Market & Macro

Goldman Sachs Q2 2026: Is 23.5% ROE a Durable New Floor?

Goldman's Q2 ROE reached 23.5%, but 93.6% of revenue growth came from Global Banking & Markets. We reconstruct the durable-revenue test behind a 3.39× price-to-TBV hurdle.

Goldman Sachs' 23.5% Q2 2026 return on equity is evidence of a powerful franchise, but not yet a dependable new floor. Global Banking & Markets generated 93.6% of the firm's year-over-year revenue growth. The counterweight is that a source-derived proxy for financing, management fees and private banking revenue grew 33.9%. The next two quarters must show that both can coexist after trading conditions cool.

At a market snapshot of $1,140 per share, the shares equaled about 3.39× Q2 tangible book value. That is an expectations test, not a price target: Goldman must keep returns high, efficiency below 60% and tangible book compounding for the multiple to remain supported.

Source-derived answer map: Goldman Sachs Q2 2026 earnings release, earnings presentation, and article calculations. The visual organizes evidence; it does not forecast Q3 or estimate fair value.

| The 30-second answer | Verified evidence | What remains unproven |

|---|---|---|

| Returns were exceptional | 23.5% ROE; 25.5% ROTE | Whether the level survives a quieter trading quarter |

| Growth was concentrated | GBM supplied 93.6% of firm revenue growth | Whether other businesses can carry more of the next increase |

| The countercase is real | More-durable proxy +33.9% YoY | Whether its revenue share can hold or rise |

| Expectations are high | ~3.39× price/TBV | Whether premium returns and TBV compound together |

Thesis

Goldman's Q2 supports a balanced conclusion. The quarter was not merely a trading spike: financing revenue, management fees and private banking revenue all contributed to a more-durable proxy that grew by one-third. But the firmwide growth bridge was overwhelmingly driven by Global Banking & Markets, where Equities alone produced 54.1% of the firm's entire year-over-year revenue increase.

That distinction matters because a high-return quarter and a repeatable earnings system are different claims. Client activity, underwriting and asset prices can lift Global Banking & Markets quickly. Compensation and infrastructure costs do not necessarily fall at the same speed when activity normalizes. Goldman's 57.4% efficiency ratio shows excellent Q2 conversion; it does not prove the same conversion under a weaker mix.

The constructive case strengthens if Q3 and Q4 each hold ROE near or above 20%, the more-durable proxy remains near or above 42% of firm revenue, efficiency stays at or below 60%, and tangible book value per share continues growing. Those are editorial monitoring tests, not Goldman guidance or an investment rating.

