Market & Macro

Intel Stock in 2026: Product Profit Versus Foundry Margin Repair

A 2026 Intel stock review that separates market-cap pressure, product-segment profit, foundry losses, cash-flow coverage, and the PC-cycle backdrop.

(Sources: Nasdaq official quote APIs, Intel Q4/FY2025 financial results, Intel Q4/FY2025 earnings release PDF, IDC PC market outlook blog, AMD Q4/FY2025 financial results)

Thesis

Intel is no longer priced like a broken CPU incumbent that only needs a small PC rebound. The captured Nasdaq quote response showed INTC at $62.38 with a market cap of about $312.7 billion. Against reported 2025 revenue of $52.9 billion, that is roughly 5.9x trailing sales for a company that still reported a negative GAAP operating margin for the year.

Related reading: Fed Rate Outlook in 2026: Data Triggers Before Cuts | Carbon Credit Exposure in 2026: Product Structure and Diligence Questions | U.S. Stock Investing in 2026: Broker Checks Before Stock Selection

The cleaner thesis is that Intel has a real product engine but an unresolved manufacturing burden. Client and data-center CPUs still generate operating profit. Intel Foundry still absorbs too much of that profit. The stock works only if product recovery and 18A execution begin to repair the margin structure faster than investors currently fear.

Source Evidence Snapshot

The hero image already carries Intel's Q4/FY2025 summary and Q1 guidance surface. The body evidence keeps three non-overlapping visual roles: market-cap context, product-versus-foundry profitability, and cash/capex discipline. IDC and AMD remain linked context rather than another screenshot layer.

Source capture: Nasdaq official quote APIs, captured 2026-04-13. The highlighted fields show INTC at $62.38, market cap at 312,731,235,770, and average volume at 95,405,685.

Quote API |

Summary API.

Source capture: Nasdaq official quote APIs, captured 2026-04-13. The highlighted fields show INTC at $62.38, market cap at 312,731,235,770, and average volume at 95,405,685.

Quote API |

Summary API.

The quote context matters because it removes the "cheap by default" framing. At more than $312 billion of market value, Intel already prices in some recovery.

Source capture: Intel supplemental operating segment results, page 9 of the Q4/FY2025 release, captured 2026-04-13. The marked figures show Q4 operating income of $2.209 billion for CCG, $1.250 billion for DCAI, and an operating loss of $2.509 billion for Intel Foundry.

Open source.

Source capture: Intel supplemental operating segment results, page 9 of the Q4/FY2025 release, captured 2026-04-13. The marked figures show Q4 operating income of $2.209 billion for CCG, $1.250 billion for DCAI, and an operating loss of $2.509 billion for Intel Foundry.

Open source.

This is the filing excerpt that should anchor the equity case. Client Computing Group and Data Center and AI remain profitable. Intel Foundry's quarterly loss was large enough to absorb most of that product profit.

Source capture: Intel consolidated statements of cash flows, page 8 of the Q4/FY2025 release, captured 2026-04-13. The marked figures show 2025 net cash from operating activities of 9,697 and additions to property, plant and equipment of 14,646.

Open source.

Source capture: Intel consolidated statements of cash flows, page 8 of the Q4/FY2025 release, captured 2026-04-13. The marked figures show 2025 net cash from operating activities of 9,697 and additions to property, plant and equipment of 14,646.

Open source.

Intel is not starving for cash, but it is not in a clean free-cash-flow posture either. The company generated $9.697 billion of cash from operations in 2025 and spent $14.646 billion on property, plant and equipment.

Source note: IDC PC market outlook blog, captured 2026-04-13. The PC-cycle evidence is kept as linked context because it qualifies the recovery thesis but does not need a fourth body screenshot.

