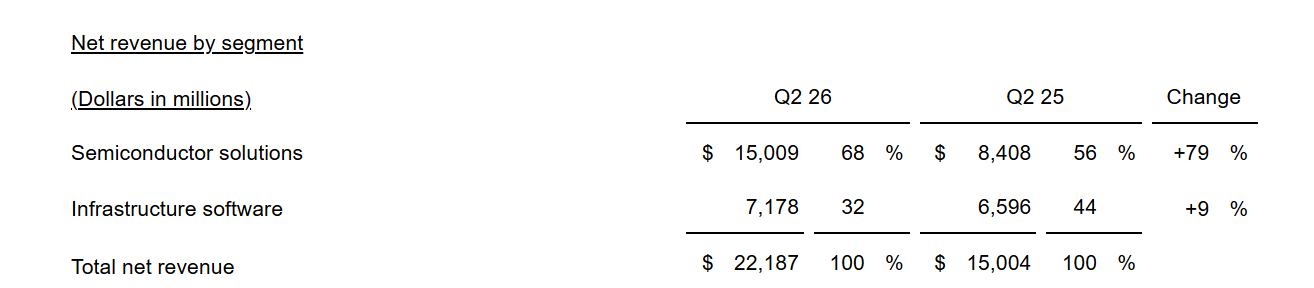

The segment table supplies the next layer. Semiconductor solutions revenue rose 79% to $15.009B, while infrastructure software rose 9% to $7.178B. Total revenue increased 48% to $22.187B.

2026-06-03, captured 2026-07-14; displayed source values are USD millions.AI therefore represented about 72.0% of semiconductor revenue. That ratio is large enough to establish AI as the center of the semiconductor segment, but it still cannot be used as an AI margin. Broadcom reports profitability for the broader segment, not for AI or either AI product family.

The year-over-year bridge adds decision value. The 143% growth rate implies prior-year AI revenue of approximately $4.444B: $10.8B / 2.43. AI therefore added about $6.356B, while total company revenue added $7.183B.

Source-derived visual: Broadcom Q2 FY2025 results and Q2 FY2026 results. The calculation is $6.356B / $7.183B = 88.48%; it is approximate because the AI revenue and growth rate are rounded.

Subtracting AI from total revenue leaves an approximate non-AI bucket of $11.387B this year versus $10.560B a year ago. That bucket grew about $0.827B, or 7.8%. It combines infrastructure software and non-AI semiconductor revenue, so it should not be mistaken for a reported segment.

What the Street Is Pricing

This article does not use a private consensus feed, a share-price target, or a valuation multiple. It therefore does not pretend to extract an exact probability from Broadcom's stock price. The observable underwriting problem is the value of a very fast-growing but incompletely separated AI engine inside a company that also owns a high-margin infrastructure software business.

The Form 10-Q shows the operating leverage. Semiconductor solutions operating income rose 93% to $9.281B from $4.806B. Infrastructure software operating income rose 13% to $5.647B from $4.987B. These segment values are before unallocated expenses and do not reveal AI profitability.

Explanation visual: Nex marks the boundary between company-reported evidence, reproducible calculations, and facts that remain undisclosed. The table below carries the actual decision labels.

| Evidence layer | What is known | What not to infer |

|---|---|---|

| Company-reported | AI revenue $10.8B; semiconductor revenue $15.009B | Accelerator or networking revenue |

| Article-calculated | AI share 48.7%; growth contribution about 88.5% | An audited AI subtotal or margin |

| Still undisclosed | Product split, AI-specific margin, program economics | That both AI product families have equal quality |

The comparison with neighboring AI-infrastructure names clarifies the market question. Nvidia already discloses a large networking business, although its new reporting lens weakens product-mix continuity. Qualcomm has made a large data-center target that still needs reported conversion. Broadcom sits between them: current AI revenue is proven, but the accelerator-versus-network composition is not.

What deserves a premium is not the label “AI.” It is a combination of verified growth, durable product attachment, good margins, and a customer base broad enough to reduce timing risk. Broadcom currently proves the first item most clearly.

Risks to the Thesis

Concentration is the strongest counterweight. Broadcom's Form 10-Q says direct sales to one semiconductor distributor represented 42% of total revenue, up from 29%. The top 5 end customers represented about 45% of first-half revenue, while distributors represented 56%.

Margin mix is the second risk. Consolidated GAAP gross margin was about 69%, versus 68% a year earlier. The filing says the higher semiconductor mix partly offsets margin benefits because semiconductor gross margin is lower than software gross margin.

The company still generated $10.262B of free cash flow, equal to 46% of revenue. That is strong counterevidence against a simple “growth without cash” bear case. It does not answer whether the next increment of AI revenue carries the same economics.

| Risk path | Current evidence | Signal that makes it worse |

|---|---|---|

| Product opacity | One combined AI number | No accelerator/networking split as AI becomes the majority |

| Distributor concentration | 42%, up from 29% | Concentration remains at or above the current level |

| End-customer timing | Top 5 at about 45% | A major program delay moves company-wide growth |

| Margin mix | 69% GAAP gross margin versus 68% prior | AI rises while gross margin falls below 68% |

| Supply and execution | Large custom programs require capacity and packaging | Revenue guidance slips because supply or ramps move out |

These risks interact. A concentrated program can create quarterly volatility, a large accelerator ramp can change the mix, and the combined AI disclosure can make the exact source of the change difficult to isolate.

What Flips the Call

Broadcom guided Q3 FY2026 total revenue to $29.4B and AI semiconductor revenue to $16.0B. If both land, AI would be about 54.4% of total revenue. That would move AI from nearly half to a majority of the company within one quarter.

Source-derived visual: Broadcom Q2 FY2026 results and Form 10-Q. The $14.7B majority line, 68% margin floor, and 42% concentration comparison are editorial monitoring thresholds, not company guidance.

The conclusion becomes more constructive if AI revenue approaches or exceeds $16.0B, gross margin stays above 68%, and distributor concentration falls from 42%. Disclosure of accelerator and networking revenue—or enough product data to reconcile them—would improve the quality of the evidence even if total growth slowed.

The conclusion weakens if AI revenue falls below $14.7B while total revenue is near $29.4B, because AI would no longer be a majority of the guided company. It also weakens if gross margin falls below 68% as AI expands, or if concentration stays at 42% or rises.

That is the decision boundary: Broadcom has proved that AI is the growth engine. The next filing must show whether the engine is becoming more measurable, profitable, and diversified as it gets larger.

Methodology, Sources & Disclosure

This article separates company-reported results, SEC disclosures, company guidance, source-derived calculations, and editorial monitoring thresholds. AI share divides $10.8B by $22.187B. The growth bridge infers prior-year AI revenue as $10.8B / 2.43 = $4.444B, then divides the $6.356B AI increase by the $7.183B consolidated increase.

- Broadcom Q2 FY2026 financial results,

2026-06-03 - Broadcom Form 10-Q for the quarter ended 2026-05-03, filed

2026-06-09 - Broadcom Q2 FY2025 financial results,

2025-06-05

Facts were rechecked as of 2026-07-14. AI assisted with structure and consistency checks; the official sources, calculations, captures, EN/KO parity, and final wording require human review before production deployment. No sponsorship or affiliate relationship with Broadcom is disclosed. This is general information, not individualized investment advice; it does not issue a rating or share-price objective.