Source Evidence Snapshot

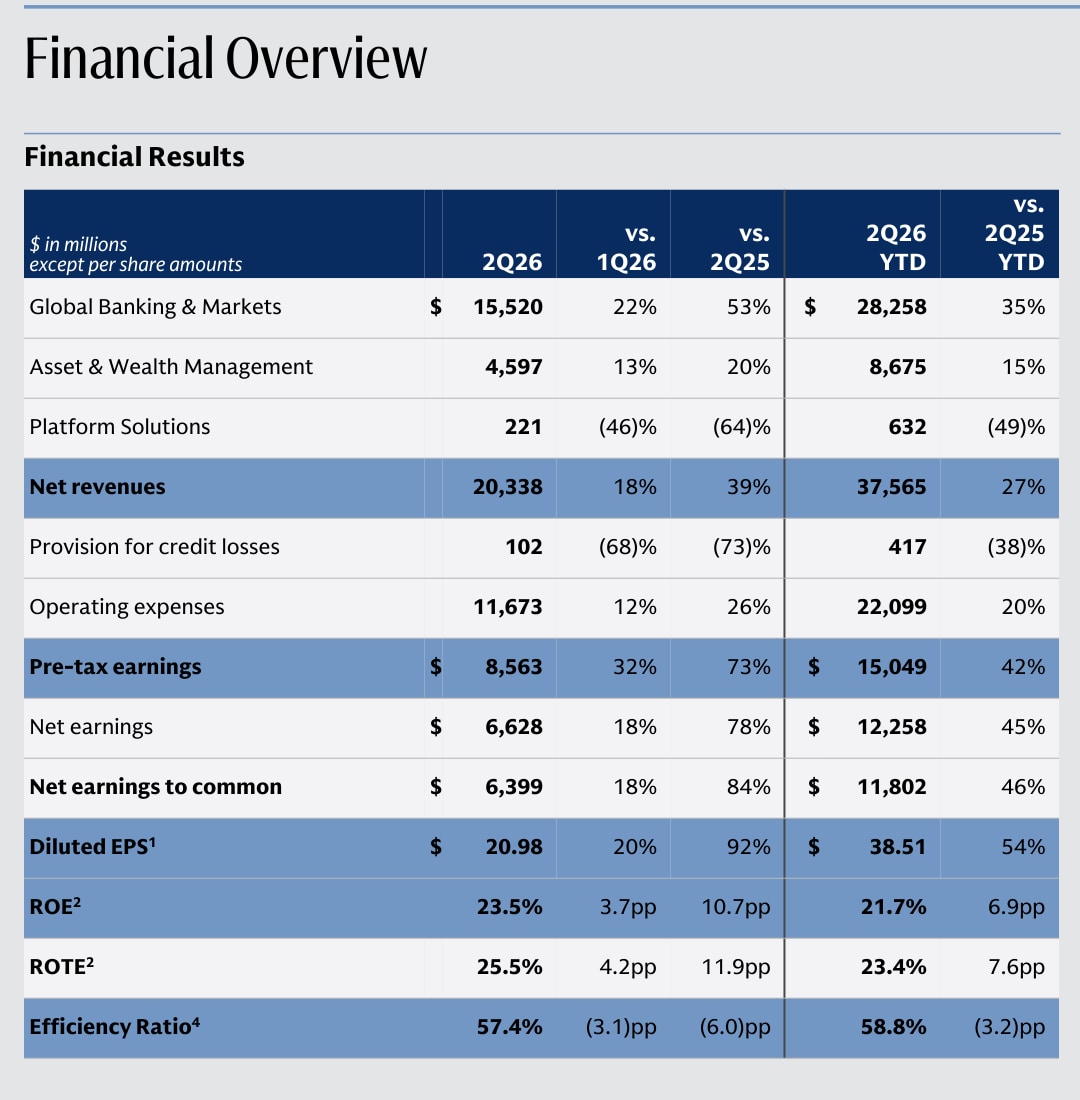

The official financial overview establishes the quarter's scale. Net revenues were $20.338B, net earnings were $6.628B and diluted EPS was $20.98 per share. Annualized ROE reached 23.5%, annualized ROTE reached 25.5%, and the efficiency ratio was 57.4%.

2026-07-14, captured 2026-07-15. Values are USD millions except per-share data and ratios. The slide proves reported results, not their future recurrence.Net revenues increased from $14.583B to $20.338B, a $5.755B gain. Global Banking & Markets rose from $10.133B to $15.520B, a $5.387B gain. Dividing those amounts gives 93.6%. Asset & Wealth Management added $766M, while Platform Solutions declined $398M. The result is a clean arithmetic bridge: almost all firmwide growth came from GBM.