What the Street is Pricing

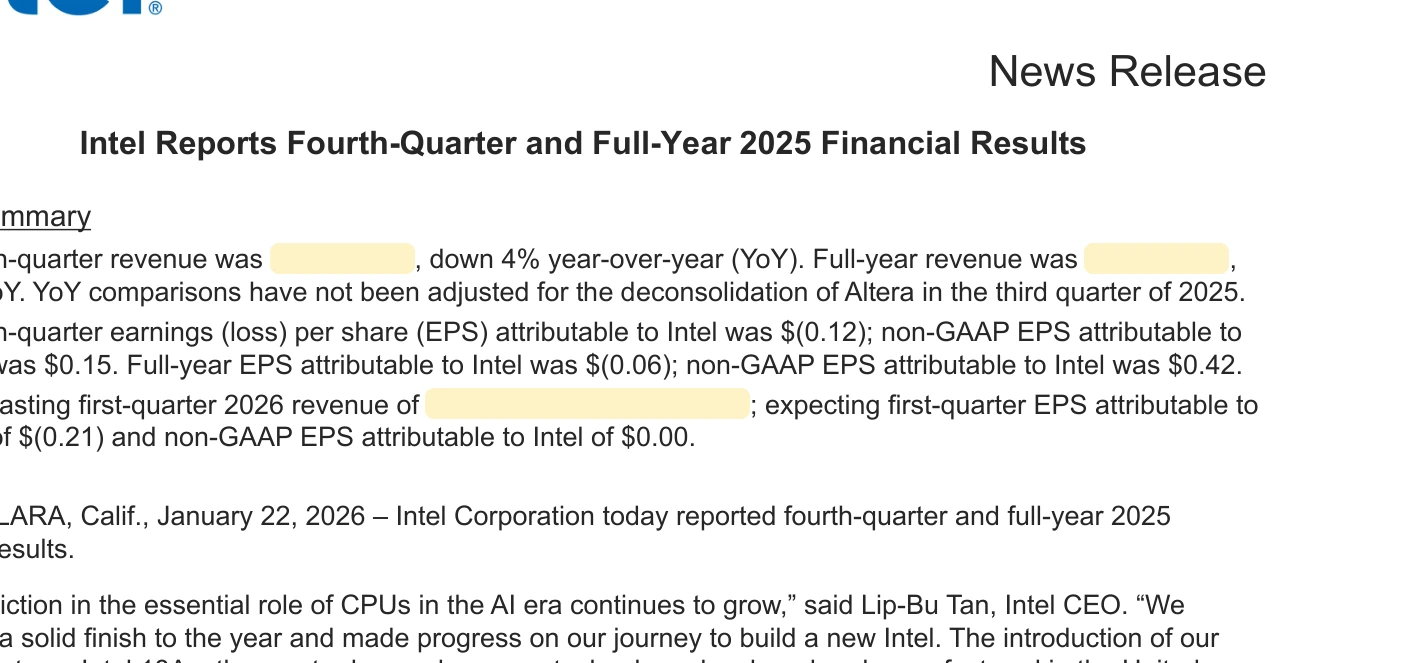

The market is pricing a repair case, not a rescue case. Intel's official release said Q4 revenue was $13.7 billion, full-year revenue was $52.9 billion, and Q1 2026 revenue guidance was $11.7 billion to $12.7 billion. It also showed Q4 Client Computing Group revenue of $8.2 billion, Data Center and AI revenue of $4.7 billion, and Intel Foundry revenue of $4.5 billion.

Those numbers are good enough to show that the CPU franchise still matters. They are not enough to make the valuation easy. A market cap above $312 billion against $52.9 billion of trailing revenue says investors are already paying for stabilization, 18A credibility, and foundry-loss improvement.

Public consensus target data was not part of the reviewed evidence. That matters because this article should not pretend to know a single intrinsic-value number. The observable market signal is simpler: the stock no longer carries a low-expectation multiple.

Risks to the Thesis

The first risk is that Intel Foundry remains too large a drag. Product segments can recover, but the equity case does not clean up until foundry operating losses narrow enough for product profit to show through.

The second risk is capital intensity. Intel's 2025 operating cash flow was real, but property, plant, and equipment additions were larger. Investors are effectively funding a manufacturing reset now in exchange for a better future margin structure.

The third risk is the PC backdrop. IDC's published view points to an 11.3% global PC-market decline in 2026 before a later rebound. AI PC language does not automatically create an easy unit cycle.

The fourth risk is competition. AMD's official Q4/FY2025 release showed stronger growth momentum in data center and client revenue. Intel still has larger client scale and deeper OEM reach, but it has to prove share and mix durability where the market is most willing to pay for performance.

What Flips the Call

The thesis improves if Q1 2026 revenue lands toward the upper end of the $11.7 billion to $12.7 billion range, Data Center and AI holds momentum against AMD, client demand stays resilient despite weak PC units, and Intel Foundry losses narrow in a visible way.

The thesis weakens if the product businesses stabilize but foundry losses keep absorbing the recovery, or if capital spending continues to exceed the cash engine without a clearer path to margin repair.

Intel is not a broken-CPU case anymore. It is a product-profit and manufacturing-repair case in a market that already prices a meaningful part of the turnaround.