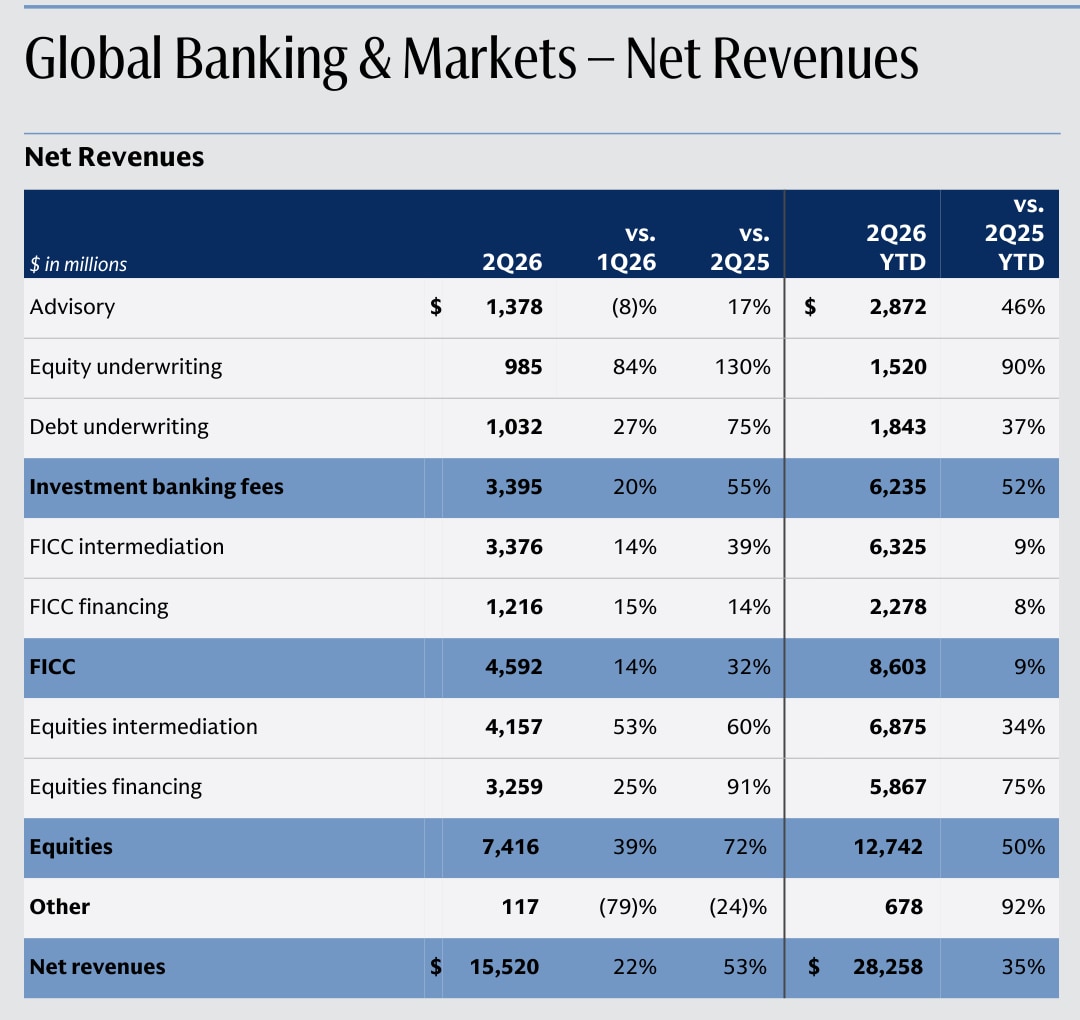

$5.387B / $5.755B = 93.6%. The bridge attributes revenue growth; it does not allocate incremental profit.GBM's official detail shows why the concentration was so large. Investment banking fees rose to $3.395B from $2.191B. FICC reached $4.592B from $3.487B, and Equities rose to $7.416B from $4.301B. Equities alone added $3.115B, or 54.1% of the firm's total revenue increase. Equities financing nearly doubled to $3.259B.

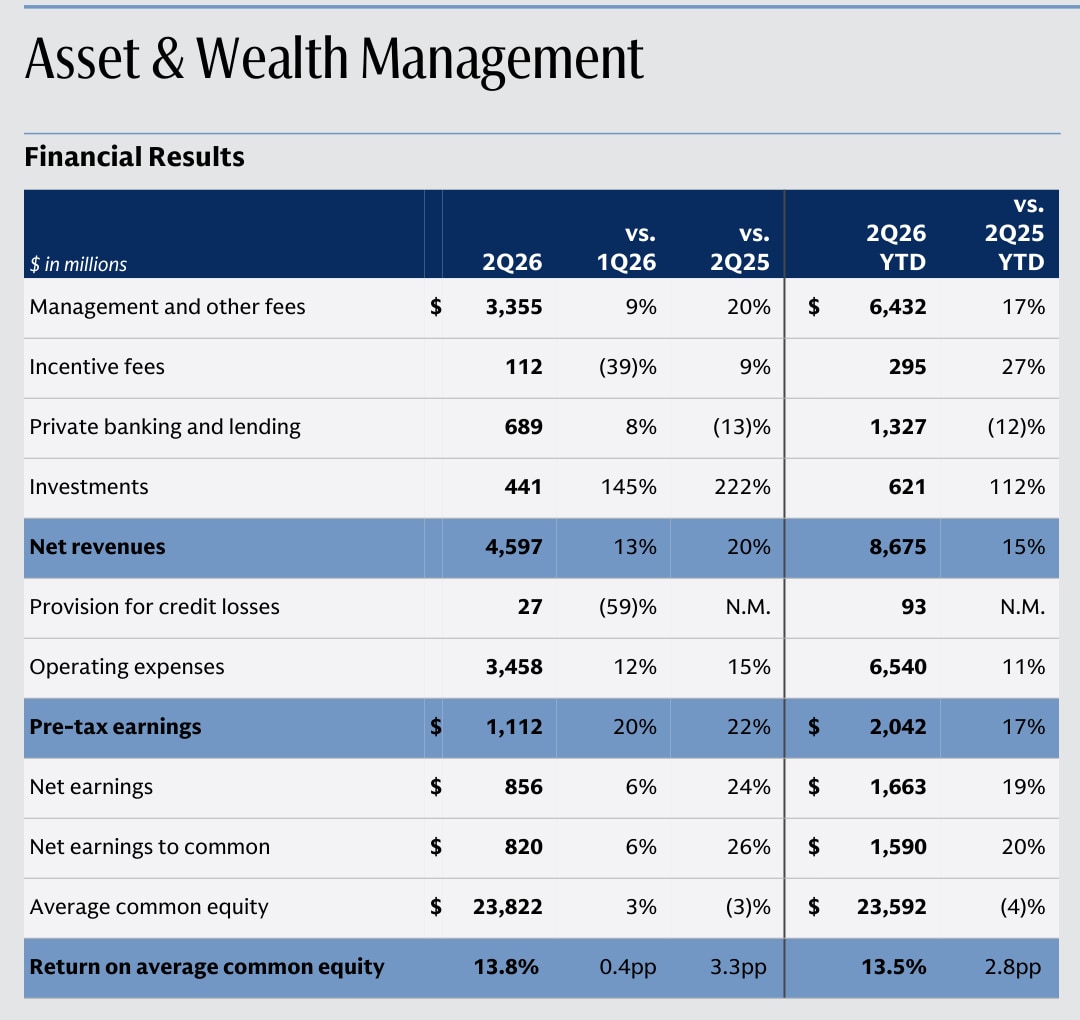

2026-07-14, captured 2026-07-15. Values are USD millions. The table proves the Q2 mix; it cannot show how client activity will normalize.The official 2025 annual report describes FICC financing, Equities financing, management and other fees, and private banking and lending as “more durable” revenues. Applying that classification to Q2 creates a transparent proxy: $1.216B + $3.259B + $3.355B + $0.689B = $8.519B. The same lines totaled $6.361B a year earlier, so the proxy grew 33.9%.

Source-derived explanation: Goldman Sachs 2025 annual report for the company classification and Q2 2026 earnings presentation, pages 4–5 for the inputs. Nex is an explainer only. “More durable” is a company category, not a guarantee that revenue recurs.

There is an important limit. The proxy represented 41.9% of firm revenue, down from 43.6% a year earlier because transactional revenue grew even faster. We also exclude AWM Investments revenue, which rose to $441M from $137M; Goldman attributed the increase mainly to higher private-equity gains. That is real revenue, but it does not belong in this recurrence test.

2026-07-14, captured 2026-07-15. Values are USD millions except assets under supervision. The source supports the fee and lending inputs and the exclusion of investment gains from the proxy.This source hierarchy follows the five-gate bank earnings guide: preserve the reported denominator, rebuild the earnings mechanism, then separate durable evidence from cyclical evidence. It also makes Goldman's question different from the JPMorgan Q2 adjusted-ROTCE test, where significant gains had to be removed before evaluating the operating quarter.

What the Street Is Pricing

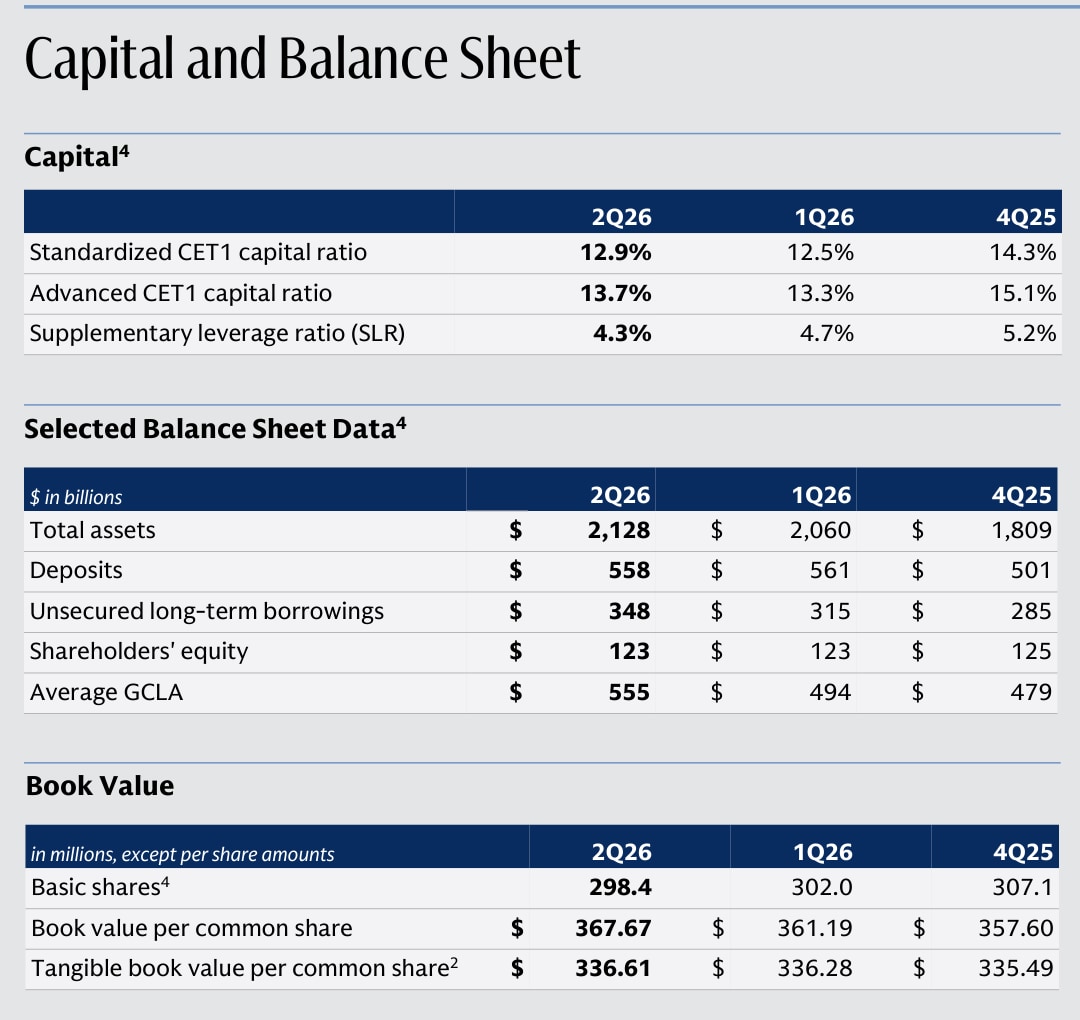

At 2026-07-14 23:59:36 UTC, Google Finance displayed Goldman Sachs at $1,140.00 per share. Goldman reported Q2 tangible book value of $336.61 per share and book value of $367.67 per share. The resulting ratios are about 3.39× tangible book and 3.10× book value.

Source-derived market snapshot: Google Finance and Goldman Sachs Q2 2026 earnings presentation, page 11. Calculation: $1,140.00 / $336.61 = 3.39×. This is expectation context, not a fair-value estimate or price objective.

| Expectation bridge | Value | Boundary |

|---|---|---|

| Price / tangible book value | ~3.39× | Timestamped price divided by quarter-end company TBV |

| Price / book value | ~3.10× | $1,140.00 / $367.67 |

| Q2 annualized ROE | 23.5% | One quarter under favorable activity conditions |

| Q2 annualized ROTE | 25.5% | Company non-GAAP measure |

| Q2 efficiency ratio | 57.4% | Historical conversion, not a forward promise |

The multiple does not establish that the shares are expensive. It identifies what must keep working. At more than 3× tangible book, the case depends less on closing a discount and more on sustaining premium returns while increasing the equity base per share.

The official capital table provides that denominator. Standardized CET1 was 12.9%, the supplementary leverage ratio was 4.3%, and tangible book value was $336.61 per share. Goldman repurchased $4.0B of stock during Q2 at an average price of $984.57 per share. The $1,140 snapshot was 15.8% above that average, making future buybacks less accretive than the quarter's purchases, all else equal.

2026-07-14, captured 2026-07-15. The table proves quarter-end capital and Q2 distributions; it does not forecast future repurchase prices or capital requirements.Risks to the Thesis

The first risk is revenue concentration. GBM represented 76.3% of firm revenue and 88.0% of common net earnings. A decline in underwriting, client activity or asset prices can therefore affect both the top line and compensation-driven operating leverage.

The second risk is confusing financing with fixed revenue. FICC and Equities financing are more durable than directional trading under Goldman's classification, but balances, spreads and client demand can still change. The label improves the analytical grouping; it does not turn market-sensitive revenue into a subscription.

The third risk is private-asset marks. AWM Investments revenue increased because of higher private-equity gains. Those gains supported Q2 earnings but were excluded from the durable proxy. A reversal would create a headwind even if management fees remain healthy.

The fourth risk is the valuation-capital interaction. The stock snapshot was near 3.39× TBV and above the quarter's average repurchase price. If returns normalize, regulatory capital needs rise or TBV growth slows, the multiple can lose support without a balance-sheet crisis.

| Risk path | Q2 evidence | What would weaken the thesis |

|---|---|---|

| GBM concentration | 93.6% of firm revenue growth | Activity normalizes before AWM and Platform Solutions offset it |

| Revenue durability | Proxy +33.9%, but mix down to 41.9% | Financing and fee revenue decelerate while trading falls |

| Operating leverage | Efficiency ratio 57.4% | Expense holds while revenue falls, lifting efficiency above 60% |

| Private-asset marks | AWM Investments $441M | Investment gains reverse and fee growth cannot offset them |

| Valuation and capital | ~3.39× TBV; CET1 12.9% | ROE and TBV growth weaken as capital requirements or payout pressure rise |

What Flips the Call

Goldman schedules its Q3 2026 results for 2026-10-13. One quarter can test the direction, but two are needed to judge whether Q2 established a stronger return regime.

Editorial decision visual based on the Q2 earnings release, earnings presentation, and official 2026 earnings calendar. The thresholds are editorial monitoring tests, not Goldman guidance.

| Watch item | Q2 evidence | Constructive condition | Weakening condition |

|---|---|---|---|

| Annualized ROE | 23.5% | Q3 and Q4 each near or above 20% | Falls below 20% as activity normalizes |

| More-durable proxy | $8.519B; 41.9% of revenue | Holds near or above 42% of firm revenue | Financing and fee lines lose share together |

| Efficiency ratio | 57.4% Q2; 58.8% YTD | Remains at or below 60% | Moves above 60% as revenue cools |

| Tangible book value | $336.61 per share | Continues growing after distributions | Stalls while valuation remains above 3× TBV |

| Growth breadth | GBM supplied 93.6% of growth | AWM and other lines supply more of the next increase | GBM weakens with no offset elsewhere |

The conclusion becomes more constructive if both Q3 and Q4 keep ROE near 20% or better while the more-durable revenue mix holds around 42%, efficiency remains below 60% and TBV per share rises. That combination would show that Q2's high return was supported by a broader earnings system.

It weakens if GBM activity cools and all three cushions fail together: financing and fees lose share, efficiency moves above 60%, and tangible book value stops growing. A single slower trading quarter would not flip the call. A weaker revenue mix plus weaker conversion would.

Methodology, Sources & Disclosure

The firmwide growth bridge subtracts Q2 2025 net revenue from Q2 2026 and repeats that calculation for each segment. The more-durable proxy applies Goldman's annual-report classification to the exact Q2 financing, management-fee and private-banking lines; it excludes AWM Investments revenue. Price-to-book ratios use one timestamped public price and quarter-end company values. None is a fair-value estimate.

- Goldman Sachs Q2 2026 earnings release, published

2026-07-14 - Goldman Sachs Q2 2026 results PDF, published

2026-07-14 - Goldman Sachs Q2 2026 earnings presentation, published

2026-07-14 - Goldman Sachs 2025 annual report, checked

2026-07-15 - Goldman Sachs 2026 earnings calendar, checked

2026-07-15 - Google Finance Goldman Sachs market snapshot, observed

2026-07-14 23:59:36 UTC

Facts, calculations, image captures and links were rechecked as of 2026-07-15. AI assisted with structure, chart production and EN/KO consistency checks; official sources, calculations and final wording require human review before production deployment. No sponsorship or affiliate relationship with Goldman Sachs is disclosed. This is general information, not individualized investment advice; it does not issue an investment rating or share-price objective.